Public Bitcoin miners are pivoting to AI data centers to hedge against declining mining profitability, energy constraints, and quantum computing risks. This strategic migration leverages existing power infrastructure to capture high-margin AI compute demand, fundamentally altering the valuation models for firms like Core Scientific (NASDAQ: CORZ) and Hut 8 (NASDAQ: HUT).

The industry is currently facing a structural crisis. For years, the narrative focused on the “digital gold” rush, but by the close of Q1 2026, the math has shifted. The convergence of the 2024 halving’s delayed impact, the exponential rise in network hashrate, and the looming theoretical threat of quantum decryption has created a “triple pressure” environment. Pure-play mining is no longer a sustainable growth strategy; it is a legacy operation.

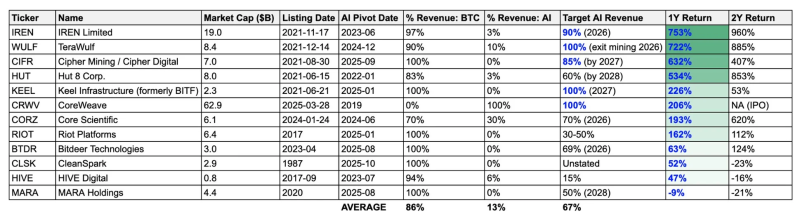

The Bottom Line

- Asset Reclassification: Markets are re-rating miners from “crypto-speculative” assets to “AI-infrastructure” plays, leading to expanded P/E multiples.

- Energy Arbitrage: The primary value proposition has shifted from the coins mined to the secured power capacity and grid interconnects.

- CAPEX Intensity: The transition from ASIC miners to NVIDIA GPU clusters requires massive capital expenditure, favoring firms with institutional backing over retail-funded operations.

The Arithmetic of the Hashrate Collapse

To understand the pivot, we must gaze at the margins. Bitcoin mining profitability is a function of the block reward versus the cost of electricity and hardware depreciation. As the network hashrate grew by approximately 28% over the last 18 months, the difficulty adjustment has squeezed smaller operators out of the market.

But the balance sheet tells a different story. While mining rewards have declined in real terms, the demand for High-Performance Computing (HPC) for Large Language Models (LLMs) has created a supply-demand imbalance in data center space. Here is the math: a megawatt of power used for Bitcoin mining generates a volatile, commodity-linked return. That same megawatt repurposed for AI compute can command a stable, long-term contract with a 3x to 5x higher revenue per kilowatt-hour.

This shift is not merely opportunistic; it is defensive. The specter of quantum computing, while still theoretical for the average investor, has forced institutional holders to diversify. The ability of quantum algorithms to potentially compromise Elliptic Curve Cryptography (ECC) has introduced a systemic risk premium that the market is now pricing in. By diversifying into AI, miners are effectively buying insurance against a “black swan” cryptographic failure.

Infrastructure Alchemy: Turning Power into Compute

The most critical asset in the AI race isn’t the chip—it’s the power. NVIDIA (NASDAQ: NVDA) can produce H100s and B200s, but they cannot build power substations. What we have is where the miners hold the leverage. Companies like Core Scientific (NASDAQ: CORZ) have spent a decade securing massive power allocations and building cooling infrastructure that can be adapted for AI workloads.

However, the transition is not a simple “plug-and-play” operation. ASIC miners are designed for a single task; AI clusters require complex networking, liquid cooling, and significantly higher power density per rack. This has led to a surge in partnerships between miners and hyperscalers. We are seeing a trend where miners provide the “shell” (power and land) while AI firms provide the “brains” (GPUs and software).

“The valuation of digital infrastructure is no longer tied to the volatility of a token, but to the reliability of the kilowatt. We are witnessing the industrialization of compute.”

This transition is impacting the broader supply chain. As miners pivot, the demand for specialized power transformers and industrial cooling systems has increased, contributing to lead times that now exceed 14 months for some critical components. You can track these infrastructure trends through Bloomberg’s industrial data or via Reuters’ energy reports.

Comparing the Unit Economics: Mining vs. AI Compute

The financial disparity between these two business models is stark. While mining is a race to the bottom on energy costs, AI compute is a race to the top on performance and reliability.

| Metric | Pure-Play BTC Mining | AI Data Center (HPC) | Variance |

|---|---|---|---|

| Revenue Stability | High Volatility (Market-Driven) | Stable (Long-term Contracts) | Significant Improvement |

| Typical Margin | 15% – 30% (Cycle Dependent) | 40% – 60% (Service Based) | +25% Avg |

| Asset Lifespan | 3-5 Years (Hardware Obsolescence) | 5-7 Years (Infrastructure) | +2 Years |

| Valuation Multiple | Low P/E (Speculative) | High P/E (Infrastructure) | 2x – 4x Expansion |

The Regulatory Tightrope and Market Consolidation

This pivot is not without risk. The U.S. Securities and Exchange Commission (SEC) has maintained a rigorous stance on how crypto-linked firms disclose their assets. As these companies transition, the transparency of their “AI revenue” will be under intense scrutiny. If a company claims AI capabilities but lacks the actual GPU count or power density to support it, People can expect a wave of “AI-washing” investigations similar to the dot-com era.

the consolidation of the power grid is creating a new set of antitrust hurdles. As a few large miners absorb the available power capacity in key regions (such as Texas and the Nordics), they are effectively creating a moat that prevents new AI startups from scaling. This brings them into direct competition with giants like Amazon (NASDAQ: AMZN) and Microsoft (NASDAQ: MSFT).

But the market is already pricing in this synergy. When looking at recent SEC filings, there is a clear trend of miners increasing their long-term debt to fund GPU acquisitions. They are betting that the cost of capital is lower than the projected growth of AI compute demand.

The Long-Term Trajectory: Beyond the Pivot

As we move further into 2026, the distinction between a “crypto miner” and a “cloud provider” will vanish. The winners will be those who successfully managed the CAPEX transition without over-leveraging their balance sheets during the 2024-2025 volatility window.

The “Triple Pressure” acted as a catalyst, forcing an evolution that was inevitable. The era of the “digital gold mine” has been replaced by the era of the “compute factory.” For investors, the play is no longer about predicting the price of Bitcoin, but about identifying who controls the power and the pipes of the AI economy.

Expect further M&A activity as hyperscalers look to acquire “power-rich” mining firms to bypass the bureaucratic delays of building new data centers from scratch. The power is the product; everything else is just software.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.