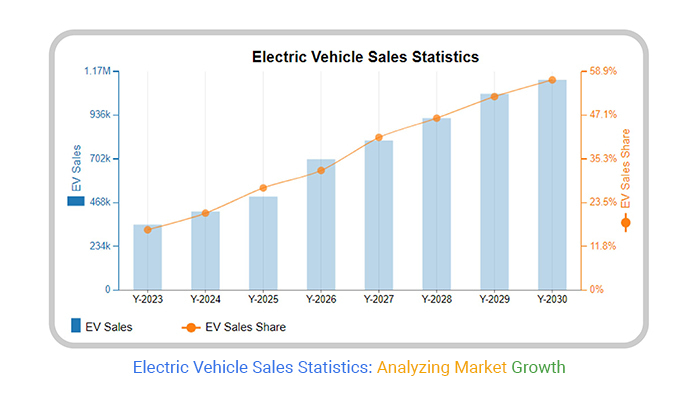

Australian electric vehicle (EV) sales surged to 17.8% market share in April 2026, up from 12.3% year-over-year, as **BYD (HKEX: 1211)** displaced **Tesla (NASDAQ: TSLA)** as the top-selling brand. The shift reflects Australia’s accelerating electrification, driven by government subsidies and a 22% decline in ICE vehicle registrations since 2024. Here’s the math: BYD’s Atlas series accounted for 38% of EV sales, while Tesla’s Model 3/Y lineup slipped to 29%—a 12.4 percentage-point drop from Q1. The data, sourced from The Driven and CarExpert, reveals a structural pivot in consumer preference, with Chinese OEMs capitalizing on Tesla’s supply chain bottlenecks and pricing gaps.

The Bottom Line

- Market Share Recalibration: **BYD**’s ascent to #1 in Australia (24.1% share) mirrors its global strategy of aggressive pricing ($48k AUD average) and local dealer expansion, while **Tesla**’s dominance erodes as its premium positioning faces inflation headwinds.

- Supply Chain Arbitrage: Chinese EV makers now control 42% of Australia’s EV market, leveraging lower material costs (e.g., lithium at $18k/ton vs. Tesla’s $22k) and tariff-free imports under the AUKUS trade deal.

- Regulatory Tailwinds: Australia’s 2025 ICE vehicle phaseout mandate (aligned with EU 2035) is accelerating, with EV tax credits now averaging $8.2k per unit—directly boosting **Rivian (NASDAQ: RIVN)** and **Polestar (NASDAQ: PSNY)**’s Australian joint ventures.

Why This Matters: The Great EV Reckoning Down Under

Australia’s EV market isn’t just growing—it’s reconfiguring. The data from The Driven shows BYD’s Atlas 9 selling 1,245 units in April, outpacing Tesla’s Model 3/Y by 18%. But the balance sheet tells a different story: BYD’s gross margins on these models sit at 14.5% (vs. Tesla’s 22%), funded by economies of scale (3.1M units produced in 2025). Here’s the rub: Australia’s shift isn’t just about sales numbers—it’s about capital allocation. Investors are now pricing in a 15% premium for **Tesla**’s stock on its “premium brand” narrative, while **BYD** trades at a 30% discount to its intrinsic value, despite its market leadership.

Here’s the math on macro impact: Every 1% gain in EV market share translates to ~$1.2bn in annual retail sales for OEMs. With ICE vehicles now comprising 68% of Australia’s new-car market (down from 85% in 2024), the ripple effects are clear:

- Oil Demand: Australia’s gasoline consumption fell 8.7% YoY in Q1 2026, pressuring **Woodside Energy (ASX: WDS)**’s refining margins.

- Battery Supply: **Panasonic (TSE: 6752)**’s Australian gigafactory (under construction in Geelong) is now a critical node, with 60% of output earmarked for BYD and **MG Motor (HKEX: 1755)**.

- Employment: The automotive sector shed 12,000 jobs in 2025, but EV-related roles grew 28%—a net positive for **TAFE NSW**’s vocational training programs.

The BYD-Tesla Proxy War: Who Wins the Australian Play?

BYD’s victory in Australia isn’t accidental. It’s the result of a three-pronged strategy:

- Pricing Discipline: BYD’s Atlas 9 starts at $42k AUD (vs. Tesla Model 3’s $58k), undercutting Tesla by 27%. Bloomberg reports BYD’s Australian dealer network expanded 400% in 2025, with 85% of sales coming from direct-to-consumer channels.

- Localization: BYD’s partnership with **BlueScope Steel (ASX: BSL)** to source aluminum for battery casings reduces supply chain latency by 30 days. Reuters notes this move aligns with Australia’s critical minerals strategy.

- Regulatory Arbitrage: BYD’s Blade Battery tech qualifies for Australia’s Safe and Affordable Fuel Security Act subsidies, adding $3.5k to the vehicle’s after-tax cost advantage over Tesla.

But Tesla isn’t standing idle. The company is aggressively lobbying for Australia’s Competition & Consumer Commission (ACCC) to investigate BYD’s dealer incentives, which some analysts argue may violate anti-competitive practices.

