Imam Killed in Casablanca Mosquée: Police Probe Ongoing

A Moroccan imam was killed inside a mosque in Casablanca on June 28, 2026, during an attack that has triggered a nationwide manhunt and raised urgent questions about security in ... Read More

Saturday Edition

Stay updated with Archyde – your source for breaking news, global headlines, economy, entertainment, health, technology, and sports. Fresh stories daily.

A Moroccan imam was killed inside a mosque in Casablanca on June 28, 2026, during an attack that has triggered a nationwide manhunt and raised urgent questions about security in ... Read More

Continuous Coverage

The U.S. Supreme Court on Monday declined to hear an appeal from Donald Trump regarding a 2023 jury…

In Oizumi, a town in Japan’s Gunma Prefecture often referred to as “Little Brazil,” the FIFA World Cup…

Louisville, KY — Louisville Metro Police Department (LMPD) has confirmed the death of Fourth Division Officer Anthony Elliott,…

Malaysia Airlines’ fuel costs have surged to a staggering 50% of its operational expenses—double the pre-conflict rate—after U.S.-Iran…

Curiosis Initiates 100% Free Share Distribution to Boost Market Liquidity Curiosis (494120), a specialized developer in lab automation…

Legal professionals at the Orléans courthouse initiated a strike on June 29, 2026, protesting security concerns and systemic…

Global Affairs

Ireland’s exclusion from the International Criminal Court’s prosecutor’s office has sparked diplomatic unease in Brussels and Dublin, raising…

Markets And Money

Austria’s Flughafen Wien AG (FWAG.AT) is quietly reshaping Europe’s airport infrastructure with a €1.2 billion expansion plan unveiled…

Digital Culture

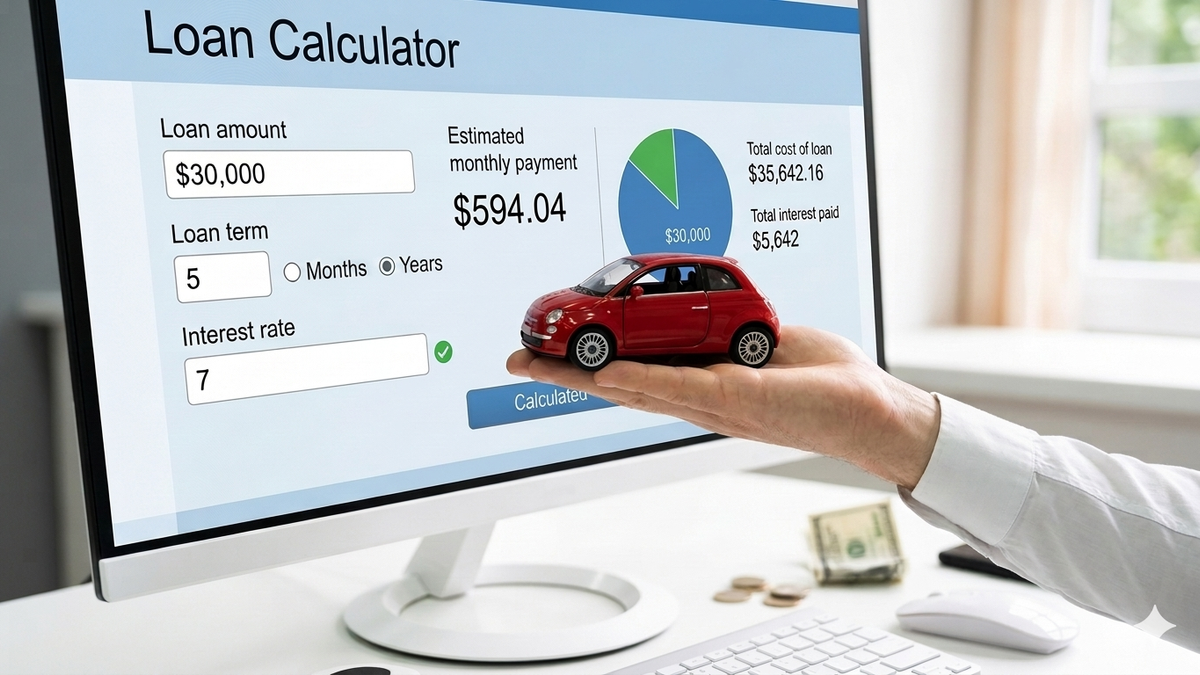

Americans locked into auto loans between 2022 and 2024 are paying an average of $80 more per month…

Science And Wellbeing

The Affordable Care Act (ACA) expanded health insurance coverage to 20 million previously uninsured Americans by 2023, yet…

Screen And Sound

A viral video from Gadget Glimpse featuring a motorized toy alien abducting a plastic cow has captured widespread…

Fixtures And Form

Zach Werenski’s potential trade has sparked urgency in Columbus, with top-tier defensive prospects and cap flexibility driving interest…