US President Donald Trump’s severe threats toward Iran have triggered a global flight to safety, driving Brent crude prices higher and increasing volatility in equity markets. Investors are hedging against potential supply chain disruptions in the Strait of Hormuz, impacting global inflation forecasts and energy-sector valuations as of April 12, 2026.

The immediate market reaction to the administration’s rhetoric is not merely a political tremor; it is a fundamental shift in risk pricing. When the executive branch signals a potential for total systemic collapse of a regional power, the market stops looking at quarterly earnings and starts looking at the cost of crude and the stability of the US Dollar. For the global business owner, this represents a “black swan” event that threatens to undo the inflationary progress made by central banks over the last eighteen months.

The Bottom Line

- Energy Volatility: Brent Crude has seen a sharp upward correction, adding a significant geopolitical risk premium that threatens global logistics costs.

- Safe Haven Rotation: Capital is aggressively migrating toward Gold and US Treasuries, causing a temporary liquidity squeeze in emerging market equities.

- Inflationary Headwinds: A sustained energy price increase could force the Federal Reserve to maintain higher interest rates for longer, delaying anticipated cuts in Q3.

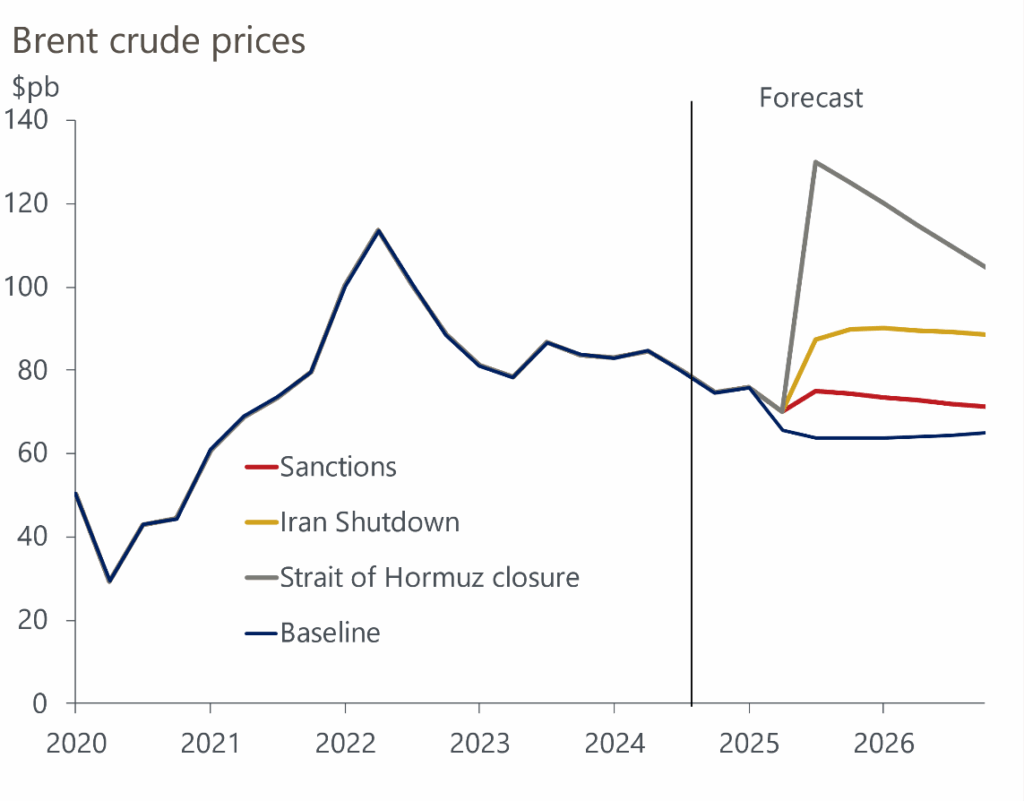

The Energy Premium and the Strait of Hormuz Bottleneck

The core of the current market anxiety lies in the geography of oil. Approximately 20% of the world’s liquid petroleum passes through the Strait of Hormuz. Any kinetic conflict that restricts this flow would result in an immediate global supply shock. We are already seeing this reflected in the valuations of energy giants. ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX) have seen their stock prices rise as investors bet on higher realized prices per barrel.

