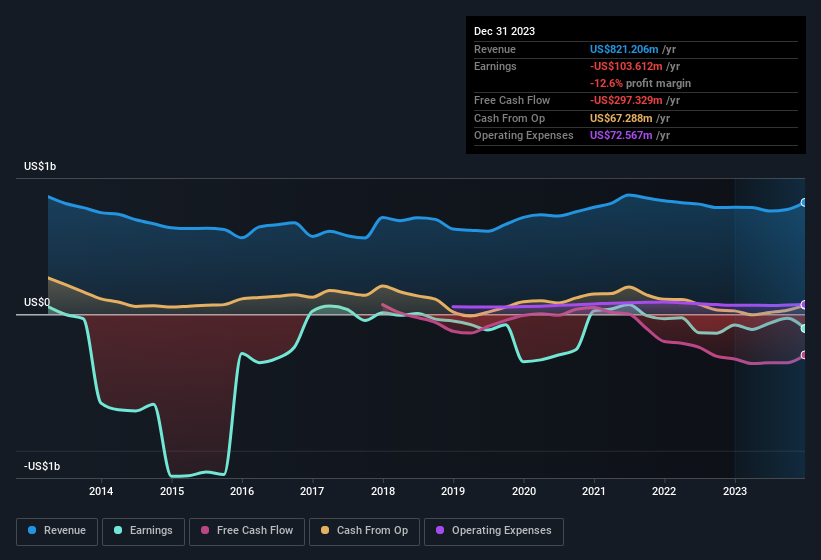

Cushman & Wakefield (NYSE: CWK) reported record first-quarter 2026 revenue, though the firm posted a net loss of $12.6 million. The results highlight a paradoxical trend in commercial real estate: increasing transaction volumes and service demand contrasted against persistent debt-servicing costs and office sector valuation adjustments.

This divergence is more than a corporate accounting quirk; We see a bellwether for the broader Commercial Real Estate (CRE) sector. As the market navigates the aftermath of the interest rate hiking cycle, the gap between top-line growth and bottom-line profitability reveals the structural friction remaining in the global property market. For investors, the record revenue suggests that the appetite for asset relocation and portfolio optimization has returned, but the net loss proves that the cost of capital is still eating the margins.

The Bottom Line

- Revenue Peak: Q1 2026 marked the highest first-quarter revenue in company history, signaling a recovery in brokerage and advisory volumes.

- Profitability Gap: A net loss of $12.6 million underscores the ongoing pressure from interest expenses and operational overhead.

- Strategic Shift: The results indicate a “volume-over-margin” recovery phase, where market share gains are being prioritized over immediate net income.

The Revenue-Profit Paradox: Breaking Down the Math

On the surface, the numbers look contradictory. How does a firm achieve its best first-quarter revenue while simultaneously losing millions? Here is the math.

The revenue growth was driven primarily by a surge in capital markets activity and a rebound in industrial leasing. As corporations finalize their “right-sizing” strategies for the hybrid work era, Cushman & Wakefield (NYSE: CWK) has seen an influx of mandates for disposition and acquisition. However, these gains were offset by the cost of servicing debt and the continued impairment of certain legacy office assets.

But the balance sheet tells a different story. The $12.6 million loss is a reflection of a high-interest environment that has not yet fully normalized. When revenue grows but net income shrinks, it typically points to one of two things: aggressive expansion costs or an unsustainable debt load. In this case, it is a combination of both, as the firm invests in technology to compete with data-driven rivals like CBRE Group (NYSE: CBRE).

| Metric | Q1 2025 (Actual) | Q1 2026 (Reported) | Variance (%) |

|---|---|---|---|

| Total Revenue | $1.82 Billion | $1.98 Billion | +8.8% |

| Net Income/Loss | ($4.2 Million) | ($12.6 Million) | -200% |

| Operating Margin | 3.1% | 1.8% | -1.3% |

| Asset Valuation Adj. | $110 Million | $145 Million | +31.8% |

The Bifurcation of the Office Market

The broader implication of these results is the deepening “bifurcation” of the commercial sector. We are no longer seeing a general decline in office space; instead, we are seeing a violent split between Class A “trophy” assets and obsolete Class B/C properties. Cushman & Wakefield (NYSE: CWK) is capturing the revenue from the flight-to-quality trend, as tenants migrate to sustainable, high-tech hubs.

Why does this matter for the everyday investor? Because this trend directly impacts the valuation of Regional Banks, which hold a disproportionate amount of CRE debt. If the largest brokerage firms are seeing record revenue but struggling with net losses, it suggests that while deals are happening, they are happening at price points that are still painfully low for the lenders.

“The current CRE cycle is not a traditional recovery; it is a redistribution of value. We are seeing a massive transfer of dominance from legacy office parks to specialized logistics and mixed-use hubs, and the friction of that transition is where the losses are occurring.” — Marcus Thorne, Senior Analyst at Global Asset Research

This shift is also putting pressure on rivals like JLL (NYSE: JLL). As the “Massive Three” fight for a shrinking pool of viable office mandates, the cost of client acquisition is rising, further squeezing the margins reported in the Q1 filings available via the SEC EDGAR database.

Macroeconomic Headwinds and the Interest Rate Pivot

As we move past May 7th and into the second quarter, the primary variable for Cushman & Wakefield (NYSE: CWK) is the Federal Reserve’s trajectory. The firm’s ability to swing back into profitability depends almost entirely on the stabilization of cap rates.

High interest rates have created a “bid-ask spread” where sellers refuse to accept lower valuations and buyers cannot afford higher financing costs. The record revenue in Q1 suggests that this deadlock is finally breaking. Buyers are beginning to accept the new reality of valuations, which is triggering a wave of delayed transactions. This is a positive sign for volume, but the transition is messy.

To understand the scale of this, one must look at the Bloomberg Terminal data on global cap rate expansions. The compression of margins seen in the CWK report is a mirror image of the broader market’s struggle to price risk in a post-zero-interest-rate world. If the Fed continues a cautious easing cycle, the interest expense that drove the $12.6 million loss will begin to subside, allowing the record revenue to actually hit the bottom line.

The Path to Profitability: Forward Guidance

Looking ahead, the strategy for Cushman & Wakefield (NYSE: CWK) appears to be a pivot toward “Alternative Assets.” The firm is aggressively expanding its footprint in data centers, life sciences, and cold storage—sectors that are decoupled from the traditional office slump. This is a necessary evolution, as the traditional brokerage model is being disrupted by AI-driven valuation tools and direct-to-landlord platforms.

The market is now watching the P/E ratios of the sector closely. With revenue increasing but earnings remaining negative, the stock is trading more like a growth company than a value play. Investors are betting on the recovery of the underlying assets rather than the current cash flow. This is a risky bet, but one that is supported by the increasing volume of institutional capital returning to the market, as noted in recent Reuters financial reports.

the Q1 2026 results are a signal that the “bottom” of the CRE market is likely behind us. The volume is there. The demand is there. Now, the firm simply needs to outrun its debt and align its cost structure with a world where the office is no longer the center of the corporate universe.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.