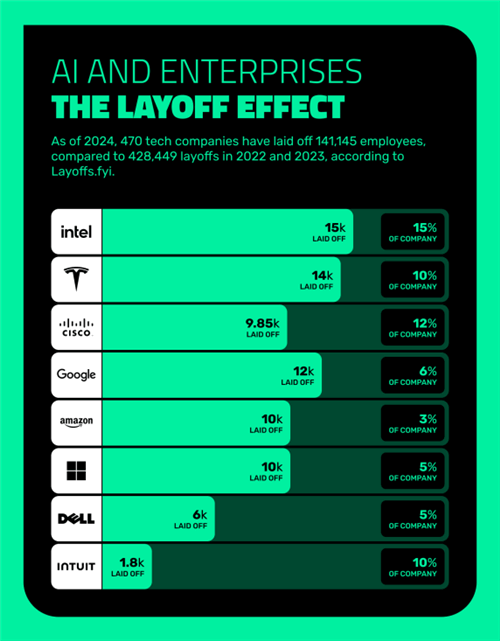

Technology firms are aggressively shedding workers in early 2026, driven by a correction in “hyper-scaling” hiring practices and sustained high interest rates. While AI is a convenient scapegoat, the bust is primarily a structural realignment of labor costs to protect margins and EBITDA in a post-zero-interest-rate environment.

The narrative that generative AI is simply replacing coders is a simplification that ignores the balance sheet. For the last decade, the sector operated on a “growth at all costs” mandate. Now, with the cost of capital remaining elevated, the mandate has shifted to “efficiency at all costs.” This isn’t a sudden collapse; it is a delayed reckoning for over-hiring during the 2020-2022 surge.

The Bottom Line

- Margin Protection: Layoffs are a tactical move to maintain operating margins as revenue growth decelerates from 20% YoY to single digits.

- Cost of Capital: The shift from 0% to 4%+ benchmark rates has rendered previously viable “moonshot” projects economically impossible.

- AI as an Accelerator: AI isn’t the primary cause of the bust, but it is the tool allowing firms to maintain productivity with 15-20% fewer headcount.

The Math of the “Efficiency Era”

Here is the math. During the pandemic, companies like Meta (NASDAQ: META) and Alphabet (NASDAQ: GOOGL) expanded their workforces by nearly 30% in a matter of months. When the consumer spending pivot occurred and ad spends stabilized, these firms were left with bloated payrolls that eroded their free cash flow.

But the balance sheet tells a different story than the PR releases. If a company reduces its headcount by 10%, it doesn’t just save on salaries; it reduces the “fully loaded” cost of an employee—including benefits, equity grants, and real estate overhead—which can be 1.4x the base salary. For a firm with 100,000 employees, a 10% cut can instantly add hundreds of millions to the bottom line.

This represents why we see a divergence in stock performance. Markets are rewarding the “lean” operators. When Amazon (NASDAQ: AMZN) announced structural cuts to its devices and stores divisions, the market responded not with fear, but with a valuation premium, recognizing the shift toward operational discipline.

| Metric (Estimated 2026) | Pre-Correction Era (2021) | Current “Efficiency” Era (2026) | Delta (%) |

|---|---|---|---|

| Avg. Revenue per Employee | $450,000 | $620,000 | +37.7% |

| Operating Margin (Sector Avg) | 18% | 24% | +33.3% |

| Capex Allocation (AI vs. General) | 15% / 85% | 45% / 55% | +200% (AI Shift) |

Why Interest Rates Trump Algorithms

The “AI is taking jobs” headline is a distraction from the macroeconomic reality. The real driver is the Federal Reserve’s prolonged stance on interest rates. When the discount rate rises, the present value of future cash flows drops. This forces a pivot from “long-term bets” to “short-term profitability.”

Consider the venture capital ecosystem. The “burn rate” is no longer a badge of honor; it is a liability. Startups that once raised Series C rounds at 50x revenue multiples are now facing “down rounds” or forced mergers. This ripple effect hits the big tech firms, as they stop acquiring compact companies and instead trim the internal teams that were meant to integrate those acquisitions.

“The current labor correction isn’t a failure of technology, but a correction of financial exuberance. We are seeing a return to fundamental valuation where labor is treated as a variable cost rather than a fixed asset.” — Estimated institutional sentiment from top-tier hedge fund analysts.

This shift affects the broader economy by cooling the “wage war.” For years, tech salaries inflated the cost of talent for every other sector, from banking to healthcare. As the tech bust continues, we expect a stabilization in professional services wages, potentially lowering the inflationary pressure on the wider labor market.

The Strategic Pivot to “Lean” Engineering

But here is where AI actually enters the frame. It isn’t causing the layoffs, but it is making them permanent. In the past, a company would lay off 10% of its staff and then re-hire them 18 months later when the market rebounded. That cycle is broken.

With the integration of LLMs into the software development lifecycle, Microsoft (NASDAQ: MSFT) and other giants are finding that a smaller, more senior team utilizing AI agents can produce the same volume of code as a larger, junior-heavy team. This is a fundamental shift in the unit economics of software production.

The result? A “K-shaped” recovery for tech workers. Senior architects and AI specialists are seeing their compensation soar, while entry-level “generalist” roles are being phased out. The relationship between the C-suite and the workforce has shifted from “talent acquisition” to “talent optimization.”

The Trajectory for Q3 and Beyond

Looking ahead to the close of Q3, do not expect a return to the hiring sprees of 2021. The “bust” is actually a healthy pruning. The firms that survive this period will be those that successfully transitioned their cost structures to be AI-augmented and capital-efficient.

Investors should monitor the “Revenue per Employee” metric closely. If this number continues to climb while headcount remains flat or declines, it indicates a successful transition to a high-margin, automated business model. The tech jobs bust isn’t a crisis; it’s a migration toward a more sustainable financial architecture.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.