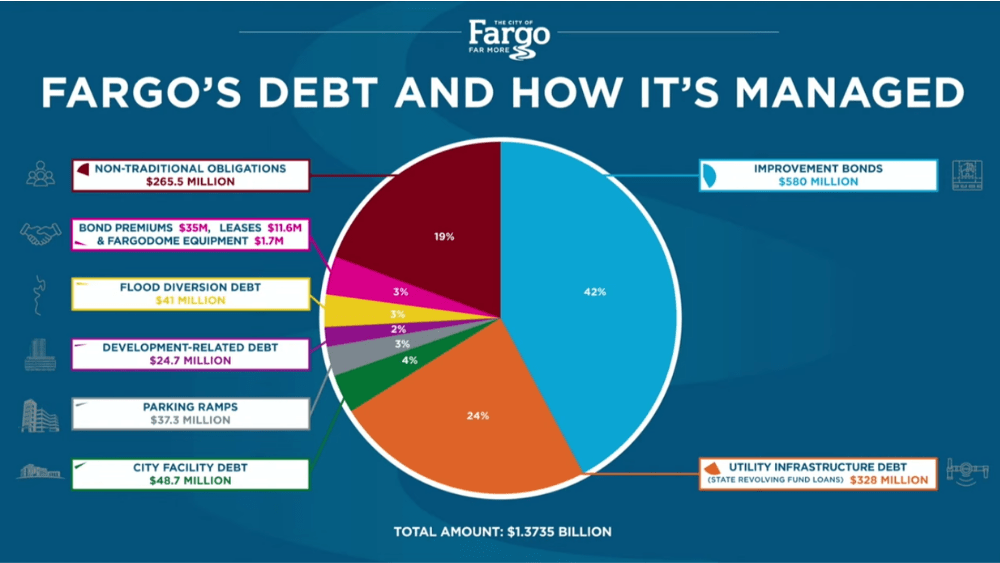

Fargo Mayor Dr. Tim Mahoney has detailed the city’s $1.37 billion debt load, specifying that $328 million is allocated to utility infrastructure via state revolving fund loans. This strategic debt supports critical wastewater plant expansions to sustain regional growth amid fluctuating municipal bond yields and rising infrastructure costs.

This disclosure is more than a local budgetary update; it is a microcosm of the current municipal leverage crisis facing mid-sized American hubs. As cities scale to meet population demands, they are forced to balance the immediate necessity of “grey infrastructure” with the long-term volatility of debt service. In an era where the Federal Reserve has maintained a restrictive stance to curb inflation, the cost of carrying this debt has shifted from a marginal expense to a primary fiscal driver.

The Bottom Line

- Debt Composition: Approximately 23.9% of Fargo’s total debt is tied specifically to utility infrastructure via State Revolving Fund (SRF) loans.

- Growth Hedge: The wastewater plant expansion is a prerequisite for commercial zoning increases, effectively betting on future tax revenue to offset current borrowing.

- Rate Mitigation: By utilizing SRF loans rather than open-market general obligation bonds, the city reduces its exposure to immediate market volatility.

The Mechanics of State Revolving Funds vs. Open Markets

To understand the $328 million carve-out, one must look at the instrument. State Revolving Funds (SRFs) are not standard municipal bonds; they are subsidized loan programs that provide below-market interest rates for water and wastewater projects. This represents a critical distinction for the city’s credit profile.

But the balance sheet tells a different story when you look at the remaining $1.04 billion. While the SRF loans are targeted and subsidized, the broader debt load is subject to the whims of the municipal bond market. When investors demand higher yields to compensate for inflation, the cost of refinancing existing debt rises.

Here is the math: if a city is forced to refinance even 10% of its non-subsidized debt at a rate 1.5% higher than the previous cycle, the annual debt service increase can strip millions from the operational budget. This is why the reliance on SRF loans is a calculated move to insulate the city from the volatility tracked by Bloomberg’s municipal bond indices.

