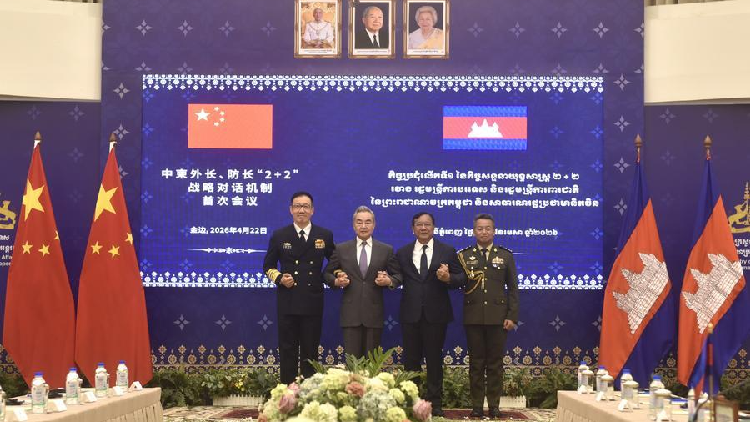

China and Cambodia reached a six-point consensus during their inaugural ‘2+2’ dialogue in Phnom Penh on April 22, 2026, covering defense cooperation, infrastructure investment, and regional security coordination, signaling a deepening strategic partnership as Beijing seeks to expand its influence in mainland Southeast Asia amid shifting U.S. Engagement patterns.

The meeting between Chinese State Councilor Wang Yi and Defense Minister Dong Jun with Cambodian Deputy Prime Minister Tea Banh and Foreign Minister Prak Sokhonn marks the first formal high-level security and foreign policy dialogue between the two nations since upgrading their relationship to a “community of shared future” in 2023. Although the consensus emphasizes non-interference and mutual respect, analysts note it reflects Cambodia’s ongoing pivot toward Beijing as Western aid conditionalities push Phnom Penh to diversify its strategic partnerships. This realignment has tangible implications for ASEAN cohesion, particularly as China advances its dual-use infrastructure projects along the Mekong Corridor, which underpins regional supply chains for electronics, textiles, and agricultural exports destined for European and North American markets.

Here is why that matters: Cambodia’s strategic location at the heart of Indochina makes it a linchpin for Beijing’s efforts to establish a secure southern flank for its Belt and Road Initiative, especially as tensions in the Taiwan Strait and South China Sea complicate maritime routes. The six-point agreement includes joint patrols in Cambodia’s exclusive economic zone, expanded training for Cambodian peacekeeping forces, and feasibility studies for a dual-use airport in Siem Reap—projects that could enhance China’s power projection capabilities while offering Phnom Penh much-needed modernization of its aging defense and logistics infrastructure.

But there is a catch: while Cambodia frames the partnership as sovereign choice, critics warn it risks entrenching dependency on Beijing at a time when the country’s public debt to China exceeds 40% of its GDP, according to the World Bank’s 2025 Debt Sustainability Analysis. This imbalance raises concerns about long-term autonomy, particularly if loan terms include opaque collateral arrangements similar to those seen in Sri Lanka’s Hambantota Port lease.

Historical Context: From Non-Alignment to Strategic Alignment

Cambodia’s foreign policy has long oscillated between neutrality and alignment, shaped by its traumatic 20th-century experience. After gaining independence from France in 1953, Prince Norodom Sihanouk pursued a policy of non-alignment, delicately balancing U.S., Chinese, and Vietnamese interests until the 1970 coup ushered in decades of conflict. Vietnam’s 1978 invasion and subsequent decade-long occupation left Cambodia deeply wary of Hanoi’s intentions—a sentiment China has skillfully exploited by positioning itself as a counterweight to Vietnamese influence.

Following the 1991 Paris Peace Accords, Cambodia gradually reopened to Western engagement, receiving substantial aid from the U.S., EU, and Japan. However, rising criticism over human rights and governance—particularly after the 2017 dissolution of the main opposition party—led to aid suspensions and sanctions. In response, Hun Sen’s government turned decisively toward China, which offered infrastructure financing without political conditions. By 2020, China had become Cambodia’s largest foreign direct investor, accounting for over 35% of approved FDI projects, according to the Council for the Development of Cambodia.

