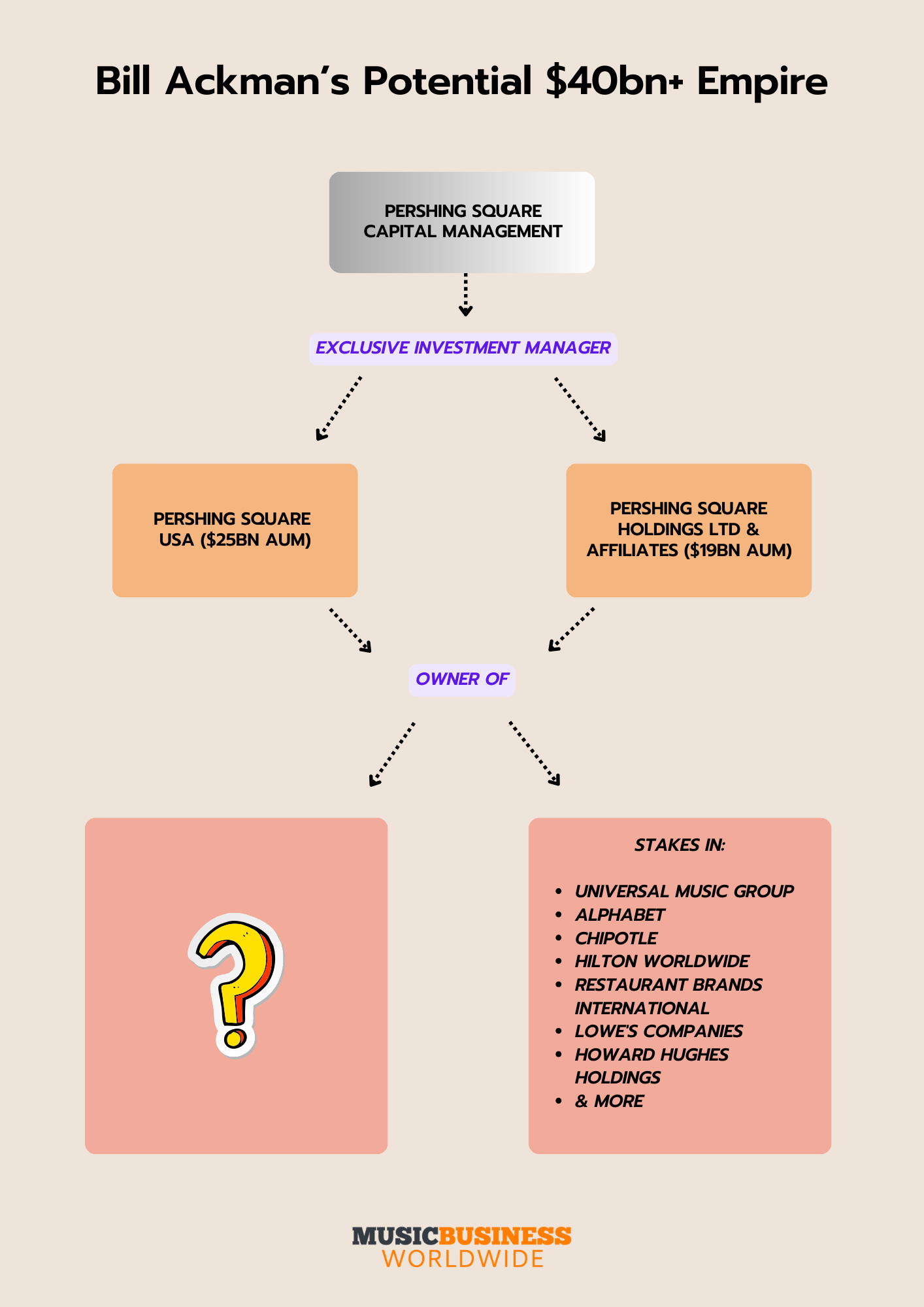

Bill Ackman’s Pershing Square has launched a $65 billion bid to acquire Universal Music Group (UMG), the world’s largest music company. The move, unfolding this Tuesday, aims to consolidate the global music market, leveraging UMG’s massive catalog of stars like Taylor Swift to dominate streaming and royalty revenues.

This isn’t just another corporate merger or a fancy line item on a balance sheet; it is the ultimate “financialization” of sound. When a hedge fund titan views the world’s most influential melodies as a diversified asset portfolio, the relationship between the artist and the label shifts fundamentally from a creative partnership to a strategy of equity management. We are witnessing the moment where pop culture ceases to be a product and officially becomes a commodity class.

The Bottom Line

- The Valuation: The $65 billion price tag reflects a massive premium on intellectual property (IP) in an era of algorithmic consumption.

