Entrepreneurial success in high-cost markets like New York City is increasingly tied to intergenerational housing strategies. By utilizing rent-controlled apartments, young professionals are bypassing traditional residential overhead to fund commercial ventures, effectively leveraging family real estate as a seed-funding mechanism for small business startups in volatile urban economies.

This is not a narrative of domestic dependency; it is a calculated exercise in capital allocation. In a city where the cost of living often cannibalizes the ability to take professional risks, the “Rent-Controlled Arbitrage” provides a rare competitive advantage. When we analyze the balance sheet of a 28-year-old entrepreneur in Manhattan, the most critical line item isn’t their revenue—it is their burn rate. By eliminating the primary driver of that burn—market-rate rent—the barrier to entry for commercial ventures drops significantly.

The Bottom Line

- Capital Redirection: Rent-controlled housing acts as a synthetic seed round, allowing founders to divert 30-50% of their gross income from residential rent to commercial equity.

- Risk Mitigation: Low residential overhead provides a “safety blanket” that allows for longer runways in low-margin industries, such as fine art galleries.

- Macro Shift: Multigenerational living is evolving from a social necessity into a strategic financial hedge against urban inflation and high interest rates.

The Rent-Controlled Arbitrage and Capital Efficiency

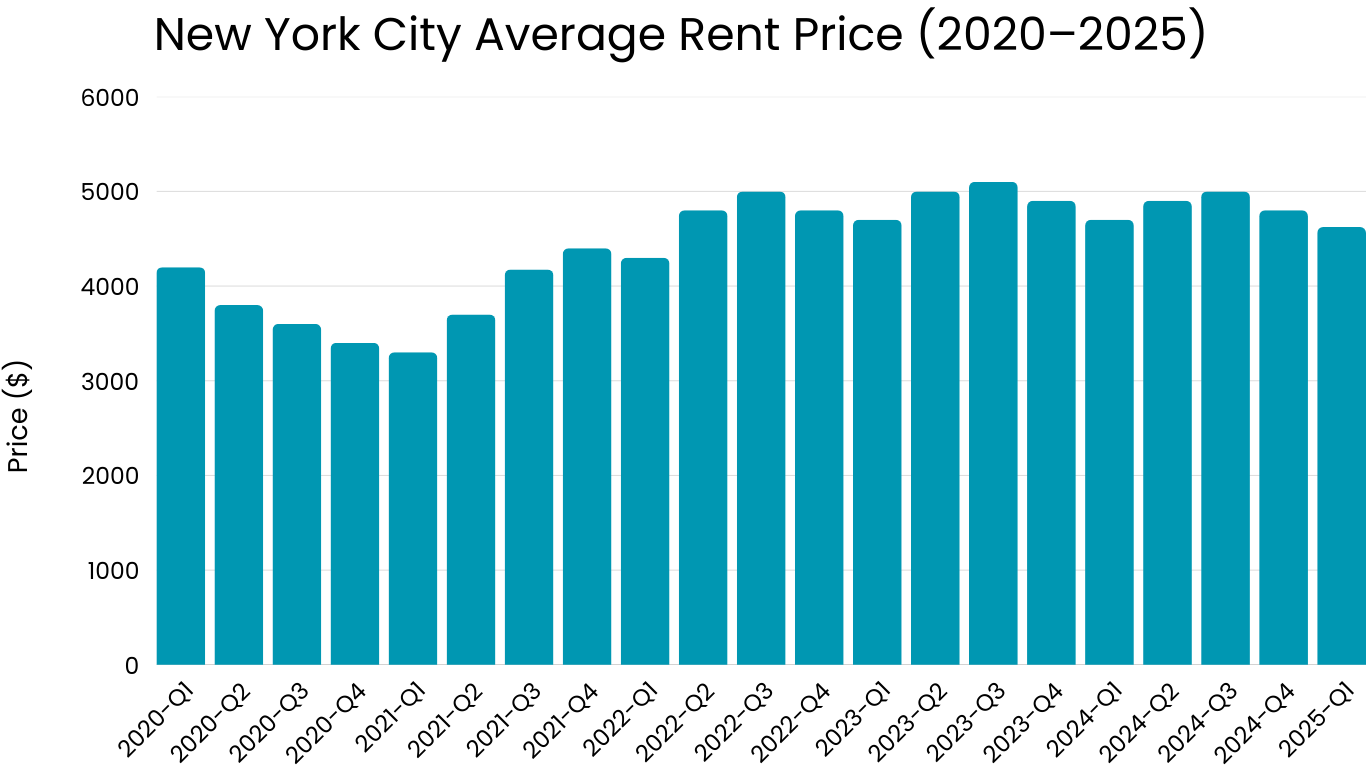

To understand the financial logic here, we must look at the delta between rent-stabilized/controlled units and the current market. As of the close of Q1 2026, median rents for a two-bedroom apartment in Manhattan have remained stubbornly high despite fluctuations in the broader economy. For a young couple, the difference between a market-rate lease and a legacy rent-controlled lease can exceed $3,000 per month.

