The mood on the trading floors of Lower Manhattan shifted in a heartbeat this morning. One moment, the consensus was a comfortable glide toward rate cuts; the next, a single data release from the Bureau of Labor Statistics acted like a bucket of ice water to the face of every bond trader in the room. The U.S. Jobs report didn’t just beat expectations—it shattered them, dragging the market back into a cold, familiar reality where inflation is the primary antagonist and the Federal Reserve is the only one with the weapon to fight it.

This isn’t just a blip in the spreadsheets. When the labor market refuses to cool, it creates a feedback loop that keeps wages high, which in turn keeps prices sticky. For investors who had already priced in a dovish pivot from the Fed, this “surprise employment” surge is a brutal reminder that the road to price stability is rarely a straight line. We are seeing a violent repricing of risk in real-time, as the market pivots from betting on cuts to hedging against further hikes.

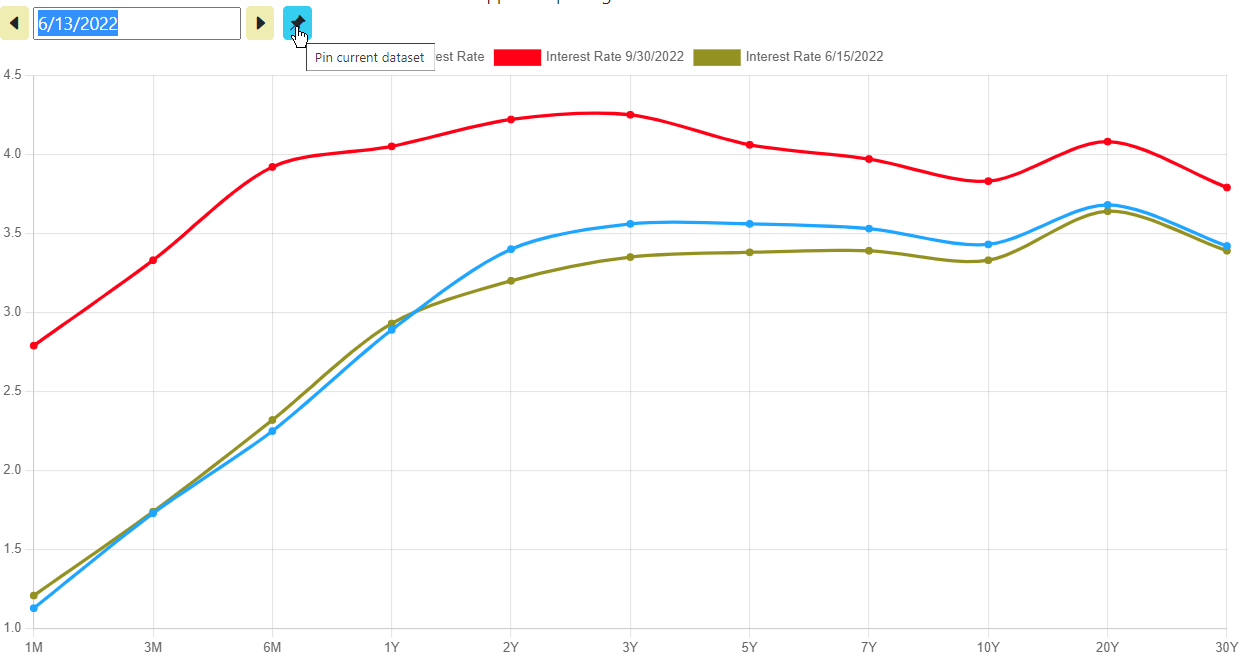

The Anatomy of a Bear Flattening

To the uninitiated, the phrase “bear flattening” sounds like financial jargon designed to confuse. To an insider, it’s a clear signal of distress and anticipation. In simple terms, we are seeing the short complete of the yield curve—the two-year and five-year notes—surge much faster than the long-term bonds. This happens due to the fact that short-term yields are hyper-sensitive to the Federal Reserve’s immediate policy moves. When the market suddenly expects the Fed to keep rates higher for longer, or even hike them, the short end spikes.

The “bear” part of the term refers to the falling price of the bonds (since yields and prices move in opposite directions). The “flattening” occurs because the gap between short-term and long-term rates narrows. This specific curve movement suggests that while the market fears immediate inflation and aggressive Fed action, there is still a lingering doubt about long-term growth. It is a precarious state of affairs; the market is essentially screaming that the Fed is behind the curve.

