{kind=link}

“`html

Credit Recovery: Enhanced Debt Adjustment Plan Offers Relief to Vulnerable Groups and self-Employed

Table of Contents

- 1. Credit Recovery: Enhanced Debt Adjustment Plan Offers Relief to Vulnerable Groups and self-Employed

- 2. Expanded Debt Relief For Vulnerable Groups

- 3. Tailored Support For Self-Employed Workers

- 4. Key Changes To Debt Adjustment Programs

- 5. Preemptive Debt Reconciliation Becomes Permanent

- 6. What are the potential drawbacks of using a Debt Management Plan (DMP) for self-employed individuals with fluctuating income?

- 7. Debt Relief for Vulnerable & Self-Employed: A Comprehensive Guide

- 8. Understanding Vulnerable Individuals & Self-Employed Debt

- 9. Defining Vulnerability in a Financial Context

- 10. The Unique Challenges of Self-Employed Individuals

- 11. Available Debt Relief Options

- 12. Debt Counselling

- 13. Debt Management Plans (DMPs)

- 14. debt Settlement

- 15. Bankruptcy

- 16. Eligibility and Application

- 17. Critically importent Documents Required

- 18. Where to Find Help

- 19. Practical Tips for Debt Management

- 20. Additional Resources

Breaking Now: New Measures Designed To Ease Financial Strain On Vulnerable Populations And Self-Employed Individuals Struggling With Debt Have Been Unveiled. Effective June 30th, 2025, These Adjustments Aim To Provide More Flexible And Forgiving Terms For Those Most in Need Of Credit Recovery.

Expanded Debt Relief For Vulnerable Groups

Important changes are coming to debt adjustment programs, offering a lifeline to those grappling with financial instability. The Focus Is On Providing Customized Support Based On Individual Circumstances, Specifically Targeting Vulnerable Groups And Self-Employed Workers.

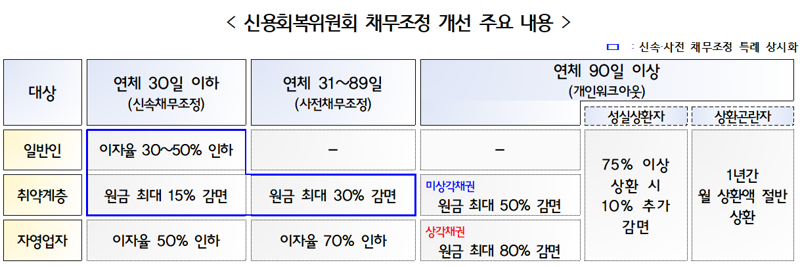

- Increased Principal exemption: For vulnerable individuals overdue by more than 90 days, the maximum principal exemption rises from 30% to 50%.

- Flexible Repayment Plans: Recognizing that income can fluctuate, debtors can now adjust their monthly payments, providing a temporary respite during financial hardships. Instead of paying the same amount monthly, debtors can now opt to pay a reduced amount for a set period.

Tailored Support For Self-Employed Workers

self-employed individuals facing debt challenges will receive enhanced support through these new measures. The Degree Of Principal Reduction Will Depend On The Overdue Period.

- Varying Principal Reduction: Self-employed individuals can see principal reductions of up to 80%, depending on how long they have been overdue.

- Incentives For Faithful Repayment: those who consistently repay their debts after receiving adjustments will receive an additional 10% exemption on the remaining balance.

Pro tip: If you are a self-employed individual struggling with debt, explore these new measures and consult with a financial advisor to create a repayment plan that works for you.

Key Changes To Debt Adjustment Programs

The Credit Recovery Committee’s proclamation detailed initiatives that build upon existing programs to provide more comprehensive debt relief. These adjustments reflect the Financial Services Commission’s commitment to stabilizing public welfare through targeted financial support.

The following table summarizes the key changes to debt adjustment programs:

| feature | Previous | New |

|---|---|---|

| Principal Exemption (Vulnerable) | Up to 30% | Up to 50% (Overdue > 90 Days) |

| Principal Reduction (Self-Employed) | Up to 70% | Up to 80% (Depending on Overdue Period) |

| Repayment Flexibility | Fixed Monthly Payments | Adjustable Payments Based on Income |

| Incentives for Repayment | None | 10% exemption on Remaining Debt After 75% Repayment |

Preemptive Debt Reconciliation Becomes Permanent

The temporary preemptive debt reconciliation program is now permanent. This initiative aims to ease the burden of interest repayment for those facing delinquency or short-term overdue notices.

