:max_bytes(150000):strip_icc()/what-is-a-fixed-rate-mortgage-3305929-Final2-3c46c75609a940939cca58b8e47f669f.png)

Mortgage and refinancing rates in March 2026 remain elevated, tethered to persistent Treasury yield volatility and inflation expectations. Fixed-rate structures lock costs for borrowers, mitigating long-term risk despite higher initial entry points. Refinancing activity contracts as spreads widen, impacting consumer liquidity and housing turnover. This analysis dissects the capital allocation implications for homeowners and institutional investors navigating the current yield environment.

The distinction between fixed and variable debt instruments is not merely semantic; We see a fundamental determinant of household balance sheet resilience. When markets price in sustained inflationary pressure, the cost of borrowing capital shifts from a temporary hurdle to a structural component of financial planning. For the broader economy, housing finance conditions act as a transmission mechanism for monetary policy. As the Federal Reserve maintains its stance on price stability, the secondary mortgage market absorbs the shock, translating bond market volatility into monthly payments for consumers. This dynamic restricts disposable income, subsequently cooling retail spending and construction sector growth.

The Bottom Line

- Capital Cost Stability: Fixed-rate mortgages insulate borrowers from yield curve fluctuations, preserving cash flow predictability despite higher initial premiums.

- Refinancing Contraction: Elevated baseline rates reduce refinancing volume by approximately 40% compared to low-rate cycles, limiting equity extraction opportunities.

- Macro Drag: Persistent housing finance costs suppress consumer discretionary spending, creating headwinds for retail and home improvement sectors.

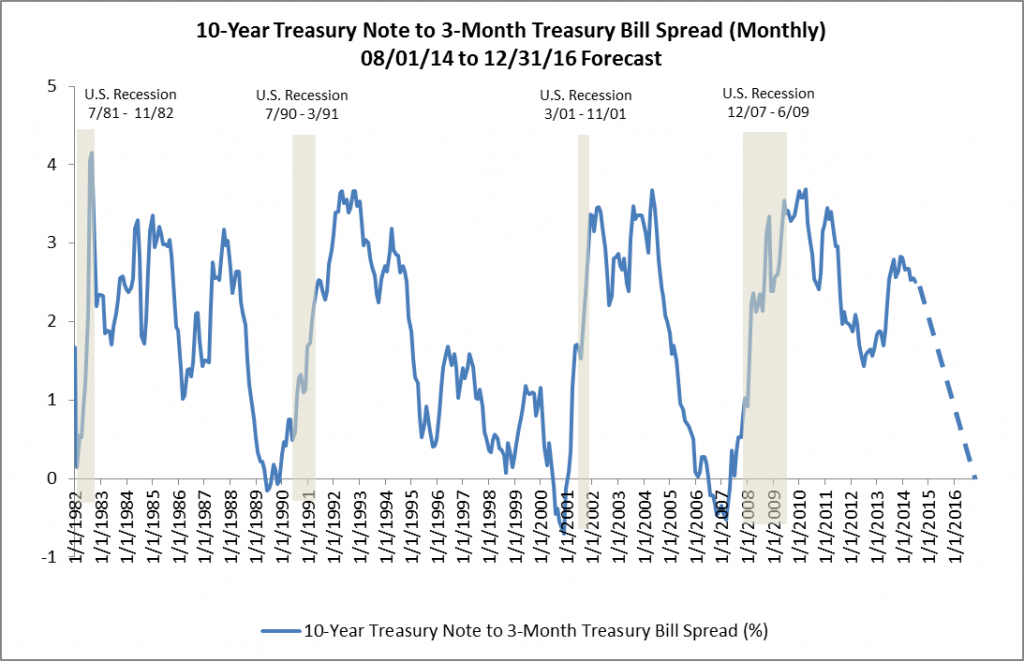

The Treasury Spread and Pricing Mechanics

Understanding the pricing of residential debt requires analyzing the spread between the 10-year Treasury note and conventional mortgage rates. Historically, this spread averages around 150 to 200 basis points. However, in periods of market uncertainty or liquidity constraints, this gap widens. Lenders price in risk premiums to hedge against prepayment speeds and interest rate volatility. Here is the math: if the 10-year yield sits at 4.5%, a standard conforming loan often prices near 6.5% to cover servicing costs and credit risk.

