{kind=link}

The difference between the current 10-year Treasury yield and its estimated “fair value” has recently contracted to its narrowest point in a year, according to recent market analyses. This development suggests a potential recalibration in bond market expectations and a possible shift in investor sentiment.

Understanding the Fair Value Estimate

Table of Contents

- 1. Understanding the Fair Value Estimate

- 2. A Downward Trend in Market Premium

- 3. Impact of Government Shutdown on data

- 4. Understanding Treasury Yields and Fair Value

- 5. Frequently Asked Questions About 10-Year Treasury Yields

- 6. What factors are contributing to the current adjustment of Treasury yields toward fair value?

- 7. Treasury Yields Adjust Toward Fair Value Amid Ongoing Rate Normalization

- 8. Understanding the Shift in Treasury Yields

- 9. What is Rate Normalization?

- 10. Factors Driving the Adjustment in Treasury Yields

- 11. Impact on Different Treasury Maturities

- 12. the Yield Curve and Recession Signals

- 13. Implications

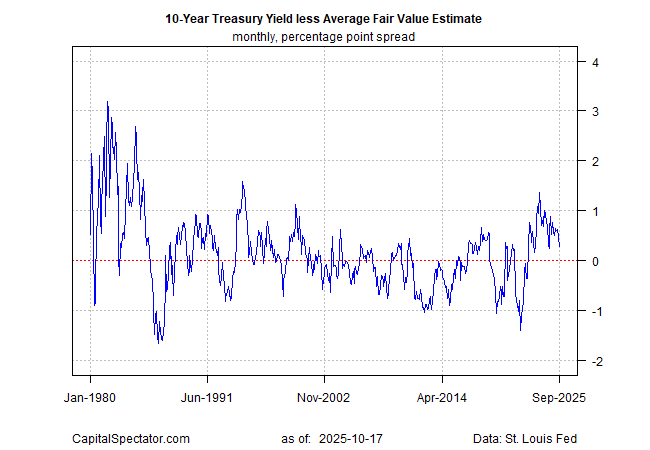

A recent monthly analysis,encompassing data through September,indicates an ongoing reduction in the market’s premium over fair value throughout the year. The current calculation places the fair value of the 10-year yield at 3.85%, a figure 27 basis points lower than the observed average market rate of 4.12% in September.this shrinking premium signals a growing alignment between market pricing and underlying economic fundamentals.

this latest decrease in the market premium continues a consistent downward trajectory observed over recent months. Analysts point to a mean-reversion dynamic influencing the 10-year yield, where premiums and discounts naturally adjust relative to the estimated fair value. The premium peaked at approximately 1.4 percentage points in late 2023, highlighting the ample shift in market perception as then.

Impact of Government Shutdown on data

Its crucial to note that these estimates are based on modeling that is currently operating with incomplete economic data. The scheduled September report on consumer spending, as an example, has been delayed due to the ongoing government shutdown. However, the impact of these missing data points has been minimized by employing three distinct models that utilize a broad range of economic indicators and market data. Analysts anticipate that the models will be updated and refined once the delayed reports are released.

Did You Know? The 10-year Treasury yield serves as a benchmark for numerous othre interest rates, impacting everything from mortgage rates to corporate borrowing costs.

| Metric | September Value |

|---|---|

| 10-Year Treasury Yield (Average) | 4.12% |

| Fair Value Estimate (10-Year Yield) | 3.85% |

| Premium (Difference) | 27 Basis Points |

pro Tip: Understanding the relationship between Treasury yields and their fair value can offer valuable insights into broader market sentiment and potential investment opportunities.

The current situation presents a compelling picture of a bond market undergoing a period of adjustment. The narrowing premium suggests that investors are increasingly aligned with fundamental economic conditions. Though, the absence of key data due to the government shutdown adds a layer of uncertainty, and future analyses will be crucial in confirming these trends.

what implications do you foresee from this shift in the 10-year Treasury yield premium? How might this affect your investment strategy?

Understanding Treasury Yields and Fair Value

Treasury yields represent the return an investor receives on U.S. government debt. As these yields fluctuate, they influence borrowing costs across the entire economy. The concept of “fair value” attempts to determine what a yield *should* be based on a complex interplay of economic factors such as inflation expectations, economic growth, and Federal Reserve policy.

Analyzing the difference between the market yield and the estimated fair value provides insight into whether the market is over- or under-pricing risk. A high premium suggests investors are demanding a larger return to compensate for perceived risks,while a low premium indicates a more optimistic outlook.

