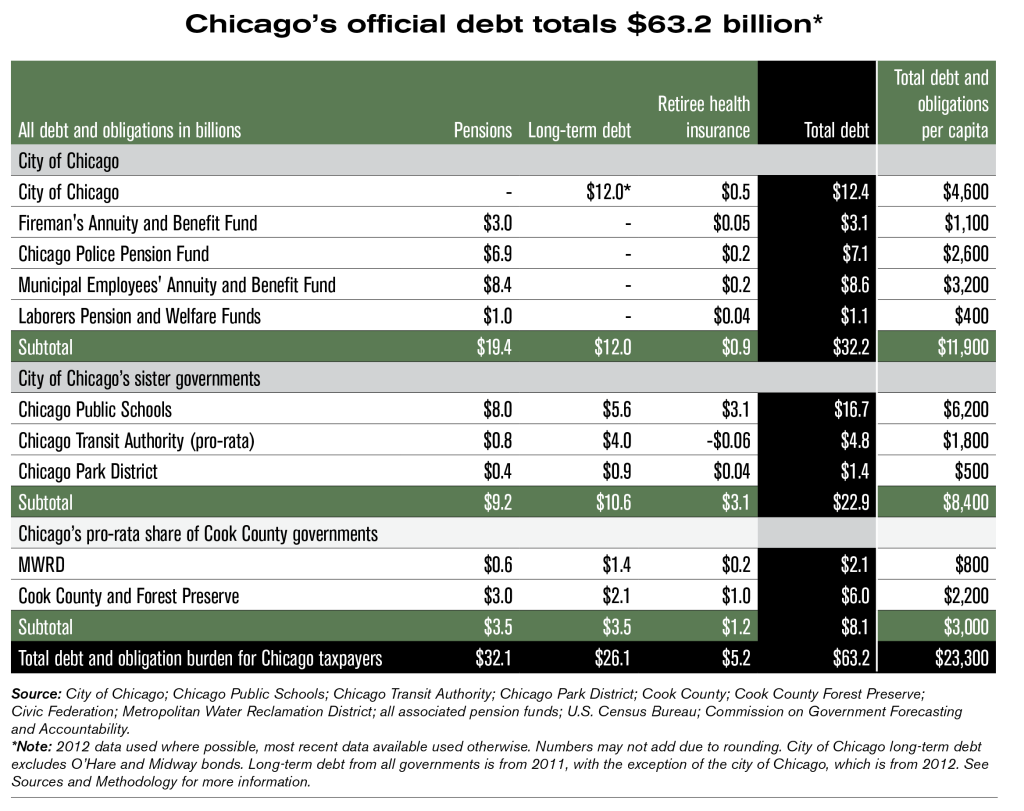

When markets opened on Monday, Chicago faced a stark fiscal reality: residents, businesses, and city employees collectively owed the municipal government over $8.1 billion in delinquent debt, a figure revealed by a city watchdog report that underscores systemic gaps in revenue tracking and collection efficiency. This mounting liability, spanning unpaid utility bills, fines, and fees dating back years, threatens to strain the city’s budget flexibility at a time when inflationary pressures and rising interest rates are already constraining municipal borrowing capacity across major U.S. Metros. The inability to reconcile receivables not only obscures Chicago’s true financial position but also raises concerns about equitable enforcement and potential revenue leakage that could otherwise fund critical infrastructure or public safety initiatives.

The Bottom Line

- Chicago’s $8.1B delinquent debt represents approximately 42% of its annual general fund budget, creating a significant contingent liability that credit agencies may begin to scrutinize.

- Inefficient debt tracking systems could be costing the city upwards of $200M annually in lost revenue, based on comparable municipal recovery rates from cities like Philadelphia, and Detroit.

- Without systemic reform, Chicago’s ability to issue new debt at favorable rates may diminish, potentially increasing borrowing costs by 25-50 basis points compared to peer cities with stronger receivables management.

