Geopolitical tensions, specifically the escalating situation in Iran, are prompting a reassessment of dollar-denominated debt by several nations. Concerns over potential sanctions and restricted access to the U.S. Financial system are driving governments to explore alternatives, potentially impacting global currency dynamics and U.S. Treasury yields. This shift, while nascent, could accelerate de-dollarization trends already observed in emerging markets.

The Financial Times’ reporting on this matter highlights a growing unease, but stops short of quantifying the potential impact on U.S. Debt markets or outlining specific strategies being considered by these governments. The core question isn’t simply *if* nations will reduce dollar exposure, but *how* and *at what pace*. This is a critical distinction for investors assessing risk and opportunity.

The Bottom Line

- Reduced Demand for U.S. Treasuries: Increased diversification away from dollar debt could lead to a decline in demand for U.S. Treasury bonds, potentially pushing yields higher and impacting borrowing costs for the U.S. Government.

- Strengthening Alternative Currencies: The Euro, Yuan, and other currencies could benefit from increased adoption as reserve currencies, altering the global financial landscape.

- Increased Volatility in FX Markets: A flight from the dollar, even a partial one, is likely to introduce increased volatility in foreign exchange markets, creating both risks and opportunities for traders.

The Mechanics of De-Dollarization: Beyond Rhetoric

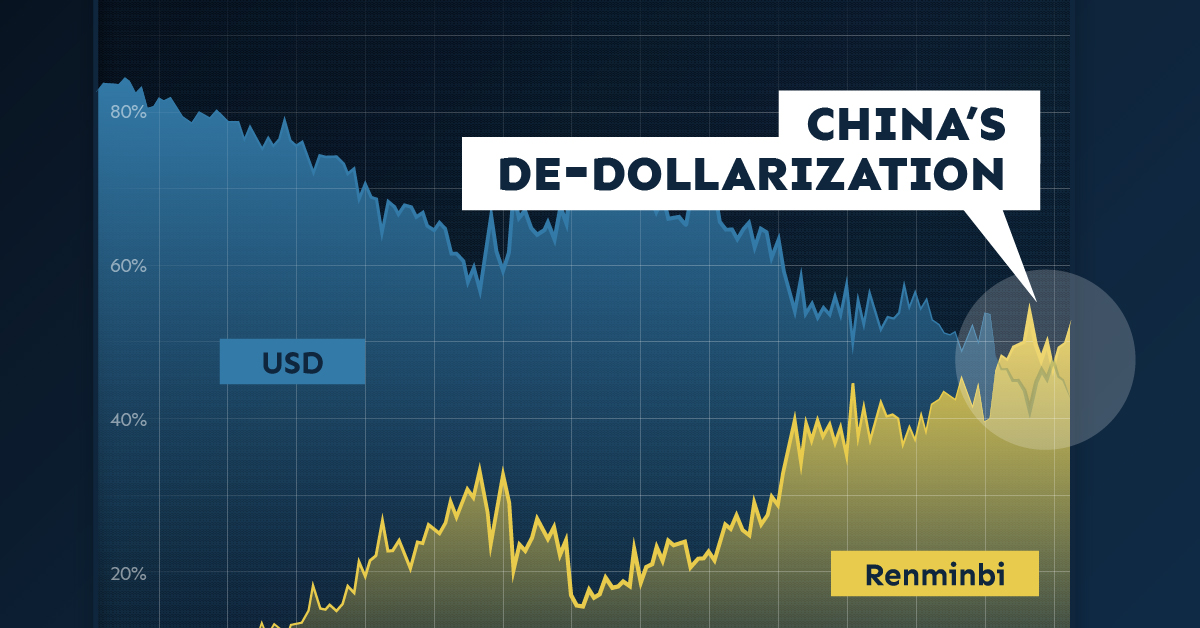

The discussion around de-dollarization isn’t new. For years, countries like Russia and China have actively sought to reduce their reliance on the U.S. Dollar in international trade. However, the potential for a more widespread shift, triggered by geopolitical instability, is what’s now capturing market attention. Currently, the U.S. Dollar accounts for roughly 59.1% of global foreign exchange reserves, according to the IMF. A significant erosion of this share would have far-reaching consequences.