For additional information on Treasury yields, consult the U.S. Department of the Treasury’s website: https://home.treasury.gov/resource-center/data-chart-center/interest-rates

Frequently Asked Questions About 10-Year Treasury Yields

- What is a 10-year Treasury yield? It’s the return an investor receives for holding a U.S. treasury bond for 10 years.

- What does ‘fair value’ mean in the context of Treasury yields? It’s an estimated yield based on economic models and fundamental factors.

- Why is the premium between the yield and fair value important? It indicates whether the market perceives the yield as overvalued or undervalued.

- How does the government shutdown affect these calculations? Delayed economic data introduces uncertainty into the fair value estimates.

- What factors influence the fair value of a 10-year treasury yield? Inflation expectations, economic growth, and Federal Reserve policy are key influences.

- Can this narrowing premium signal a change in market direction? potentially, it suggests a shift in investor sentiment and a possible recalibration of expectations.

- Where can I find more information about Treasury yields? The U.S. Department of the Treasury website provides complete data and resources.

share your thoughts on this developing story in the comments below!

What factors are contributing to the current adjustment of Treasury yields toward fair value?

Treasury Yields Adjust Toward Fair Value Amid Ongoing Rate Normalization

Understanding the Shift in Treasury Yields

For much of the past decade, Treasury yields have been artificially suppressed by extraordinary monetary policy – quantitative easing (QE) and near-zero interest rates. Now, as central banks globally engage in rate normalization, we’re witnessing a recalibration. This isn’t necessarily a “spike” in rates, but rather an adjustment toward what manny economists consider fair value. This process impacts everything from mortgage rates and corporate borrowing costs to stock valuations and global capital flows. Understanding the dynamics at play is crucial for investors and businesses alike.

What is Rate Normalization?

Rate normalization refers to the process of gradually raising interest rates from historically low levels. Following the 2008 financial crisis and, more recently, the COVID-19 pandemic, central banks implemented aggressive easing policies to stimulate economic growth. These policies included:

* Lowering the Federal Funds Rate: The target rate banks charge each other for overnight lending.

* Quantitative Easing (QE): Purchasing government bonds and other assets to inject liquidity into the financial system.

* Forward Guidance: Communicating the central bank’s intentions, what conditions would cause it to maintain its course, and what conditions would cause it to change course.

As inflation surged in 2022 and 2023,central banks began to reverse course,initiating a period of monetary tightening – the opposite of easing. This tightening is the core of rate normalization.

Factors Driving the Adjustment in Treasury Yields

Several interconnected factors are contributing to the current adjustment in Treasury yields:

* Inflation Expectations: While inflation has cooled from its peak, expectations remain elevated. Higher inflation expectations translate directly into higher nominal yields.The market is pricing in the risk of persistent inflation, demanding a greater return to compensate for the erosion of purchasing power.

* Federal Reserve Policy: The Federal Reserve’s (fed) actions – raising the federal funds rate and reducing its balance sheet (quantitative tightening or QT) – directly influence Treasury yields. The Fed’s commitment to bringing inflation back to its 2% target is a key driver.

* Stronger Economic Data: Resilient economic growth, particularly in the U.S., suggests the economy can withstand higher interest rates.This reduces the risk of a recession,allowing yields to rise. Indicators like the ISM Manufacturing PMI and non-farm payroll reports are closely watched.

* Increased Supply of Treasuries: The U.S. government’s increasing debt burden necessitates a larger supply of Treasury bonds. Increased supply, all else equal, puts upward pressure on yields.

* Global Demand for U.S. Debt: Fluctuations in global demand for U.S. debt also play a role. Geopolitical events and economic conditions in other countries can impact investor appetite for U.S.Treasury securities.

Impact on Different Treasury Maturities

the adjustment in Treasury yields isn’t uniform across the yield curve.

* Short-Term Yields: These are most directly influenced by the Fed’s policy rate. They’ve risen significantly as the Fed has hiked rates.

* Intermediate-Term Yields: Reflect expectations for future Fed policy and economic growth. They’ve also increased, but to a lesser extent than short-term yields.

* Long-term Yields: Are influenced by a broader range of factors, including inflation expectations, economic growth prospects, and global demand. While they initially rose sharply, they’ve shown more volatility and, at times, have fallen as recession fears have resurfaced. The 10-year Treasury yield is a particularly important benchmark.

the Yield Curve and Recession Signals

The yield curve – the difference between long-term and short-term Treasury yields – is closely watched as a potential recession indicator. An inverted yield curve (where short-term yields are higher than long-term yields) has historically preceded recessions. While the yield curve has inverted at times, its predictive power isn’t foolproof. The current flattening of the yield curve suggests increased economic uncertainty.