U.S. Nonfarm payrolls increased by 178,000 in March 2026, surpassing market expectations and pushing the unemployment rate down to 4.3%. This labor market resilience suggests a “higher-for-longer” interest rate environment, putting immediate upward pressure on Treasury yields and strengthening the U.S. Dollar against global peers.

For the institutional investor, this data point is not merely a statistic on employment; It’s a signal of macroeconomic persistence. When the labor market refuses to cool despite aggressive tightening cycles, the **Federal Reserve (Fed)** loses its primary justification for pivoting toward rate cuts. This creates a friction point between equity valuations, which price in cheaper capital, and the reality of a stubborn labor market that fuels wage-push inflation.

The Bottom Line

- Rate Cut Delays: The probability of a Fed rate cut in the first half of 2026 has diminished, as 178,000 new jobs indicate an economy running above trend.

- Yield Pressure: The 2-year Treasury yield’s move toward 3.89% reflects a market repricing of the short-term cost of capital.

- Currency Divergence: The widening interest rate differential between the U.S. And Japan will likely sustain USD/JPY volatility, complicating hedging strategies for multinationals.

The 2-Year Yield and the Fed’s Policy Trap

The most immediate reaction to the March data was seen in the bond market. The 2-year Treasury yield, a primary barometer for near-term interest rate expectations, rose to 3.89%. This movement is a direct response to the “Information Gap” regarding the Fed’s reaction function. Although the headline number of 178,000 is not an explosion in hiring, the fact that it exceeded forecasts suggests that the labor market is not yet at a breaking point.

Here is the math: when employment remains strong, consumer spending—which accounts for roughly 70% of U.S. GDP—stays robust. This robustness prevents the Consumer Price Index (CPI) from returning to the 2% target rapidly. The **Federal Reserve** is trapped; cutting rates too early risks a second wave of inflation, but holding them high risks a delayed “hard landing.”

But the balance sheet tells a different story for corporations. For companies like Microsoft (NASDAQ: MSFT) or Alphabet (NASDAQ: GOOGL), the cost of servicing debt is less of a concern than the valuation of future cash flows. Higher discount rates, driven by rising yields, compress the present value of those future earnings, which typically leads to a contraction in P/E ratios for growth stocks.

| Metric | Market Forecast | Actual (March 2026) | Variance |

|---|---|---|---|

| Nonfarm Payrolls | ~140,000 – 160,000 | 178,000 | +18,000 to +38,000 |

| Unemployment Rate | 4.4% | 4.3% | -0.1% |

| 2-Year Treasury Yield | 3.75% (Avg) | 3.89% | +14 bps |

The USD/JPY Nexus and Global Capital Flows

The currency markets reacted with predictable precision. A stronger-than-expected jobs report typically triggers a “risk-off” move in the Yen as traders bet on a widening yield gap. While the initial move in the USD/JPY pair was described as limited, the underlying structural pressure remains. The Bank of Japan (BoJ) is operating in a completely different paradigm, attempting to nudge rates upward from near-zero, while the U.S. Is fighting to bring rates down from a peak.

This divergence creates a significant headwind for Japanese exporters and financial institutions like Mitsubishi UFJ Financial Group (NYSE: MUFG), which must navigate the volatility of carry trades. When the 2-year yield hits 3.89%, the incentive to hold Dollars over Yen increases, effectively exporting U.S. Monetary tightness to the rest of the world.

“The resilience of the U.S. Labor market is the primary obstacle to a synchronized global easing cycle. As long as nonfarm payrolls beat expectations, the dollar remains the default safe haven, regardless of the underlying fiscal deficits.”

To understand the broader implications, one must look at the Bloomberg Terminal data on capital flows. We are seeing a rotation out of emerging market equities and back into U.S. Treasuries, not since the U.S. Economy is “safe,” but because the yield is too attractive to ignore.