Here is the math. The total global foreign exchange reserves are estimated at around $14.6 trillion (as of Q4 2025). A 5% shift away from the dollar would equate to a $730 billion reduction in demand for dollar-denominated assets. This doesn’t necessarily mean a direct sale of U.S. Treasuries, but rather a gradual reduction in new purchases and a preference for alternative currencies in trade settlements.

Impact on U.S. Treasury Yields and the Debt Ceiling

The timing of this potential shift is particularly sensitive. The U.S. Is already grappling with a substantial national debt – exceeding $34.6 trillion as of March 2026, according to US Debt Clock – and ongoing debates surrounding the debt ceiling. Reduced demand for U.S. Treasuries could exacerbate these challenges, forcing the Treasury to offer higher yields to attract investors. This, in turn, would increase the cost of servicing the national debt.

But the balance sheet tells a different story. While a decline in foreign demand is a concern, domestic demand for U.S. Debt remains relatively strong, particularly from pension funds and insurance companies. However, this domestic demand may not be sufficient to fully offset a significant outflow of foreign capital.

Competitor Reactions and Currency Dynamics

The potential beneficiaries of a weakening dollar are primarily the Euro and the Chinese Yuan. The Eurozone, with a combined GDP of approximately $17.7 trillion (2025 estimate, Statista), represents a significant economic bloc. Increased adoption of the Euro in international trade could strengthen its position as a reserve currency. However, the Eurozone also faces its own economic challenges, including high inflation and varying levels of fiscal discipline among member states.

China’s Yuan, while gaining traction, still faces hurdles related to capital controls and a lack of full convertibility. However, China’s Belt and Road Initiative and its growing economic influence are gradually increasing the Yuan’s prominence in global trade.

“We are seeing a subtle but definite shift in sentiment towards diversifying away from the dollar, particularly among countries that feel vulnerable to U.S. Foreign policy,” says Dr. Eleanor Vance, Chief Economist at Global Macro Advisors. “This isn’t about a complete abandonment of the dollar, but rather a prudent risk management strategy.”

Sector-Specific Impacts: Energy and Commodities

The energy and commodities markets are particularly sensitive to currency fluctuations. Many commodities, such as oil and gold, are priced in U.S. Dollars. A weaker dollar could make these commodities more affordable for buyers using other currencies, potentially boosting demand. However, it could also lead to inflationary pressures in the U.S. As import prices rise.

Chevron (NYSE: CVX), for example, derives a significant portion of its revenue from international sales. A weaker dollar could positively impact Chevron’s earnings when translated back into U.S. Dollars. Conversely, **ExxonMobil (NYSE: XOM)**, while also benefiting from higher commodity prices, could face increased competition from producers in countries with stronger currencies.

| Company | Ticker | Q4 2025 Revenue (USD Billions) | Q4 2025 Net Income (USD Billions) | 2026 YTD Stock Performance (%) |

|---|---|---|---|---|

| Chevron | CVX | 58.5 | 9.2 | +8.7% |

| ExxonMobil | XOM | 84.1 | 11.4 | +6.2% |

| TotalEnergies | TTE | 75.3 | 8.1 | +12.5% |

The Role of BRICS and Alternative Payment Systems

The BRICS nations (Brazil, Russia, India, China, and South Africa) have been actively promoting the use of their own currencies in trade settlements and exploring the creation of a new reserve currency. While the practical implementation of these initiatives remains challenging, they represent a long-term effort to reduce reliance on the U.S. Dollar. The development of alternative payment systems, such as China’s Cross-Border Interbank Payment System (CIPS), provides alternatives to the SWIFT network, which is dominated by Western financial institutions.

“The BRICS nations are not looking to replace the dollar overnight, but they are laying the groundwork for a more multipolar financial system,” explains James Carter, Head of Emerging Markets at BlackRock. “This is a gradual process, but it’s one that investors necessitate to pay attention to.”

Looking ahead, the trajectory of dollar debt will depend heavily on the evolution of geopolitical tensions, the economic performance of alternative currency blocs, and the willingness of nations to actively pursue de-dollarization strategies. The current situation demands a cautious approach, with investors closely monitoring developments and diversifying their portfolios accordingly. The potential for increased volatility in FX markets and U.S. Treasury yields is significant, creating both risks and opportunities for those prepared to navigate the changing landscape.

The coming months will be crucial. When markets open on Monday, investors will be scrutinizing any further statements from governments regarding their dollar debt holdings and trade settlement practices. Any concrete announcements of diversification efforts will likely trigger further market reactions.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*