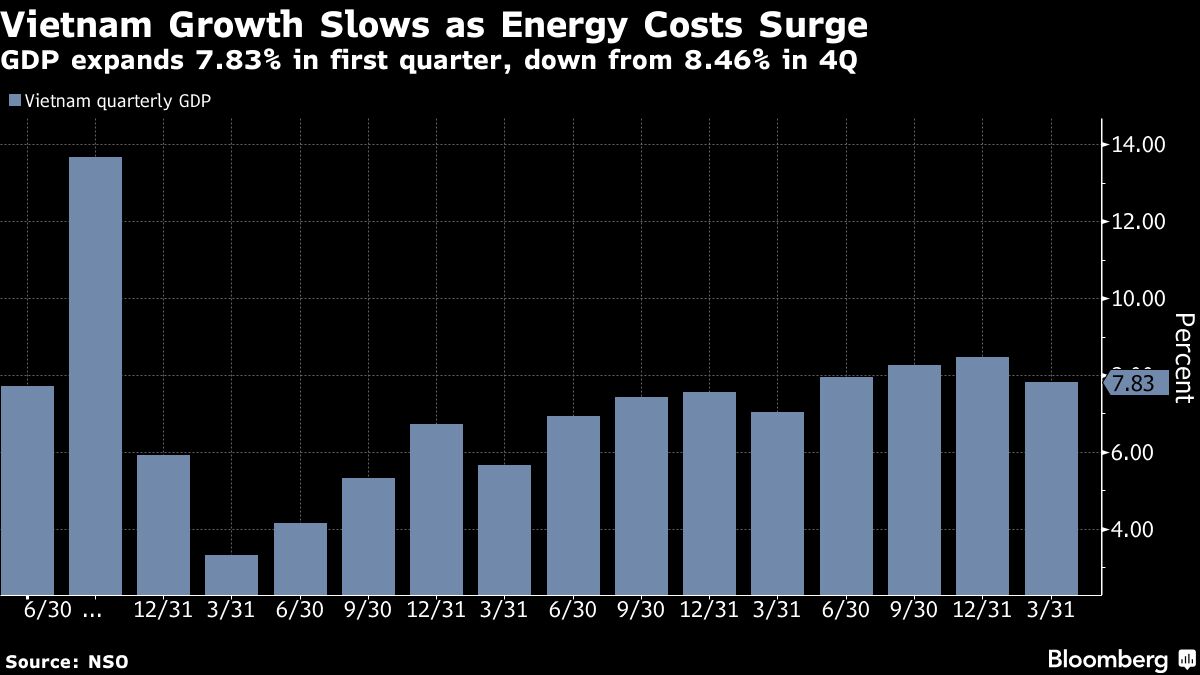

Vietnam’s Q1 2026 economic growth decelerated as Middle East geopolitical tensions inflated energy costs and disrupted critical shipping lanes. This slowdown complicates General Secretary To Lam’s double-digit growth ambitions, threatening manufacturing margins and increasing inflationary pressure across the primary Southeast Asian hub for global supply chain diversification.

This deceleration is not a localized anomaly; We see a systemic warning for the “China+1” strategy. For years, multinational corporations have shifted production to Vietnam to mitigate geopolitical risk in East Asia. However, the current volatility in energy markets proves that geographic diversification does not grant immunity from global macroeconomic shocks. When the cost of powering a factory rises and the cost of shipping the finished product increases, the competitive advantage of low-cost labor evaporates.

The Bottom Line

- Energy Vulnerability: Rising global crude and LNG prices are squeezing margins for energy-intensive manufacturing, forcing a reassessment of operational costs.

- Logistics Friction: Trade route disruptions in the Middle East have increased freight lead times and insurance premiums, impacting export volumes to the EU and North America.

- Policy Conflict: The State Bank of Vietnam (SBV) faces a tightening corridor between stimulating growth and managing currency depreciation against a strong US Dollar.

The Energy Math Behind the Margin Squeeze

Vietnam’s industrial sector is heavily reliant on imported energy to fuel its export-oriented growth. As tensions in the Middle East persist, the landed cost of energy has created a direct headwind for the manufacturing sector. But the balance sheet tells a different story than the official growth targets.

For companies like Samsung Electronics (KRX: 005930), which operates massive production hubs in Vietnam, energy price volatility introduces unpredictability into quarterly guidance. When energy inputs rise by 12% to 15%, the ability to absorb those costs without raising wholesale prices is limited. This is particularly acute in the garment and electronics sectors, where contracts are often fixed long-term.

