The Bank of England will only raise interest rates if a severe supply shortage emerges, Governor Andrew Bailey stated, signaling a cautious approach to monetary tightening despite persistent inflationary pressures as markets open on Monday. This stance reflects growing concern that premature rate hikes could stifle economic recovery amid fragile supply chains and uneven wage growth, with the BoE prioritizing demand-side stability over preemptive inflation control.

The Bottom Line

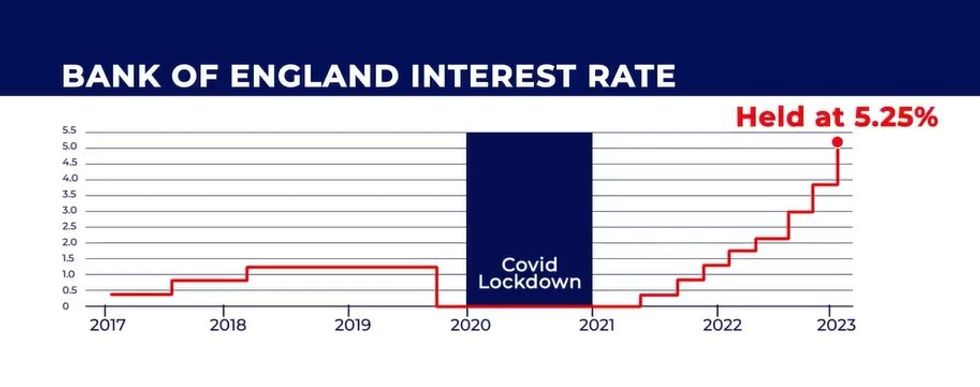

- The BoE’s conditional rate-hike framework implies interest rates will likely remain at 5.25% through Q3 2026 unless supply-chain disruptions intensify.

- UK gilt yields have already priced in only one 25-basis-point hike by year-end, down from four expected in January, per ICE Benchmark Administration data.

- Consumer-facing sectors like retail and hospitality may benefit from prolonged low rates, while exporters face continued pound sterling volatility.

How the BoE’s Supply-Dependent Rate Policy Reshapes UK Inflation Expectations

The Bank of England’s shift to a supply-triggered rate-hike model marks a departure from its traditional forward-looking inflation targeting. By tying monetary policy to observable supply shortages rather than wage growth or services inflation, the BoE is effectively outsourcing inflation control to global commodity markets and logistics networks. This approach carries significant risk: if supply constraints emerge suddenly—such as a North Sea oil platform outage or a semiconductor import delay—the BoE may be forced into aggressive, reactive tightening that could trigger a sharper-than-expected downturn. Conversely, if supply chains remain resilient, the UK could endure persistently above-target inflation without policy relief, eroding real wages and consumer confidence. As of April 2026, UK CPI inflation stands at 3.8%, down from 6.7% in early 2024 but still above the 2% target, with services inflation at 5.1% driving the persistence, according to the Office for National Statistics.

Market Reaction: Gilt Yields, Sterling, and Sector Divergence

Following Bailey’s remarks, two-year gilt yields fell 12 basis points to 4.35%, while ten-year yields slipped to 4.10%, reflecting diminished near-term rate-hike expectations, per London Stock Exchange Group data. The pound sterling weakened 0.8% against the dollar to $1.27, as investors priced in a longer period of monetary divergence from the Federal Reserve, which maintains a 5.25–5.50% range. Notably, FTSE 100 exporters such as **Diageo (LSE: DGE)** and **Unilever (LSE: ULVR)** gained 1.2% and 0.9% respectively, benefiting from a weaker pound boosting overseas earnings when converted to sterling. In contrast, domestically focused banks like **Lloyds Banking Group (LSE: LLOY)** fell 0.7%, as prolonged low rates compress net interest margins. Lloyds’ Q1 2026 net interest margin declined to 2.9% from 3.1% in Q4 2025, per its trading update, underscoring the pressure on UK lenders.

Supply Chain Fragility: The Hidden Trigger for BoE Action

The BoE’s conditional framework hinges on monitoring specific supply-side indicators, including the UK Manufacturing PMI’s delivery times sub-index, global freight rates via the Drewry World Container Index, and energy import volumes. As of March 2026, the UK Manufacturing PMI delivery times stood at 48.2 (below 50 indicating lengthening delays), while the Drewry index showed a 22% YoY increase in container freight rates from Asia to Europe, driven by Red Sea rerouting and port congestion in Singapore. Energy supply remains a critical vulnerability: UK natural gas storage levels are at 58% of capacity, below the five-year average of 72% for this time of year, per Gas Infrastructure Europe data. A cold snap or LNG import disruption could rapidly tighten supply, forcing the BoE’s hand. “The BoE is essentially outsourcing its inflation fight to global logistics,” said

David Miles, former BoE MPC member and Professor of Financial Economics at Imperial College London.

“If a Suez Canal-style shock hits, they’ll have to hike fast—and markets aren’t priced for that volatility.”

Corporate Earnings and Forward Guidance: Building Resilience Amid Uncertainty

UK corporations are adjusting to the BoE’s wait-and-see stance by reinforcing balance sheets and diversifying supply chains. **Tesco (LSE: TSCO)** reported Q1 2026 revenue growth of 3.1% YoY, with gross margins stable at 5.8%, citing effective hedging against commodity volatility and longer-term supplier contracts. The retailer has increased its UK-sourced produce share to 42% from 35% in 2023, reducing exposure to global shipping delays. Similarly, **GSK (LSE: GSK)** raised its 2026 full-year earnings guidance to £6.8–7.0 billion, up from £6.5–6.7 billion, citing strong demand for its HIV and oncology portfolios and effective pricing power despite modest currency headwinds. GSK’s CFO noted in its earnings call that “we are building inventory buffers in key markets to mitigate supply-chain shocks, which aligns with the BoE’s focus on actual disruption rather than forecasts.”

The Broader Economic Implication: Stagflation Risks and Policy Asymmetry

The BoE’s supply-dependent rate strategy introduces a dangerous asymmetry: it is leisurely to tighten when inflation rises from demand but may be forced to hike abruptly if supply shocks hit. This creates a policy lag that could worsen stagflation risks—where inflation remains elevated while growth stagnates. UK Q1 2026 GDP growth was revised down to 0.1% QoQ from 0.3%, with business investment falling 1.4%, per the ONS. Meanwhile, unemployment remains low at 4.0%, but wage growth at 5.2% continues to outpace productivity, fueling services inflation. “The BoE is betting that supply chains will hold,” said

Katrina Ell, Senior Economist at Oxford Economics.

“But if they don’t, the UK could face a 1970s-style policy dilemma—too late to act, then too aggressive when it does.”

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*