The Macroeconomic Pressure on Municipal Solvency

Fargo’s debt situation does not exist in a vacuum. It mirrors a broader trend where cities are competing for corporate relocations by over-investing in infrastructure. This “infrastructure arms race” often involves heavy borrowing from entities like Moody’s Corporation (NYSE: MCO) rated bonds to fund growth.

The risk here is the “growth trap.” Cities borrow to build the capacity for new businesses, assuming those businesses will provide the tax base to pay off the debt. However, if macroeconomic headwinds—such as a slowdown in commercial real estate or a shift in remote work trends—stunt that growth, the city is left with “stranded assets” and a mounting debt service requirement.

“The primary risk for municipal issuers in the current cycle is not the absolute level of debt, but the debt-to-revenue growth ratio. When infrastructure costs outpace the organic growth of the tax base, credit downgrades become inevitable.”

This sentiment is echoed across the industry. As Reuters has reported on municipal trends, the cost of raw materials for wastewater plants—concrete, steel, and specialized piping—has remained stubbornly high, often exceeding original project estimates by 15% to 20%.

Infrastructure as a Commercial Catalyst

Despite the headline figure of $1.37 billion, the wastewater expansion is a strategic play. Without increased capacity, the city cannot issue new building permits for high-density commercial or industrial developments. This creates a dependency on firms like Aecom (NYSE: ACM) or Fluor (NYSE: FLR), who manage the execution of these massive civic projects.

The relationship is symbiotic: the city borrows to build, the contractors profit from the spend, and the resulting infrastructure allows for the entry of new corporate taxpayers. But this cycle depends entirely on the city’s ability to maintain its credit rating. A downgrade from S&P Global or Moody’s would immediately increase the cost of any future non-SRF borrowing.

| Debt Category | Estimated Allocation | Funding Source | Primary Strategic Purpose |

|---|---|---|---|

| Utility Infrastructure | $328 Million | SRF Loans | Wastewater & Water Expansion |

| General Obligation | $750 Million (Est.) | Municipal Bonds | Public Services & Administration |

| Other Liabilities | $292 Million (Est.) | Mixed/Revenue | Operational Capital & Pensions |

The Risk of Interest Rate Persistence

As we move through May 2026, the market is hyper-focused on whether the Federal Reserve will maintain rates at this plateau or begin a slow descent. For a city with over a billion dollars in liabilities, a 25-basis-point shift in the benchmark rate can have a ripple effect on the cost of future issuance.

If the city continues to lean on SRF loans, it effectively hedges against this risk. However, these funds are finite and often come with stringent federal regulations. The city cannot fund every project through a revolving fund; eventually, it must return to the open market.

Investors monitoring these trends often look at SEC filings of municipal-focused ETFs to see where the capital is flowing. Currently, there is a flight to quality, meaning cities with diversified revenue streams and a disciplined approach to “essential” debt—like wastewater—are faring better than those borrowing for aesthetic urban renewal.

The Forward Trajectory

Fargo’s current strategy is a pragmatic acceptance of leverage in exchange for scalability. By isolating the utility debt within the SRF framework, Mayor Mahoney is attempting to preserve the city’s general fund flexibility. The success of this gamble depends on the city’s ability to convert that $328 million in pipes and pumps into actual commercial square footage and payroll taxes.

For the business owner in Fargo, this means utility rates will likely remain a point of contention as the city services this debt. For the institutional investor, it is a signal that the city is aggressively positioning itself for growth, albeit with a significant liability overhang. The focus now shifts to the 2026-2027 fiscal audits to see if the revenue growth is keeping pace with the interest accrual.

the market will judge Fargo not by the size of its debt, but by the efficiency of its capital deployment. If the wastewater expansion unlocks a new wave of industrial investment, $1.37 billion is a manageable price for progress. If not, it is a weight that will constrain the city’s fiscal autonomy for a generation.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.