This trend accelerated under Hun Manet, who assumed the premiership in August 2023 after his father’s resignation. Though presenting a reformist facade, the younger Hun has maintained continuity in foreign policy, prioritizing economic pragmatism over ideological alignment. The ‘2+2’ dialogue institutionalizes this shift, creating a standing mechanism for strategic coordination that bypasses traditional ASEAN consensus protocols.

Global Supply Chain Implications: The Mekong Corridor as a Chokepoint

Cambodia’s role in global manufacturing has grown significantly over the past decade, particularly in textiles, footwear, and electronics assembly. The country exported $12.4 billion in goods to the United States and $8.1 billion to the EU in 2025, making it one of Southeast Asia’s fastest-growing export economies. Much of this output relies on the Mekong Corridor—a network of roads, railways, and river ports linking Phnom Penh to Ho Chi Minh City, Bangkok, and Kunming.

China’s investment in upgrading this corridor—including the Phnom Penh–Sihanoukville Expressway and the planned Lao-Cambodian-Vietnamese railway—aims to reduce transit times and logistics costs for southern China’s exports to Southeast Asia and beyond. For multinational firms operating in Vietnam and Thailand, improved Cambodian infrastructure offers an alternative route to bypass congestion at Laem Chabang and Hai Phong ports. However, it also increases exposure to single-point risks: should China leverage its infrastructure control for geopolitical leverage, disruptions could ripple through global apparel and electronics supply chains.

As one regional trade analyst noted, “Cambodia is becoming a critical node in China’s land-based maritime alternative strategy—what we call the ‘Maritime Silk Road’s inland twin.’ Any instability or coercion here affects not just ASEAN but global just-in-time manufacturing networks.”

“The real significance of this dialogue isn’t what’s on the paper—it’s the signal it sends to Washington and Brussels that Phnom Penh is now operating within Beijing’s strategic orbit, not just accepting its money.”

ASEAN Unity Tested: The Creeping Normalization of Asymmetrical Partnerships

The deepening Sino-Cambodian bond poses a quiet challenge to ASEAN’s centrality principle, which relies on consensus and non-aggression among members. While Cambodia insists its partnerships do not undermine ASEAN unity, its consistent alignment with Beijing on issues such as the South China Sea code of conduct has drawn friction from claimant states like Vietnam and the Philippines.

In 2024, Cambodia blocked an ASEAN joint statement criticizing China’s deployment of coast guard vessels near Second Thomas Shoal—a move widely seen as repaying Beijing’s diplomatic cover during Cambodia’s 2022 chairmanship. This pattern raises concerns about the bloc’s ability to act collectively as more members entertain tiered engagement strategies with major powers.

Yet, not all analysts see this as a zero-sum game. Some argue that Cambodia’s engagement with China could indirectly benefit ASEAN by accelerating infrastructure integration that lowers costs for all members.

“We should avoid framing this as Cambodia ‘choosing sides.’ Instead, it’s leveraging its geography to attract investment from all quarters—China just happens to be the most willing to write big checks without strings attached.”

The Long Game: Beijing’s Quiet Expansion in Mainland Southeast Asia

While much attention focuses on China’s maritime assertiveness, its quieter advance through mainland Southeast Asia may prove more consequential over the long term. Unlike the South China Sea, where overlapping claims invite resistance, Cambodia offers Beijing a cooperative partner willing to host dual-use facilities under the guise of civilian development.

The six-point consensus includes provisions for joint research on disaster relief and disease prevention—areas that allow China to establish a persistent civilian-military presence without triggering the same alarms as naval base construction. Similar models are being explored in Laos, where China has already upgraded the Vientiane–Boten railway and expressed interest in a logistics hub near the Thai border.

This approach reflects a broader shift in Chinese statecraft: from overt coercion to subtle integration, using economic interdependence to shape strategic outcomes. For global investors, the implication is clear—supply chain resilience now depends not just on diversifying production locations but on understanding the political ecology of the corridors that connect them.

As Phnom Penh prepares to host the next ASEAN summit in 2027, the question is no longer whether Cambodia will balance its relationships—but whether it still can.