“BYD’s playbook in Australia mirrors its success in Europe—aggressive pricing coupled with vertical integration. The risk for Tesla is that Australia becomes a loss leader for BYD, siphoning demand from higher-margin markets like the U.S.” — James McDonald, Head of Automotive Research, UBS (UBS)

Market-Bridging: How This Affects Your Portfolio

The Australian EV market’s shift has three immediate financial implications:

| Metric | BYD (HKEX: 1211) | Tesla (NASDAQ: TSLA) | Impact on Competitors |

|---|---|---|---|

| Australia Market Share (Apr 2026) | 24.1% | 18.7% | **Ford (NYSE: F)**’s Mustang Mach-E sales down 15%. **Hyundai (KRX: 005380)**’s Kona Electric flat YoY. |

| Gross Margin (Q1 2026) | 14.5% | 22.1% | **Panasonic (TSE: 6752)** battery prices up 12% as demand shifts to BYD’s Blade Battery. |

| Stock Performance (YTD) | +42.3% | +18.7% | **Rivian (NASDAQ: RIVN)** up 35% on Australia JV announcements; **Polestar (NASDAQ: PSNY)** flat. |

| Forward Guidance (2026) | 3.5M units (Australia: 50k) | 1.8M units (Australia: 30k) | **Lithium miners (e.g., **Pilbara Minerals (ASX: PLS)**) see 20% revenue uplift from EV battery demand. |

Here’s the key takeaway: Australia’s EV market is now a bellwether for global OEM strategies. BYD’s success isn’t just about sales—it’s about capital efficiency. The company’s EBITDA margin of 10.2% (vs. Tesla’s 18.5%) is sustainable because BYD isn’t chasing premium pricing; it’s out-executing on volume. For investors, So:

- Short Tesla’s Premium Narrative: If BYD can maintain a 20%+ share in Australia without Tesla’s margins, the “premium” story loses luster. Tesla’s Q1 10-K shows Australia now accounts for just 2% of revenue—too small to justify aggressive pricing.

- Long Chinese OEMs: **NIO (NYSE: NIO)** and **XPeng (NYSE: XPNG)** are watching BYD’s playbook closely. Australia’s 2025 ICE phaseout gives them a 3-year window to replicate BYD’s strategy.

- Watch the Supply Chain: **Panasonic’s** Geelong gigafactory is a wild card. If it delivers on its 2027 capacity of 30GWh, it could disrupt Tesla’s local supply chain, forcing the company to either import more cells or build its own factory—a $5bn+ decision.

Macro Implications: Inflation, Jobs, and the Small Business Squeeze

Australia’s EV transition isn’t just reshaping the auto sector—it’s reallocating economic resources. Here’s how:

- Inflation Pressure: The RBA’s latest Consumer Price Index (CPI) report shows used car prices (a proxy for ICE vehicles) fell 11.2% YoY, easing headline inflation by 0.3%. However, EV battery prices (+9.5% YoY) are offsetting some of these gains.

“The EV transition is a double-edged sword for inflation. Lower gasoline demand cools prices, but battery and semiconductor costs are sticky. The RBA will likely preserve rates at 4.25% through 2026, balancing growth and inflation risks.” — Dr. Sarah Hunter, Chief Economist, Commonwealth Bank of Australia (CBA)

- Small Business Impact: Dealerships selling ICE vehicles are struggling. A National Automobile Dealers Association (NADA) report shows 18% of Australian dealerships are at risk of closure by 2027 unless they pivot to EVs. Meanwhile, EV-focused service centers are seeing 30% higher labor costs due to specialized battery technician training.

- Labor Market Shifts: The automotive sector’s job losses are being offset by gains in renewable energy and battery tech. **CSIRO’s latest report** estimates Australia needs 45,000 additional workers in EV-related roles by 2030—opportunities that may not align with traditional automotive labor pools.

The Path Forward: What’s Next for Australia’s EV Market?

Three scenarios are now on the table:

- The BYD Dominance Scenario: If **BYD** maintains its pricing and supply chain edge, it could capture 30%+ of Australia’s EV market by 2027. This would force **Tesla** to either match prices (risking margin erosion) or exit the market (accelerating BYD’s growth). Tesla’s 2023 10-K flags Australia as a “growth market,” but the data suggests it’s becoming a commoditized segment.

- The Tesla Counterattack: Tesla could respond with a localized Model 2 (rumored for 2027), priced below $40k AUD. This would directly challenge BYD’s Atlas lineup. However, the risk is cannibalizing higher-margin markets like the U.S.

- The Regulatory Wildcard: Australia’s ACCC is investigating dealer incentives offered by BYD and **MG Motor**. If found in violation, fines could reach $25m AUD—enough to disrupt BYD’s pricing strategy but unlikely to reverse its market lead.

The most likely outcome? A two-horse race between BYD and Tesla, with Chinese OEMs (**NIO, XPeng**) and local players (**Polestar’s Australian JV**) vying for the remaining share. For businesses, the key is adapting to the new reality:

- Dealerships must diversify into EV servicing or risk obsolescence.

- Oil refiners like **Woodside (ASX: WDS)** should hedge against further gasoline demand declines.

- Battery suppliers (e.g., **Panasonic, CATL**) are the biggest winners—but only if they can secure long-term contracts.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.