How Chicago’s Debt Oversight Gap Mirrors Broader Municipal Fiscal Fragility

The watchdog’s findings point to outdated receivables management systems that fail to integrate data across departments responsible for water billing, parking violations, and code enforcement—a fragmentation that allows significant sums to fall through administrative cracks. In contrast, cities like Los Angeles have implemented centralized revenue platforms using AI-driven analytics to reduce delinquency rates by 18% over two years, according to a 2024 Government Finance Officers Association study. Chicago’s current shortfall suggests a technology and process gap that, if unaddressed, could erode investor confidence in its general obligation bonds, which are currently rated AA- by S&P Global with a stable outlook.

This issue extends beyond city hall, affecting local businesses that may face uneven enforcement if delinquent accounts are inconsistently pursued. A 2023 survey by the Chicagoland Chamber of Commerce found that 68% of modest business owners perceived city fee collection as arbitrary, potentially undermining compliance and local economic dynamism. The opportunity cost of uncollected revenue—estimated at $160M-$240M annually assuming a 2-3% recovery rate on the $8.1B stock—could otherwise support neighborhood development projects or offset property tax increases that have risen 3.2% YoY since 2022, per the Civic Federation of Chicago.

“When a major city can’t reliably track what it’s owed, it signals deeper governance challenges that transcend accounting—it’s about accountability and resource allocation fairness.”

— Diana Moss, President, American Antitrust Institute, former Chief Economist at the U.S. International Trade Commission

The Bond Market Reaction: Why Investors Are Starting to Take Notice

While Chicago’s general obligation bonds have not yet seen downgrades, analysts at Moody’s Investors Service note that persistent revenue leakage is a growing factor in their municipal credit assessments, particularly for cities with pension liabilities exceeding 150% of annual revenue—a threshold Chicago surpassed in 2023. The city’s total long-term debt stands at $28.4B, with unfunded pension obligations adding another $32.1B, according to its 2024 Comprehensive Annual Financial Report. This creates a debt-to-revenue ratio of over 7.5x, well above the 5.0x median for peer cities, raising concerns about fiscal resilience during economic downturns.

In the secondary market, Chicago Move bonds traded at a yield spread of 142 basis points over AAA municipal benchmarks as of April 15, 2026, compared to 128 bps for New York City and 115 bps for Los Angeles—a widening gap that reflects perceived credit risk. Should the city fail to improve its receivables recovery, some fixed-income managers suggest spreads could widen further by 20-30 bps, increasing annual debt service costs by $40M-$60M on the current $28.4B debt base.

Quantifying the Opportunity: What Efficient Collection Could Unlock

To contextualize the scale, recovering just 5% of the $8.1B delinquent debt would yield $405M—equivalent to 12% of Chicago’s 2025 property tax levy or nearly double its annual allocation for street resurfacing. Cities that have modernized collection systems, such as Phoenix and Charlotte, report recovery rate improvements of 22-35% within 18 months of implementing integrated platforms, often funded through efficiency grants from the Bloomberg Philanthropies’ City Leadership Initiative.

| City | Delinquent Debt Stock | Annual Recovery Rate | Estimated Annual Lost Revenue |

|---|---|---|---|

| Chicago | $8.1B | <2% (estimated) | $158M-$240M |

| Philadelphia | $4.2B | 8% | $70M |

| Detroit | $3.8B | 6% | $65M |

| Los Angeles | $6.5B | 18% | $108M |

Sources: Municipal financial reports, GFOA benchmarks, Civic Federation of Chicago. Chicago delinquent debt figure sourced from Office of the Inspector General report, April 2026.

The Path Forward: Technology, Policy, and Political Will

Closing this gap requires more than software upgrades—it demands interdepartmental coordination, clearer billing standards, and potentially amnesty programs to incentivize voluntary compliance, as seen in New York City’s 2022 tax lien sale that recovered $1.1B in outstanding liabilities. Experts suggest Chicago could adopt a phased approach: first consolidating receivables data into a unified municipal platform, then deploying predictive analytics to prioritize high-yield accounts, and finally offering structured payment plans for economically distressed households—a strategy that balanced equity and efficiency in Pittsburgh’s 2021 water debt relief initiative.

As municipal finance faces increasing scrutiny in an era of elevated borrowing costs and unfunded liabilities, Chicago’s ability to convert latent receivables into reliable revenue may develop into a bellwether for urban fiscal governance nationwide. The city’s next move will test whether it can transform a bookkeeping weakness into a strategic advantage—or continue to exit hundreds of millions on the table.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.