Investors monitoring this sector must watch the Bloomberg Fixed Income data for real-time yield movements. When the yield curve inverts or steepens unpredictably, mortgage-backed securities (MBS) develop into less attractive to institutional buyers like BlackRock (NYSE: BLK) or Vanguard. This reduced demand forces originators to pass costs to the borrower. The source material notes that fixed rates lock costs for the loan’s viability, such as 30 years. This duration mismatch creates asset-liability management challenges for banks holding these loans on their balance sheets.

Refinancing Volume and Equity Liquidity

The refinancing market serves as a critical release valve for consumer equity. When rates rise, the incentive to refinance diminishes unless home values appreciate significantly enough to justify cash-out transactions. In the current 2026 landscape, refinancing applications have stabilized at lower volumes. This reduction limits the ability of homeowners to consolidate higher-interest consumer debt into lower-interest secured debt. Unsecured debt levels may rise, impacting credit card delinquency rates across major issuers like JPMorgan Chase (NYSE: JPM).

Consider the following comparison of debt structures in the current environment:

| Metric | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest Risk | Borrower Protected | Borrower Exposed |

| Initial Rate | Higher Premium | Lower Teaser Rate |

| Payment Stability | Constant Principal & Interest | Variable After Initial Period |

| Refinance Dependency | Low | High |

But the balance sheet tells a different story. Homeowners opting for Adjustable-Rate Mortgages (ARMs) to lower initial payments face reset risk in years three, five, or seven. If rates remain elevated by 2029 or 2031, payment shock could trigger defaults. This systemic risk is monitored closely by rating agencies and regulators. For more on housing finance data, refer to the Freddie Mac Primary Mortgage Market Survey.

Consumer Spending and Macro Headwinds

Housing costs constitute the largest component of consumer expenditure. When mortgage rates remain high, the marginal propensity to consume declines. Families allocate a larger percentage of monthly income to debt service, leaving less for discretionary categories such as travel, dining, and retail. This shift directly impacts earnings guidance for consumer-facing corporations. Retailers often adjust inventory levels based on this reduced liquidity, creating a ripple effect through supply chains.

Labor markets similarly feel the strain. The construction sector, highly sensitive to housing starts, may see slower hiring growth if mortgage demand suppresses modern home purchases. This cooling effect can inadvertently assist the Federal Reserve in managing inflation by reducing aggregate demand. However, it also risks tipping regional economies into recession if housing activity stalls too abruptly. The Federal Reserve monitors these indicators closely to adjust open market operations.

Institutional investors recognize this correlation. As noted by industry leaders, the housing market remains a primary transmission channel for monetary policy.

“Housing sensitivity to interest rates is the most direct link between Fed policy and the real economy. When financing costs rise, transaction volumes fall, and wealth effects diminish.”

This perspective underscores why mortgage rates are not just a consumer issue but a macroeconomic signal. For further reading on economic indicators, consult the Wall Street Journal Market Data.

Strategic Positioning for the Next Cycle

For business owners and investors, the current rate environment demands a shift in strategy. Capital allocation should prioritize efficiency over expansion. Debt refinancing should only be pursued if the spread justification is clear and closing costs are amortized quickly. Equity positions in homebuilding firms or mortgage REITs require careful stress testing against further yield curve shifts. The era of cheap capital has paused, requiring a return to fundamentals-based valuation.

Looking ahead, the trajectory of rates depends on inflation data and fiscal policy. If government spending remains unchecked, bond vigilantes may push yields higher, forcing mortgage rates up alongside them. Conversely, if productivity gains from AI and technology offset inflationary pressures, rates could stabilize. Investors must remain agile, monitoring the U.S. Department of the Treasury auction results for signals of demand. The prudent path involves locking in costs where possible and maintaining liquidity reserves to weather potential volatility in the consumer sector.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.