This volatility is deeply rooted in the Federal Reserve Board‘s dual mandate: maintaining price stability while maximizing employment. For the last year, the Fed has been trying to balance these two. But when employment remains this robust, the “maximum employment” side of the equation begins to threaten the “price stability” side. We are witnessing the return of the wage-price spiral fear, where companies raise prices to cover the higher wages they must pay to attract talent in a tight labor market.

Why the Labor Market Refuses to Break

The core question haunting the desks today is simple: Why is the U.S. Economy still this hot? Traditional economic theory suggests that after a prolonged period of high interest rates, we should spot a noticeable cooling in hiring. Yet, the Bureau of Labor Statistics continues to report numbers that defy gravity. This resilience is likely a cocktail of post-pandemic structural shifts and a massive surge in productivity driven by the integration of generative AI in white-collar sectors.

We are seeing a “labor hoarding” phenomenon. After the hiring nightmares of 2021 and 2022, many firms are terrified of letting go of skilled workers, even as growth slows. This creates a floor for employment that prevents the “cooling” the Fed so desperately wants to see. When you combine this with a shrinking pool of available workers due to aging demographics, you get a market where the employer has lost all leverage, and the employee holds all the cards.

“The resilience of the labor market is a double-edged sword. While it supports consumer spending and prevents a deep recession, it simultaneously removes the primary mechanism the Fed uses to dampen inflation. We are effectively fighting a tide that refuses to go out.”

This sentiment is echoed across the street. The danger here is that the Fed may be forced to over-tighten. If they keep hiking or holding rates at these peaks to kill the labor heat, they risk snapping the economy’s spine rather than gently bending it. The “soft landing” narrative—the holy grail of the current economic cycle—is looking increasingly like a fairy tale.

The Global Ripple Effect and the Dollar Trap

The fallout from a “higher-for-longer” U.S. Rate environment doesn’t stop at the border. When U.S. Treasury yields spike, the U.S. Dollar typically strengthens as global capital floods into the highest-yielding, safest asset on earth. This creates a “Dollar Trap” for emerging markets. Countries that have borrowed in dollars now find their debt servicing costs skyrocketing, while their own currencies plummet in value.

According to analysis from the International Monetary Fund, this divergence in monetary policy can lead to severe capital flight from developing nations. As the U.S. Pulls the world’s liquidity back into its own shores to fight domestic inflation, the rest of the world is left to deal with “imported inflation”—where the cost of essential imports, priced in dollars, rises simply because their local currency has weakened.

the U.S. Department of the Treasury is facing its own challenge. With yields rising, the cost for the U.S. Government to service its own massive national debt increases. Every basis point jump in the 10-year yield translates to billions of additional dollars in interest payments, potentially crowding out other federal spending and adding another layer of fiscal instability to an already volatile political climate.

Navigating the Latest Rate Reality

For the average investor, the takeaway is clear: the era of “easy money” isn’t just over; it’s being actively erased. The market’s bet on a quick return to low rates was a gamble based on a hope that inflation would vanish quietly. Instead, inflation is proving to be a stubborn guest that refuses to leave the party.

The immediate strategy for the coming quarter is defensive. Diversification is no longer just a suggestion; it’s a survival mechanism. With the yield curve flattening and the Fed in a corner, volatility will be the only constant. We are moving into a phase where “real yield” (the nominal rate minus inflation) is the only metric that truly matters. If inflation remains sticky while rates rise, the real return on bonds remains unattractive, pushing investors toward hard assets or high-quality equities with strong pricing power.

The big question now is whether the Fed has the stomach for one more hike. If they blink, inflation could become entrenched, leading to a decade of stagnation. If they act, they might trigger the incredibly recession they’ve spent two years trying to avoid. It is a high-stakes game of chicken, and the bond market is currently betting that the Fed will choose the pain of a recession over the shame of failed inflation targets.

Carter’s Closing Thought: We’ve spent months talking about the “pivot.” It turns out the pivot was a mirage. The real story is the resilience of the American worker and the stubbornness of the CPI. As we watch the yields climb, ask yourself: is the economy actually “strong,” or are we just seeing the final, frantic burst of a bubble before the pin finally hits? I’d love to hear your capture—are you hedging for a crash or betting on a miracle? Let’s discuss in the comments.