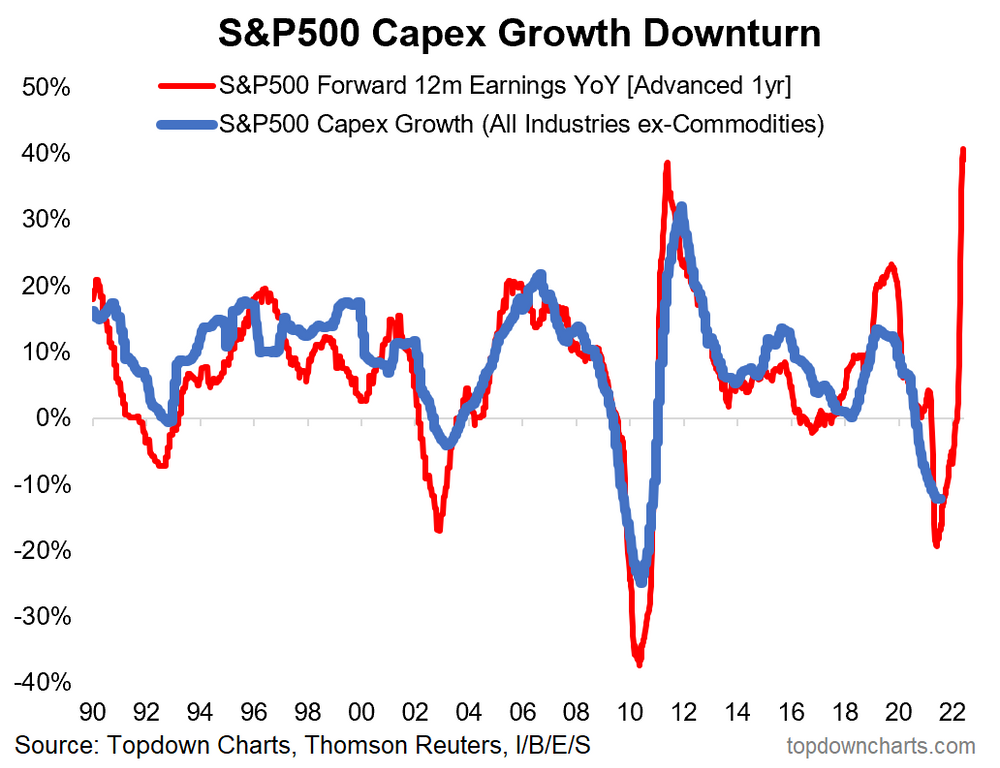

Corporate Capex and the Wage-Push Spiral

Beyond the macro numbers, business owners are facing a pragmatic crisis: the cost of talent. An unemployment rate of 4.3% indicates a tight labor market where workers still hold significant bargaining power. For mid-cap firms, this manifests as wage-push inflation. When companies are forced to raise wages to attract talent, they either absorb the cost—shrinking their EBITDA margins—or pass the cost to the consumer, further fueling the inflation the Fed is trying to kill.

This is where the strategy shifts. We are seeing a marked increase in capital expenditure (CAPEX) toward automation and AI integration. The goal is no longer just “efficiency”; it is “labor substitution.” If the cost of a human employee continues to rise due to a tight labor market, the ROI on automation software becomes exponentially more attractive.

For deeper insights into how this affects corporate filings, analysts should monitor SEC EDGAR filings for mentions of “labor costs” and “wage inflation” in the 10-Q reports of S&P 500 companies. The trend is clear: the era of cheap, abundant labor is over, and the era of expensive, scarce labor is being solved by software.

The Trajectory: What to Watch Moving Forward

As we move deeper into Q2 2026, the focus shifts from the headline payroll number to the “quality” of the jobs created. Are these full-time positions in high-productivity sectors, or are they part-time roles in the service economy? The former suggests sustainable growth; the latter suggests a fragile recovery.

Investors should keep a close eye on the Reuters economic calendar for the upcoming CPI print. If strong employment is followed by a spike in inflation, the Fed may be forced to consider a “hawkish hold” or even a surprise rate hike to prevent a wage-price spiral.

The pragmatic play here is simple: reduce exposure to highly leveraged firms that require immediate refinancing and increase positions in companies with strong pricing power. In a world where the labor market stays hot and the Fed stays hawkish, cash flow is king, and the ability to pass on costs is the only real hedge.

For a comprehensive view of the current yield curve, refer to the Wall Street Journal’s market data section, which tracks the real-time movement of the 2-year and 10-year spreads. The inversion may be shallowing, but the risk remains skewed to the upside.