Rising credit card APRs are increasing the cost of consumer debt as balances hit record highs. Borrowers are utilizing balance transfer cards with 0% introductory rates to mitigate interest expenses and accelerate principal repayment, a critical move as the Federal Reserve maintains a restrictive monetary stance to curb inflation.

This shift in consumer behavior is not merely a personal finance trend; it is a macroeconomic indicator. As the cost of servicing debt rises, the discretionary income of the American consumer shrinks, creating a direct headwind for retail and service sectors. When the Federal Reserve adjusts the federal funds rate, the ripple effect hits the prime rate almost instantly, which in turn dictates the APRs seen on statements from JPMorgan Chase (NYSE: JPM) and Bank of America (NYSE: BAC). For the market, the critical metric is no longer just the volume of spending, but the quality of the debt supporting that spending.

The Bottom Line

- Interest Arbitrage: Balance transfer cards allow consumers to move high-interest debt to 0% APR windows, typically lasting 12-21 months, effectively pausing interest accrual.

- Banking Risk: Rising delinquency rates among low-to-moderate income borrowers are forcing lenders to increase loan loss provisions, potentially impacting quarterly EPS.

- Consumption Drag: As a higher percentage of monthly income is diverted to debt service, forward guidance for consumer discretionary stocks is likely to remain conservative.

The Math of the Interest Rate Squeeze

To understand why low-interest cards are currently a strategic necessity, one must look at the compounding nature of credit card debt. Most standard cards now carry APRs ranging from 21% to 29%. At these levels, a consumer paying only the minimum requirement is not paying down the principal; they are merely servicing the interest.

But the balance sheet tells a different story when a balance transfer is introduced. By shifting a balance to a card with a 0% introductory rate, the borrower converts a revolving debt instrument into a temporary interest-free loan. Here is the math: on a $10,000 balance at a 24% APR, the monthly interest charge is approximately $200. Over a year, that is $2,400 in non-equity-building payments.

Even with a typical balance transfer fee of 3% to 5%, the cost of the move (roughly $300 to $500) is a fraction of the annual interest expense. This creates a window for aggressive principal reduction. However, this strategy requires a credit score typically above 670 to secure the most competitive offers from issuers like Citigroup (NYSE: C).

| Debt Amount | Standard APR (24%) Annual Interest | 0% Transfer Card (4% Fee) Annual Cost | Net Annual Savings |

