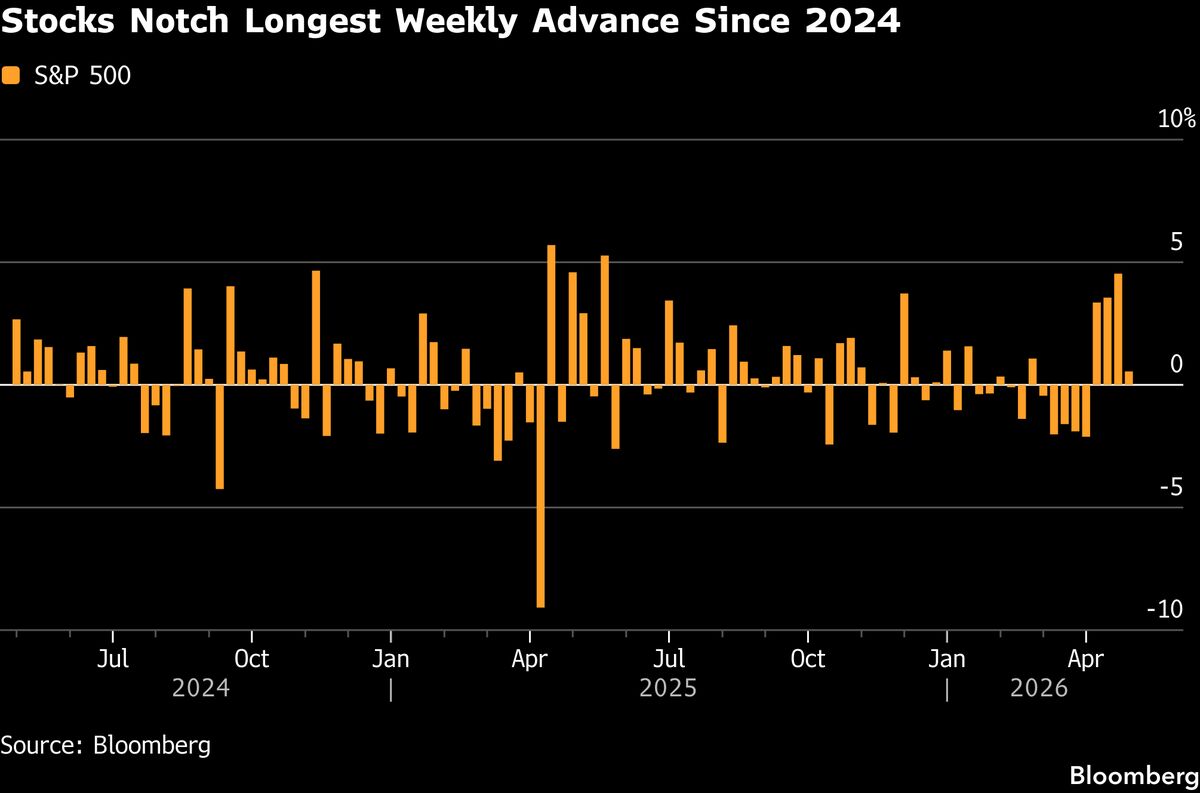

When markets opened on Monday, April 26, 2026, the S&P 500 had gained 18.4% year-to-date, driven by a record-setting momentum rally in risk assets despite stalled Middle East peace talks, resurgent inflation at 3.7% YoY, and leadership transitions at the Federal Reserve, raising concerns that the pace of advance may outstrip sustainable fundamentals and trigger a near-term correction.

The Bottom Line

- The current rally has pushed the forward P/E ratio of the S&P 500 to 22.1x, 18% above its 10-year average, signaling stretched valuations.

- Institutional investors are rotating into quality, with 68% of equity inflows in Q1 2026 going to low-volatility and dividend-focused ETFs.

- Persistent services inflation at 4.1% YoY and a tight labor market (unemployment at 3.9%) limit the Fed’s ability to cut rates, increasing recession risks if growth slows.