Here is the math.

Over a 48-month period, that delta represents roughly $144,000 in saved liquidity. For a startup, this is the difference between failing in year one and surviving until a break-even point. In the case of the art gallery on the Lower East Side, this saved capital likely funded the initial security deposits and the first few months of a 10-year commercial lease—a commitment that would be prohibitively risky for someone paying $4,000 a month for a studio in Long Island City.

This strategy mirrors the “lean startup” methodology, but applies it to the founder’s personal life. By optimizing the residential cost center, the entrepreneur can sustain a higher burn rate on the business side. According to data tracked by CoStar Group (NASDAQ: CSGP), commercial real estate vacancies in NYC have fluctuated, but the fixed costs of a long-term lease remain a primary cause of small business insolvency.

| Expense Category | Market-Rate Scenario (Est.) | Rent-Controlled Scenario (Est.) | Annual Capital Gain/Saving |

|---|---|---|---|

| Monthly Rent (2BR Manhattan) | $5,200 | $1,100 | $49,200 |

| Annual Housing Cost | $62,400 | $13,200 | $49,200 |

| Available Business Seed Capital | Low/Debt-Reliant | High/Equity-Based | +$49,200 |

Commercial Real Estate Risk and the 10-Year Lease

Signing a 10-year commercial lease in Manhattan is a high-stakes gamble. Most small businesses fail within five years; committing to a decade of rent requires either massive capital reserves or an incredibly low personal cost of living. This is where the “family safety net” becomes a strategic asset.

But the balance sheet tells a different story when you factor in the “opportunity cost” of the parents’ time. The author mentions paying back their parents through household labor and IT support. In economic terms, this is an exchange of “sweat equity” for “housing equity.” The parents receive domestic services and care—which would otherwise cost thousands in professional home-care or concierge services—although the children receive a subsidized launchpad.

This symbiotic relationship is becoming a blueprint for the “Boomer-Millennial Wealth Transfer.” Rather than a lump-sum inheritance, wealth is being transferred via “living subsidies.” As noted by Bloomberg, the transfer of assets from baby boomers to their heirs is one of the largest shifts of wealth in human history, but it is increasingly happening through non-cash supports like co-habitation.

“The rise of multigenerational households in urban centers is not merely a response to a housing crisis, but a rational economic adaptation. We are seeing a strategic consolidation of resources that allows the younger generation to enter the market with less debt and more agility.”

Macroeconomic Headwinds and the Urban Flight Hedge

The decision to remain in New York City, rather than moving to a lower-cost borough or state, is a bet on the city’s enduring status as a global hub for art and finance. However, this bet is only viable if the residential cost is decoupled from the market. For those locked into rent-controlled units, the “urban flight” trend is irrelevant; they possess a legacy asset that grants them permanent residency at a fraction of the cost.

This creates a bifurcated economy in NYC. On one side, you have the “market-exposed,” who are vulnerable to interest rate hikes and inflation. On the other, you have the “legacy-protected,” who can weather economic downturns because their primary expense is fixed. This protection allows the legacy-protected to take risks—like opening an art gallery—that the market-exposed simply cannot afford.

As we look toward the second half of 2026, the viability of this model depends on the stability of rent-control laws. Any legislative shift toward deregulation would immediately increase the burn rate for thousands of urban entrepreneurs, potentially triggering a wave of small business closures. The relationship between housing policy and entrepreneurial activity is more direct than most policymakers realize.

The Strategic Takeaway

The “failure” of living at home is a social construct; the “success” of it is a financial reality. By treating housing as a strategic variable rather than a social milestone, the author has effectively engineered a low-risk environment for a high-risk business. For the modern entrepreneur, the most valuable asset isn’t always a venture capital check—sometimes, it is a rent-controlled lease and a supportive family structure.

Investors and analysts should view these multigenerational arrangements as a form of “informal venture capital.” As long as the cost of urban living continues to outpace wage growth, One can expect more professionals to prioritize balance sheet health over traditional markers of independence. The future of urban entrepreneurship may not be found in Silicon Valley’s dorms, but in the rent-controlled apartments of Manhattan.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.