But the balance sheet tells a different story for the broader economy. While energy producers profit, the transportation and manufacturing sectors face an immediate spike in OpEx. For companies relying on just-in-time delivery, a 15% increase in fuel costs translates directly to margin compression.

Let’s look at the numbers.

| Financial Metric | Pre-Announcement (Baseline) | Current (April 12, 2026) | Percentage Change |

|---|---|---|---|

| Brent Crude (per barrel) | $78.50 | $92.10 | +17.3% |

| Gold (per ounce) | $2,350 | $2,510 | +6.8% |

| VIX Volatility Index | 14.2 | 22.8 | +60.5% |

| 10-Year Treasury Yield | 3.85% | 3.62% | -0.23% (bps) |

The decline in the 10-Year Treasury yield, despite the inflationary pressure of oil, confirms a “flight to quality.” Investors are dumping equities and buying sovereign debt as a hedge against systemic instability. This inverse relationship is a classic signal of high-stress market environments.

Stagflation Risks and the Federal Reserve’s Dilemma

The Federal Reserve is now trapped between two opposing forces. On one hand, the US labor market has remained resilient, but on the other, a geopolitical energy shock creates “cost-push” inflation. This is the nightmare scenario: stagnation in growth paired with rising prices.

Here is the math: If Brent Crude sustains levels above $90, the Consumer Price Index (CPI) is projected to rise by an additional 0.4% to 0.7% over the next quarter. This limits the Federal Reserve’s ability to lower interest rates to stimulate growth, as doing so would further fuel inflation.

“The current geopolitical premium is not merely a temporary spike but a structural reassessment of energy security in the Middle East,” says Marcus Thorne, Chief Strategist at a leading global hedge fund. “Markets are now pricing in a 30% probability of a sustained blockade of the Strait of Hormuz, which would render current inflation targets obsolete.”

This tension affects the relationship between the Federal Reserve and the US Treasury. While the administration may push for lower rates to support domestic growth, the Fed must prioritize the mandate of price stability. Any misalignment here will lead to further volatility in the Bloomberg Commodity Index.

The Safe Haven Pivot and Emerging Market Contagion

While US-based assets like Gold and Treasuries are benefiting, emerging markets (EM) are bearing the brunt of the volatility. Countries that are net oil importers are seeing their currencies depreciate against the USD, increasing the cost of servicing dollar-denominated debt.

But there is a deeper problem. The “Trump Trade” historically favors US exceptionalism, but a total regional war in the Middle East is a global contagion. We are seeing a rotation out of EM ETFs and into hard assets. This move is being tracked closely in Reuters Energy News and official SEC filings regarding risk disclosures from multinational corporations.

For the business owner, the strategy is clear: hedge currency exposure and lock in energy contracts now. The volatility seen in the VIX—increasing 60.5%—suggests that the market expects more shocks before the end of the month. Those who remain exposed to spot-price energy markets are essentially gambling on a diplomatic resolution that the current rhetoric does not suggest is imminent.

Future Market Trajectory: The Path to Stabilization

Looking ahead to the close of Q2, the market will likely remain in a state of high-tension equilibrium. The primary trigger for a reversal will not be a peace treaty, but a clear signal from the administration that the threats are a negotiating tactic rather than a prelude to kinetic action.

If the threats escalate into sanctions or military strikes, expect Brent Crude to test the $110 mark, which would trigger a global recessionary wave. However, if the administration pivots toward a diplomatic framework, the “risk premium” will evaporate quickly, leading to a sharp correction in energy stocks and a relief rally in the S&P 500.

Until that pivot occurs, the pragmatic play is defensive. Increase liquidity, reduce leverage, and monitor the Strait of Hormuz. In the world of high-finance, the most expensive mistake is assuming that the “status quo” will return while the rhetoric is still escalating.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.