Here is the math: a sustained 10% increase in energy costs typically correlates with a 0.5% to 0.8% drag on GDP growth for energy-importing emerging markets. For a country aiming for double-digit growth, these fractional losses are catastrophic to the final target.

| Metric | Q1 2025 (Actual) | Q1 2026 (Est.) | Variance (%) |

|---|---|---|---|

| GDP Growth (YoY) | 6.8% | 5.2% | -23.5% |

| CPI Inflation | 3.4% | 4.1% | +20.5% |

| Energy Import Cost | $12.4B | $14.1B | +13.7% |

| FDI Inflow (Net) | $18.2B | $17.5B | -3.8% |

Shipping Bottlenecks and the Export Paradox

Vietnam’s economy is an export machine. However, that machine requires clear arteries. The disruption of global trade routes has effectively added a “geopolitical tax” to every container leaving the port of Hai Phong or Ho Chi Minh City. Freight rates for Asia-to-Europe routes have seen significant volatility, forcing exporters to either eat the cost or risk losing market share to regional competitors with shorter supply chains.

This logistics friction is impacting the valuation of shipping and logistics firms. Even as global carriers like Maersk (CPH: MAERSK-B) may observe short-term revenue gains from higher spot rates, the actual volume of goods moving out of Vietnam is stagnating. This creates a paradox: higher shipping costs are not translating to higher profits for Vietnamese firms, but rather to diminished demand in Western markets due to landed-price inflation.

“The narrative that Vietnam is a safe harbor from global volatility is being tested. We are seeing a shift where investors are no longer just looking at labor costs, but at the resilience of the energy grid and the reliability of the trade corridors.”

— Marcus Thorne, Senior Emerging Markets Strategist at a leading global institutional fund.

To Lam’s Growth Ambition vs. Macroeconomic Reality

General Secretary To Lam has signaled a desire for double-digit growth—a bold target that requires a perfect alignment of domestic policy and global demand. However, the current environment is far from perfect. The World Bank has frequently cautioned that infrastructure bottlenecks remain a primary constraint on Vietnam’s long-term potential.

To achieve 10% growth, Vietnam would need a massive surge in high-value-added manufacturing and a significant increase in domestic consumption. But rising energy costs act as a regressive tax on the population, eating into disposable income and slowing the growth of the domestic retail sector. The result is a reliance on Foreign Direct Investment (FDI) that is becoming increasingly sensitive to global risk appetite.

the relationship between the State Bank of Vietnam and the Federal Reserve remains a critical point of failure. If the US maintains higher interest rates for longer to combat its own inflation, the Vietnamese Dong faces downward pressure. To prevent capital flight, the SBV may be forced to raise rates, which would further stifle the very growth To Lam is attempting to accelerate.

The FDI Ripple Effect and Corporate Strategy

The slowdown is creating a divergence in how multinationals approach the region. While Intel (NASDAQ: INTC) and other semiconductor players continue to view Vietnam as a strategic pivot, the “burn rate” for new infrastructure projects is increasing. Capital expenditure (CapEx) is being scrutinized more heavily as the cost of borrowing and the cost of energy rise.

We are seeing a transition from “rapid expansion” to “optimized expansion.” Companies are no longer just building more factories; they are investing in on-site renewable energy to hedge against the volatility of the national grid. This shift indicates that the private sector is preparing for a prolonged period of energy uncertainty.

But the real risk lies in the mid-tier suppliers. Small and medium enterprises (SMEs) that feed into the supply chains of giants like Apple (NASDAQ: AAPL) do not have the balance sheets to absorb a 15% increase in energy overheads. If these suppliers fail, the entire production ecosystem is compromised, regardless of how much capital the anchor tenants invest.

The Forward Trajectory: Adaptive Growth

Vietnam will not stop growing, but the era of “easy growth” driven solely by the exodus from China is ending. The market is entering a phase of adaptive growth. To regain momentum, the government must accelerate its energy transition and modernize its ports to reduce reliance on volatile global corridors.

For investors, the play is no longer a broad bet on Vietnam as a country, but a surgical bet on companies that have decoupled their energy needs from the global grid and those with diversified shipping partnerships. The growth will still happen, but it will be slower, more expensive, and far more selective.

As markets open on Monday, expect a cautious sentiment toward Southeast Asian equities as analysts bake in the higher energy costs for the remainder of the fiscal year. The “Vietnam Miracle” is not over, but it is currently undergoing a necessary and painful stress test.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.