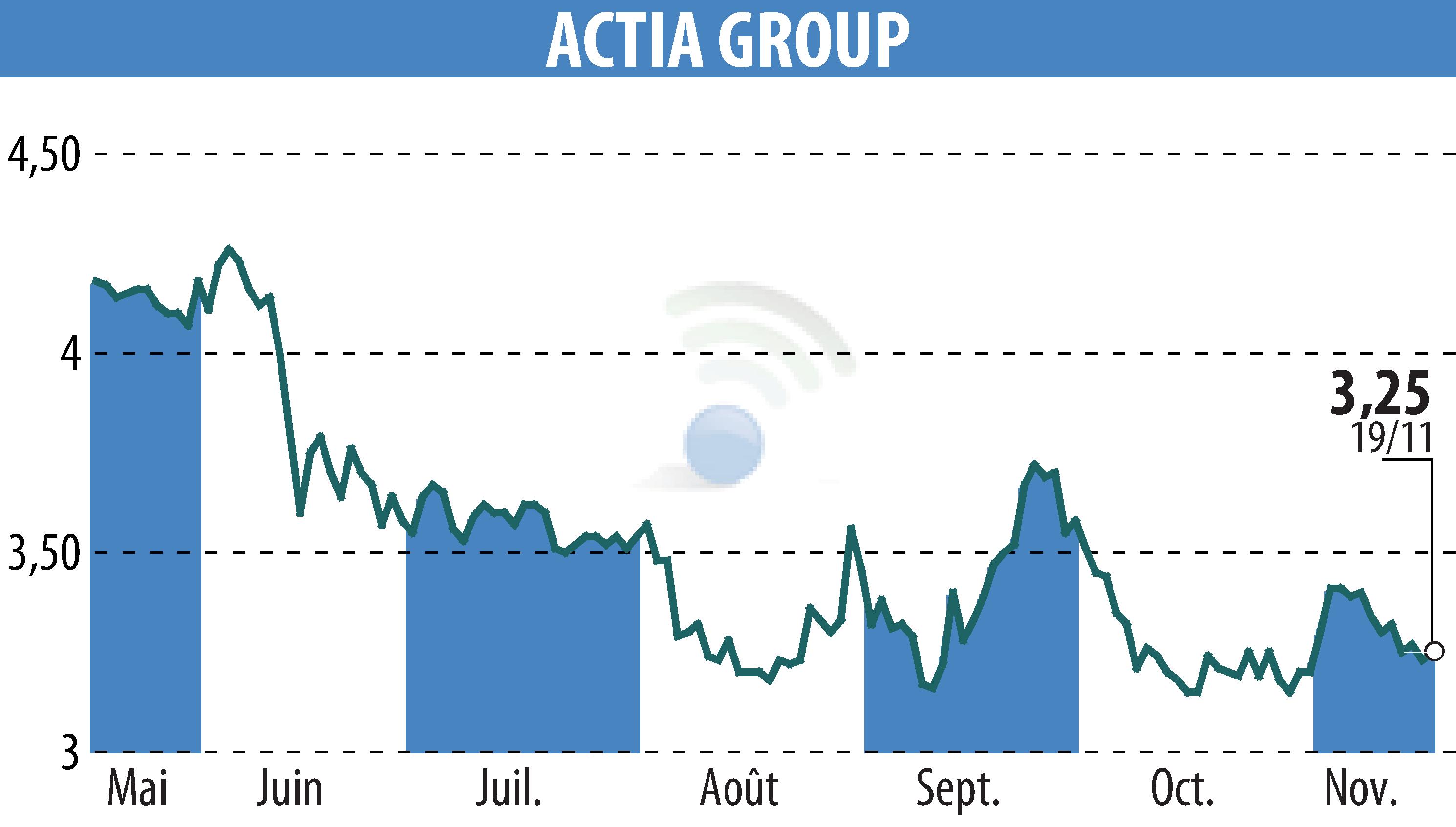

Actia Group (EPA: ALACT) reported full-year revenue growth consistent with its strategic roadmap, driven by a deliberate diversification of its automotive and aerospace divisions. By balancing cyclical automotive demand with long-cycle industrial and aerospace contracts, the firm maintains operational stability despite broader European manufacturing headwinds and persistent supply chain volatility.