- The Strategy: Ackman is betting that streaming royalties provide a more stable, predictable yield than the volatility of the traditional stock market.

- The Artist Risk: A shift toward “asset optimization” could lead to more aggressive catalog acquisitions and tighter control over artist royalties.

The Hedge Fund Playbook and the Music Asset Class

For years, we’ve seen the “quiet” acquisition of catalogs. Bob Dylan, Bruce Springsteen, and Sting all sold their life’s work to investment firms like Hipgnosis or BMG. But those were surgical strikes. What Ackman is attempting with Bloomberg-tracked movements is a full-scale invasion.

By acquiring the entire house of UMG, Pershing Square isn’t just buying songs; they are buying the infrastructure of global fame. From Kendrick Lamar’s lyrical dominance to the sheer economic engine of the Eras Tour, UMG controls the pipes through which the world hears music. But the math tells a different story than the art.

To a financier, a song is essentially a perpetual annuity. As long as people stream, the check clears. In a world of inflation and geopolitical instability, the “Taylor Swift Effect” is a safer bet than most government bonds. Here is the kicker: Ackman isn’t just looking at current royalties; he’s looking at the untapped potential of licensing in virtual worlds and AI-generated experiences.

The Streaming Squeeze and the Power Shift

For a decade, the “Streaming Wars” were fought between platforms—Spotify vs. Apple Music vs. Amazon. But the real power doesn’t lie with the platform; it lies with the content owner. If you own the music, the platforms are merely your delivery drivers.

By consolidating UMG under a private equity-style lens, Ackman gains immense leverage in royalty negotiations. If UMG decides to pull its catalog or demand a higher percentage of revenue, Spotify’s stock price doesn’t just dip—it craters. This creates a vertical monopoly where the owner of the IP can dictate the terms of the technology.

This shift mirrors the consolidation we’ve seen in the film industry, where Variety has frequently noted the struggle of mid-budget films against the monolithic IP of Disney and Warner Bros. Discovery. In music, the “blockbuster” isn’t a movie; it’s a global superstar’s entire discography.

| Major Label | Estimated Market Share | Primary Value Driver | Strategic Focus (2026) |

|---|---|---|---|

| Universal Music Group | ~32% | Massive Frontline Catalog | AI Rights & Global Scaling |

| Sony Music | ~21% | Deep Publishing Assets | Cross-Media Integration |

| Warner Music Group | ~17% | Strategic Indie Partnerships | Creator Economy Tech |

The AI Wildcard: Protection or Exploitation?

We cannot talk about a $65 billion bid without talking about Artificial Intelligence. UMG has spent the last two years in a legal trench war against “deepfake” music and unauthorized AI training. Ackman’s interest likely stems from the fact that UMG owns the “clean” data.

If the future of music involves AI-generated tracks that sound like a 1970s Stevie Wonder or a 2010s Rihanna, the person who owns the original voice-print owns the copyright. It is a land grab for the digital DNA of human creativity. Let’s be real: the goal isn’t to foster new talent; it’s to monetize the existing legacy in ways the original artists never imagined.

“The transition of music from a cultural service to a financial asset is nearly complete. When the valuation is driven by discounted cash flow models rather than artistic merit, the industry risks alienating the very creators who generate the value.”

This sentiment, echoed by various analysts at Billboard, highlights the tension. If Pershing Square treats UMG like a portfolio of stocks, the “A&R” (Artists and Repertoire) process becomes a data science project. We move from “I hear a star” to “The data suggests this demographic will yield a 4% increase in quarterly dividends.”

From the Studio to the Spreadsheet

The ripple effects of this deal will be felt far beyond the recording studio. We are looking at a potential clash with the “Creator Economy.” As independent artists find more success via TikTok and direct-to-fan platforms, a consolidated UMG under Ackman might pivot toward aggressive acquisition of these independent “micro-labels” to stifle competition.

this affects the live touring circuit. With Deadline reporting on the ongoing scrutiny of ticketing monopolies, a hedge-fund-backed UMG could seek to integrate more deeply with live event promoters, creating a “closed loop” where they control the recording, the streaming, and the ticket to the present.

It is a dizzying amount of power. But is it sustainable? The risk is “franchise fatigue.” When music is managed for maximum efficiency, it often loses the raw, unpredictable edge that makes it culturally relevant in the first place. You can’t optimize a revolution, and you can’t place a spreadsheet on a soul.

the $65 billion offer is a bet on the permanence of the superstar. Ackman is betting that the world will always wish the biggest names, and that those names are the safest investments on earth. Whether the artists feel the same way is a different story entirely.

What do you think? Does the “financialization” of music kill the art, or is this just the natural evolution of the industry? Let me understand in the comments if you’d trust a hedge fund manager with your favorite artist’s legacy.