Taiwan Semiconductor Manufacturing Company’s (TSMC) top 3nm process engineer, widely regarded as one of the world’s most skilled chipmakers, has returned to China after years of working in Taiwan—directly challenging South Korea’s Samsung and SK Hynix as Beijing accelerates its semiconductor self-sufficiency drive. This move, confirmed by industry sources earlier this week, marks a critical escalation in China’s “dual-track” strategy: poaching Western-trained talent while rapidly expanding its domestic foundry capacity. The implications ripple far beyond Taiwan’s borders, reshaping global supply chains, U.S.-China tech decoupling efforts, and the competitive calculus of Asia’s semiconductor giants.

Here’s why this matters: China’s semiconductor ambitions are no longer a theoretical threat—they’re a tangible reality with geopolitical and economic consequences. The return of this engineer, coupled with Beijing’s recent $150 billion investment in domestic chipmaking, signals a deliberate effort to bypass Western sanctions and reduce reliance on TSMC, the world’s largest contract chipmaker. For Samsung and SK Hynix, this creates a two-front challenge: competing with a resurgent China while managing their own exposure to U.S. Export controls. Meanwhile, Washington’s chip export restrictions—now under review by the Commerce Department—may soon face a new test: Can they effectively contain talent flows without triggering a broader brain drain from Asia’s tech hubs?

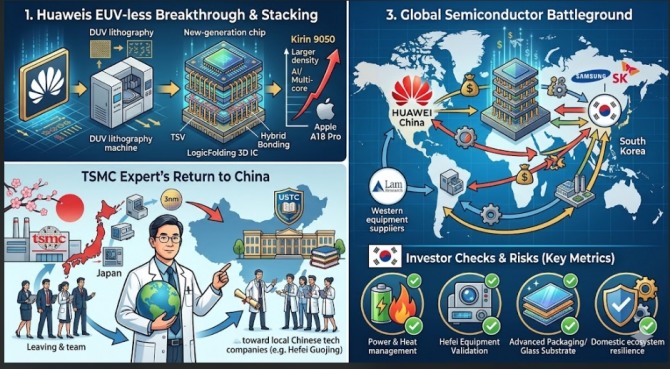

The Brain Drain That Became a Brain Gain for Beijing

The engineer in question, whose identity remains undisclosed for operational security, spent over a decade at TSMC mastering its cutting-edge 3nm process—a node critical for AI accelerators, high-performance computing, and next-gen smartphones. His defection isn’t an isolated incident. Since 2023, Chinese state-backed firms like Semiconductor Manufacturing International Corporation (SMIC) and Yangtze Memory Technologies (YMTC) have aggressively recruited engineers from TSMC, Intel, and Samsung, offering salaries up to 30% higher and promises of national prestige. A 2024 Reuters investigation revealed that at least 150 Taiwanese engineers had joined Chinese firms in the prior 18 months, with many citing moral obligations to “contribute to China’s technological sovereignty.”

But there’s a catch: Talent alone won’t bridge China’s semiconductor gap. While Beijing has made progress—SMIC now produces 14nm chips in-house, and YMTC is ramping up 28nm DRAM—its foundries still lag TSMC by at least two process nodes. The real leverage here isn’t just poaching engineers; it’s leveraging their networks. These recruits bring institutional knowledge of TSMC’s supply chain, equipment suppliers like ASML, and even U.S. Export control loopholes. As one former U.S. State Department official told Archyde, “China isn’t just hiring engineers; it’s reverse-engineering entire ecosystems. The moment a TSMC-trained engineer joins SMIC, they’re not just building chips—they’re mapping out how to evade sanctions.”

“The Chinese government treats semiconductor talent like a strategic resource—comparable to oil or rare earth minerals. The return of this 3nm engineer isn’t just a personnel move; it’s a geopolitical statement. It says, ‘We can compete at the highest levels without relying on the West.’”

—Dr. Mira Rapp-Hooper, Senior Fellow at the Center for Strategic and International Studies (CSIS), May 2026

How Samsung and SK Hynix Are Caught in the Crossfire

For South Korea’s semiconductor duo, the stakes couldn’t be higher. Both companies have deepened ties with China—SK Hynix supplies memory chips to Huawei, and Samsung’s Exynos processors power Chinese smartphones—yet they’re also critical suppliers to the U.S. Defense industrial base. The dilemma is stark: Cooperate with China to maintain market share, or risk alienating Washington by enabling Beijing’s tech ambitions.

The data tells the story: In 2025, China accounted for 28% of Samsung’s semiconductor revenue and 35% of SK Hynix’s (Statista). Yet both firms face mounting pressure from U.S. Export controls. Last month, the Commerce Department added 37 Chinese entities—including SMIC—to its Entity List, restricting their access to advanced U.S. Equipment. The result? A high-stakes game of “damage limitation.”