- Expanded Eligibility: The program now includes individuals in the bottom 20% of credit ratings,up from the bottom 10

What are the potential drawbacks of using a Debt Management Plan (DMP) for self-employed individuals with fluctuating income?

Debt Relief for Vulnerable & Self-Employed: A Comprehensive Guide

Financial hardship can affect anyone, but certain groups, including vulnerable individuals and the self-employed, may face heightened challenges. This article explores debt relief options specifically designed to help you navigate financial difficulties and regain stability. We’ll delve into various programs, eligibility criteria, and practical steps to find the right solution for your situation. Understanding your rights and available resources is crucial to managing debt effectively.

Understanding Vulnerable Individuals & Self-Employed Debt

Vulnerable individuals often experience financial difficulties alongside other challenges such as disability, age-related issues, or reliance on social security. Self-employed individuals, while enjoying the flexibility of their work, may have fluctuating income and limited access to traditional safety nets.

Defining Vulnerability in a Financial Context

Vulnerability in relation to debt can be defined by several factors. this frequently enough includes, but is not limited to:

- Low Income: Those with incomes below a certain threshold are at a higher risk of debt.

- Health Issues: Medical expenses can lead to financial struggles.

- Age-Related Challenges: Older adults often face fixed incomes and may experience age-related health concerns.

- Disability: Those with disabilities may face barriers to employment and increased expenses.

The Unique Challenges of Self-Employed Individuals

self-employment brings unique financial challenges. The lack of a steady paycheck, limited access to employer-sponsored benefits and irregular income streams can make debt management more difficult. Fluctuations in revenue and expenses can create vulnerabilities, especially during economic downturns.

Available Debt Relief Options

Several debt relief options exist to help vulnerable and self-employed individuals. It’s essential to research and determine which option best suits your circumstances. Consider factors such as the type of debt, your income, and your long-term financial goals.

Debt Counselling

Debt counseling provides personalized guidance and assistance in managing debt. Certified debt counselors work with you to assess your financial situation, create a budget, and negotiate with creditors. This can lead to lower payments and interest rates, making your debt more manageable. Seeking professional advice is a key first step to managing your financial well-being.

Debt Management Plans (DMPs)

A Debt Management Plan (DMP) is often offered by debt counseling agencies. Under a DMP, you make a single monthly payment to the agency, who then distributes it to your creditors. DMPs commonly include lower interest, and are beneficial in consolidating multiple credit card debts. They can help you avoid bankruptcy if applicable. Though note that DMPs affect your credit score.

debt Settlement

Debt settlement involves negotiating with creditors to pay off your debt for less than the full amount owed. This may reduce the total debt amount. This may be a viable option but it can negatively impact your credit score.

Bankruptcy

When other options are unsuccessful, filing for bankruptcy, such as Chapter 7 or Chapter 13, may be considered a last resort. This provides legal protection from creditors and may allow you to eliminate certain debts.Though, bankruptcy has lasting impacts on your credit history.

Eligibility and Application

eligibility requirements for debt relief programs vary. Generally, you’ll need to demonstrate:

- Financial Hardship: A demonstrable inability to meet your debt obligations.

- Income and Expenses: Assessments of your income, essential living expenses, and current debts.

Critically importent Documents Required

To apply for debt relief, you will typically need to provide:

- Proof of income (pay stubs, tax returns).

- Bank statements.

- List of debts and creditors.

- List of assets.

Where to Find Help

Several resources can support your debt relief journey. It’s wise to assess government schemes, non-profit agencies provide free counseling and are useful.

Resource Description Benefits Non-profit credit counseling agencies Provide free or low-cost budgeting and debt counseling. free or low-cost advice,negotiating with creditors. Government programs Vary county by county, they may offer cash assistance or debt assistance. May decrease the burden if applicable Legal professionals (check for Pro bono services) May provide legal advice and represent you. Legal advocacy, representation in court. Practical Tips for Debt Management

Alongside debt relief options, proactive measures are crucial for financial stability. This includes budgeting, building an emergency fund, and learning debt management basics. A solid financial plan is key to financial freedom.

- Create a Budget: Track income and expenses to understand where your money goes.

- Build an emergency fund: Helps cover unexpected financial shocks.

- Prioritize Debts: Focus on paying off high-interest debts first.

- Seek Professional Advice: Consult with a financial advisor for personalized help.

Additional Resources

There are many ways to get more information.

- Government websites: Consult government agencies for information about debt relief programs.

- Nonprofit organizations: Debt counseling agencies and other nonprofits provide educational materials and resources.