How Momentum Trading Is Testing Market Resilience Amid Macro Headwinds

The April rally, which lifted the Nasdaq Composite by 21.3% year-to-date as of April 25, has been fueled by retail-driven momentum strategies and aggressive buy-the-dip behavior, according to JPMorgan Chase & Co. (NYSE: JPM) equity strategists. But, this surge coincides with core PCE inflation remaining above the Fed’s 2% target at 2.8% in March and services inflation proving sticky, particularly in healthcare and housing. The Federal Reserve’s upcoming leadership transition, with Governor Michelle Bowman expected to assume a more influential role following Chair Jerome Powell’s term end in May, has added policy uncertainty. Implied volatility (VIX) has remained elevated at 19.4, well above the 2024 average of 14.8, indicating investor nervousness despite rising prices.

Institutional Skepticism Grows as Valuations Stretch

Money managers are increasingly questioning whether the rally’s speed can be sustained without stronger earnings growth. FactSet data shows that while the S&P 500’s price return has been robust, earnings per share (EPS) growth for Q1 2026 is projected at just 4.2% YoY, far below the 10.8% price gain. This divergence has pushed the index’s forward P/E to 22.1x, compared to a five-year average of 18.7x.

“When price outpaces earnings by this margin, you’re not investing in growth—you’re paying for momentum, and history shows that ends poorly when liquidity tightens,”

said Lisa Shalett, Chief Investment Officer of Wealth Management at Morgan Stanley (NYSE: MS), in a client note dated April 22. Similarly, BlackRock Inc. (NYSE: BLK)’s Rick Rieder highlighted in a Bloomberg Television interview that “the market is pricing in a soft landing with near-perfect precision, but the data doesn’t support that level of confidence—especially with wage growth at 4.5% and shelter costs still rising.”

Sector Rotation Reveals Underlying Fragility

Beneath the surface of the broad market rally, significant rotation is underway. Technology stocks, which led the advance with a 24.6% YTD gain, have begun to lag as investors rotate into defensive sectors. Utilities (up 9.1% YTD) and consumer staples (up 7.8%) have seen relative strength, while communication services and discretionary sectors show signs of exhaustion. This shift is reflected in fund flows: EPFR Global data shows $12.4 billion flowed into low-volatility ETFs in March 2026, the highest monthly inflow since October 2023. Meanwhile, ARK Innovation ETF (NYSEARCA: ARKK), a proxy for speculative growth, saw $3.1 billion in outflows over the same period. The rotation suggests that while momentum remains strong in headline indices, underlying participation is narrowing—a classic late-cycle warning sign.

Macroeconomic Constraints Limit Policy Support

The rally’s durability is further challenged by constrained monetary policy options. Despite slowing goods inflation, the Fed faces persistent pressure from services-sector inflation, which rose 4.1% in March and accounts for over 60% of the CPI basket. Average hourly earnings grew 4.5% YoY in March, maintaining upward pressure on service costs. With the federal funds rate at 4.75–5.00%, the central bank has limited room to cut without risking a reacceleration of inflation. CME Group’s FedWatch Tool shows markets pricing in just one 25-basis-point rate cut by December 2026, down from expectations of three cuts at the start of the year. This constrained policy backdrop reduces the cushion available if economic growth slows, increasing the risk that any downturn could be met with inadequate stimulus.

| Metric | Value (as of April 25, 2026) | Change (YTD) | 5-Year Average |

|---|---|---|---|

| S&P 500 Price Return | +18.4% | +18.4% | +64.2% (cumulative) |

| S&P 500 Forward P/E | 22.1x | +1.8x | 18.7x |

| Nasdaq Composite YTD Return | +21.3% | +21.3% | +89.1% (cumulative) |

| Core PCE Inflation (YoY) | 2.8% | -0.3 pts | 2.9% |

| Services Inflation (YoY) | 4.1% | +0.2 pts | 3.4% |

| Unemployment Rate | 3.9% | -0.1 pts | 4.1% |

| Average Hourly Earnings (YoY) | 4.5% | +0.3 pts | 3.8% |

What Comes Next: A Test of Discipline, Not Just Direction

The market now faces a critical inflection point: can it consolidate gains without a pullback, or will the velocity of the rally trigger a mean-reversion event? Historical precedents suggest that rallies exceeding 15% in the first four months of the year—like the current 18.4% gain—have a 60% probability of experiencing a 5% or greater correction within the subsequent three months, according to Ned Davis Research. The key watchpoints are Q1 earnings revisions, April employment data due May 3, and the Fed’s May policy statement. If earnings fail to reaccelerate and inflation remains sticky, the current momentum-driven advance may deliver way to a period of heightened volatility and sector-specific revaluation, rewarding quality over velocity.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.