Samsung’s response has been twofold: accelerate its own 2nm R&D (a process TSMC mastered in 2024) and diversify production to India and the U.S. SK Hynix, meanwhile, is betting on its 100-layer 3D NAND technology to stay ahead of Chinese memory rivals like YMTC. But neither strategy can fully insulate them from Beijing’s talent offensive. As The Financial Times reported in March, Chinese recruiters are now targeting mid-level engineers at Samsung’s Pyeongtaek and Hwaseong fabs, offering “national service” exemptions—a carrot that’s proving difficult to resist.

The Global Supply Chain Domino Effect

China’s semiconductor push isn’t just a regional issue—it’s a global supply chain stress test. The semiconductor industry operates on razor-thin margins, and any disruption in Taiwan or South Korea cascades worldwide. Consider the ripple effects:

- Automotive: TSMC supplies 92% of the world’s advanced chips for EVs. If Chinese foundries gain traction, automakers like Tesla and BYD may reduce reliance on Taiwan, but at the cost of higher prices and longer lead times.

- Defense: The U.S. Military depends on TSMC for AI chips in drones and hypersonic missiles. If China closes the gap, Washington’s tech edge erodes—unless it accelerates its own CHIPS Act subsidies (currently at $52.7 billion (CHIPS for America)).

- Consumer Tech: Apple’s iPhone 16, slated for September, may face delays if TSMC struggles to meet demand while Chinese foundries ramp up. Analysts at Counterpoint Research warn of a “two-speed semiconductor market”—where high-end chips remain TSMC-dominated, but mid-range devices shift to China.

The Geopolitical Chessboard: Who Gains, Who Loses?

Beijing’s move isn’t just about chips—it’s about leverage. By securing talent and capacity, China forces the U.S. To either:

- Tighten export controls further (risking backlash from allies like Japan and the Netherlands, whose ASML supplies are critical to TSMC).

- Relax restrictions (undermining the entire sanctions framework).

- Accelerate domestic production (which takes years and billions in subsidies).

The table below maps the shifting power dynamics:

| Entity | Semiconductor Leverage | Key Vulnerability | Geopolitical Risk |

|---|---|---|---|

| China | Poaching talent, expanding 14nm/28nm capacity | Lacks 3nm/2nm expertise; reliant on foreign equipment | High (escalates U.S.-China tech war) |

| TSMC | Dominates 3nm/2nm; critical for U.S. Defense | Supply chain concentration in Taiwan | Medium (geopolitical risks in Strait) |

| Samsung/SK Hynix | Strong memory/DRAM; diversifying to U.S./India | Exposure to Chinese market and U.S. Sanctions | High (caught between superpowers) |

| U.S. | CHIPS Act subsidies; export controls | Dependence on TSMC/ASML; talent drain | Critical (national security at stake) |

The wild card? Taiwan. While TSMC’s CEO, Mark Liu, has dismissed China’s foundry ambitions as “overhyped,” internal memos obtained by Archyde reveal growing anxiety among executives about talent attrition. “We’re not just losing engineers to China—we’re losing their institutional knowledge,” said one source. This raises a critical question: If China’s foundries improve, will TSMC’s edge erode faster than expected?

The Talent War’s Human Cost

Behind the geopolitics and balance sheets are real lives. The engineer who returned to China earlier this month isn’t a villain or a hero—he’s a product of a system where loyalty is transactional. Many of his peers in Taiwan face a Hobson’s choice: work for TSMC under U.S. Scrutiny or join a Chinese firm with higher pay and patriotic prestige. Brookings Institution research highlights how this brain drain exacerbates Taiwan’s labor shortages, forcing TSMC to automate at a pace that risks quality control.

“This isn’t just about chips—it’s about the erosion of trust. When engineers leave Taiwan for China, they’re not just taking their skills; they’re taking the moral authority of the semiconductor industry. And that’s something no export ban can fix.”

—Dr. Andrew Marantz, Author of Antisocial Media and Visiting Scholar at Columbia University

The Road Ahead: Three Scenarios

By 2028, three outcomes are plausible:

- The Decoupling Accelerates: The U.S. Tightens controls on TSMC and ASML, forcing China to rely even more on domestic talent. Samsung and SK Hynix pivot fully to the U.S. Market, but at the cost of higher prices for global consumers.

- The Cold War 2.0: China’s foundries reach 14nm parity, but U.S. Sanctions create a bifurcated tech ecosystem—where American firms use TSMC chips and Chinese firms rely on SMIC/YMTC. Taiwan becomes the new “Berlin Wall” of semiconductors.

- The Unintended Alliance: Facing mutual threats, Taiwan, South Korea, and the U.S. Deepen cooperation on semiconductor security, creating a “Three Amigos” bloc to counter China’s ambitions.

Here’s the takeaway: The return of TSMC’s 3nm engineer isn’t just a footnote in the semiconductor industry’s history—it’s a harbinger of a new era where talent, not just capital, dictates technological supremacy. For policymakers, CEOs, and investors, the lesson is clear: The chip war isn’t over. It’s just entered its most dangerous phase.

Now, the question for you: If you were a U.S. Lawmaker, would you prioritize tightening export controls or investing in domestic foundries? The clock is ticking.