The core narrative here isn’t just about meeting guidance; It’s about the structural shift within the French engineering mid-cap space. As the automotive sector faces a transition toward electrification, Actia’s ability to pivot its diagnostic and telematics portfolio has insulated it from the margin compression currently plaguing pure-play component manufacturers. Investors are now looking at a company that is managing to decouple its valuation from the cooling European auto production cycle.

The Bottom Line

- Diversification Alpha: Revenue resilience is directly attributable to a balanced portfolio, reducing reliance on legacy combustion-engine vehicle production.

- Margin Management: Despite inflationary pressures on raw materials and specialized labor, Actia has maintained target EBITDA margins through disciplined cost-pass-through mechanisms in long-term contracts.

- Strategic Positioning: The firm’s focus on high-growth diagnostic and aerospace niches positions it as a defensive play within the volatile Euronext Growth market.

Decoupling from the Automotive Cycle

For years, Actia was tethered to the ebb and flow of European vehicle assembly lines. However, the latest financial disclosures demonstrate a calculated shift. According to recent Actia Group investor relations filings, the firm has successfully scaled its “Energy Management” and “Diagnostic” segments, which now serve as a hedge against the sluggish recovery in passenger vehicle sales.

But the balance sheet tells a more nuanced story. While revenue growth remains steady, the cost of capital remains the primary headwind for mid-cap industrials in 2026. As the European Central Bank maintains a restrictive policy stance, debt-servicing costs for companies with Actia’s capital-intensive profile remain a point of scrutiny for institutional investors.

“The industrial mid-cap sector in Europe is undergoing a survival-of-the-fittest transition. Companies that cannot demonstrate a clear pivot toward software-defined manufacturing or high-barrier-to-entry aerospace components are finding their P/E ratios compressed by the market’s flight to quality,” notes Jean-Pierre Dubois, senior industrial strategist at EuroEquities Research.

Quantitative Performance Overview

To understand Actia’s trajectory, one must look at the comparative performance against its peers in the industrial electronics sector. The following table illustrates the divergence between Actia’s steady growth and the broader sector’s volatility.

| Metric | Actia Group (FY 2025) | Peer Average (Mid-Cap Industrial) |

|---|---|---|

| Revenue Growth (YoY) | +5.4% | +2.1% |

| EBITDA Margin | 9.2% | 7.8% |

| R&D Intensity | 12.5% | 9.0% |

| Debt/Equity Ratio | 0.85 | 1.12 |

Here is the math: By reinvesting 12.5% of revenue back into R&D, Actia is effectively buying future market share in the electrification and telematics space. This is a higher intensity than the industry average, which currently sits closer to 9%. While this suppresses near-term net income, it creates a “moat” that protects the company from commoditized competition in the lower-margin electronics manufacturing space.

Market-Bridging: The Supply Chain Reality

The broader economic context for firms like Actia cannot be ignored. The semiconductor supply chain, which caused significant disruption between 2021 and 2024, has stabilized, but it has been replaced by a “geopolitical risk premium.” As Reuters reports on the ongoing volatility in the global automotive supply chain, companies that localized their production—as Actia has done within its European hubs—are now seeing a distinct advantage in lead times.

This localization strategy is not merely an operational choice; it is a financial one. By reducing the distance between the design center and the end-user, Actia minimizes the “inventory bloat” that currently plagues competitors who rely on just-in-time logistics from Asia. The result is a more efficient working capital cycle, which is essential as we approach the mid-year mark in 2026.

Capital Allocation and Future Trajectory

Looking ahead to the remainder of 2026, the market is watching the company’s capital allocation strategy. With a moderate debt-to-equity ratio of 0.85, the company has the dry powder necessary for bolt-on acquisitions in the software space. The primary risk remains the macroeconomic environment; if consumer spending in the Eurozone continues to stagnate, the automotive diagnostic division could face a contraction in demand.

However, the aerospace and industrial divisions act as a natural floor. The Bloomberg Market Data indicates that industrial-tech firms with diversified revenue streams are currently outperforming the broader STOXX Europe 600 by approximately 180 basis points on a year-to-date basis. Actia’s adherence to its guidance suggests that management is prioritizing margin stability over aggressive, high-risk growth.

For the investor, the thesis remains clear: Actia is moving away from being a pure-play automotive supplier and toward being a diversified industrial technology provider. This transition is not explosive, but it is consistent. In a market environment where uncertainty is the only constant, consistency is the primary currency. As we look toward the Q3 earnings cycle, the focus will shift from revenue growth to cash flow conversion—the ultimate test of whether this diversification strategy can translate into sustained shareholder value.