|---|---|---|---|

| $5,000 | $1,200 | $200 | $1,000 |

| $10,000 | $2,400 | $400 | $2,000 |

| $20,000 | $4,800 | $800 | $4,000 |

How Credit Delinquencies Pressure Banking Valuations

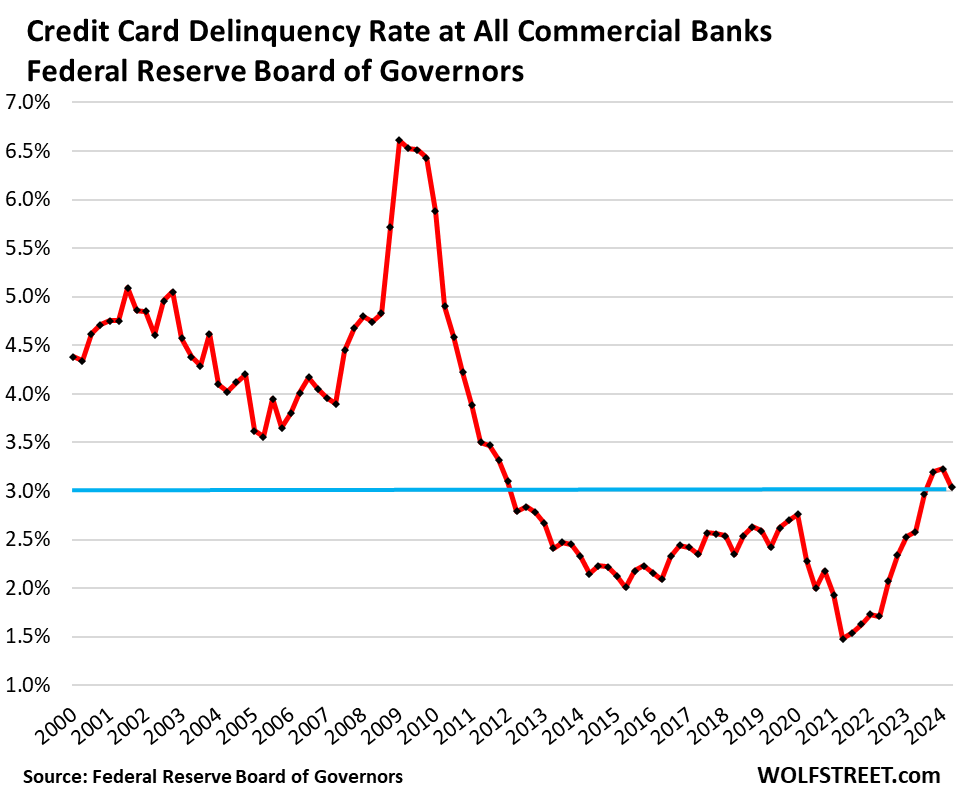

The rise in APRs has a symbiotic, yet dangerous, relationship with banking profitability. Although higher rates increase the Net Interest Margin (NIM) for lenders, they simultaneously increase the probability of default. We are seeing this play out in the latest data from the Federal Reserve Bank of Recent York, which indicates that credit card delinquency rates are trending upward, particularly in the 25-39 age demographic.

For institutions like Capital One (NYSE: COF) and Discover Financial (NYSE: DFS), which have significant exposure to unsecured consumer credit, this creates a volatility paradox. Higher rates boost short-term revenue, but if the consumer hits a breaking point, the resulting write-offs can erase those gains. This is why institutional investors are closely monitoring “Net Charge-Off” (NCO) rates in SEC filings.

“The consumer has been remarkably resilient, but we are reaching the limit of excess savings. When the cost of debt begins to outpace wage growth, the risk of a systemic credit contraction increases significantly.”

This sentiment is echoed across Wall Street, where analysts are weighing the strength of the labor market against the eroding purchasing power of the middle class. If the unemployment rate ticks upward while APRs remain elevated, the “balance transfer” strategy will shift from a savvy financial move to a survival mechanism for millions.

The Macroeconomic Ripple Effect on Consumer Spending

The impact of rising APRs extends far beyond the banking sector. It acts as a stealth tax on the consumer. When a household spends an additional $200 a month on interest, that is $200 removed from the local economy—money that would have otherwise gone to retailers, restaurants, or service providers.

This contraction in discretionary spending affects the valuation of companies like Amazon (NASDAQ: AMZN) and Walmart (NYSE: WMT). While Walmart often benefits from “trade-down” behavior—where consumers switch from premium brands to generic ones—a systemic debt crisis reduces the overall volume of transactions. We are seeing a correlation between rising credit utilization rates and a decline in average order value (AOV) across e-commerce platforms.

the regulatory environment is tightening. The Consumer Financial Protection Bureau (CFPB) has increased scrutiny on “junk fees” and predatory interest practices. This regulatory pressure, combined with the need to maintain liquidity, may force banks to tighten credit standards, making it harder for the average consumer to access the very low-interest cards they need to deleverage.

Navigating the 2026 Credit Landscape

As we move further into the second quarter of 2026, the strategy for debt management must be surgical. The goal is not simply to move debt, but to eliminate it before the introductory period expires. A common failure in balance transfer strategies is the “revolving door” effect, where the borrower moves the debt to a 0% card but continues to spend on the original account, effectively doubling their total liability.

For a sustainable recovery, consumers must align their repayment schedule with the expiration date of the 0% offer. For example, a $12,000 balance on a 12-month 0% APR card requires a monthly payment of exactly $1,000 to avoid a return to high-interest compounding. Those who cannot meet this threshold may need to explore debt consolidation loans, which offer fixed rates and structured timelines, though often at a higher cost than a 0% card.

Looking ahead, the market trajectory suggests that while the Federal Reserve may eventually pivot toward rate cuts, the “lag effect” means consumer APRs will remain elevated for some time. The ability of the US economy to avoid a hard landing depends on whether consumers can successfully deleverage without a collapse in overall spending. For now, the balance transfer remains the most efficient tool for the individual to decouple their financial health from the volatility of the prime rate.

For further tracking of interest rate trends and banking stability, refer to the Bloomberg Terminal data or the latest SEC EDGAR filings for major credit issuers.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.