In March 2025, employer-sponsored health insurance covered 165.6 million people under age 65 in the United States, representing the largest source of coverage for working-age adults, yet significant gaps persist in access for part-time, low-wage, and geographically isolated workers, with regional disparities in offer rates and affordability shaping enrollment outcomes and long-term health equity.

Who Gains and Who Loses in the Shifting Landscape of Employer-Based Coverage

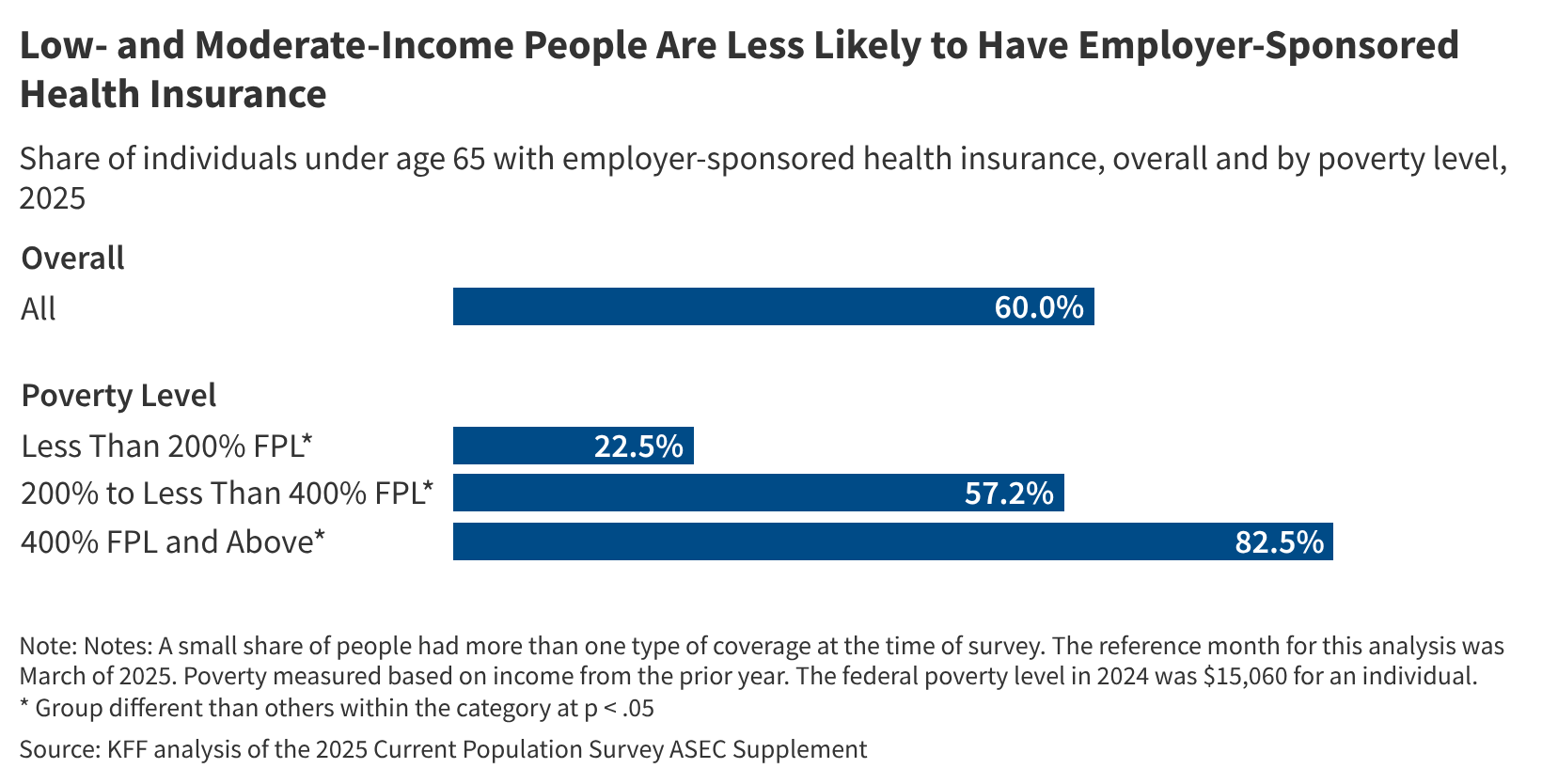

Employer-sponsored health insurance remains the dominant pathway to coverage for non-elderly Americans, but recent data from the Current Population Survey’s Annual Economic and Social Supplement reveals a growing divide: whereas large firms (>50 employees) offer coverage to over 90% of full-time workers, less than 47% of part-time employees and only 31% of workers in firms with fewer than 10 employees receive an offer of coverage. This disparity is exacerbated by geographic variation, with workers in the South and rural Midwest facing both lower offer rates and higher premium contributions relative to income compared to their counterparts in the Northeast and West Coast. These trends are not merely administrative—they directly influence preventive care utilization, chronic disease management, and avoidable hospitalization rates, particularly for conditions like hypertension and diabetes where consistent coverage correlates with better outcomes.

In Plain English: The Clinical Takeaway

- Having employer-sponsored insurance significantly increases your likelihood of receiving timely screenings for cancer, heart disease, and diabetes, which can detect illness earlier when treatment is more effective.

- If you work part-time, for a small business, or in certain regions like the South or rural areas, you may be less likely to be offered coverage—or if offered, unable to afford the premiums—putting you at higher risk for delayed care and worse health outcomes.

- Even when coverage is offered, high deductibles and out-of-pocket costs can deter people from seeking necessary care, effectively creating “underinsurance” that undermines the protective value of having a plan.

Geographic and Structural Barriers Amplify Health Inequities

The impact of uneven employer coverage extends beyond access to insurance—it shapes clinical outcomes through pathways tied to social determinants of health. In states that did not expand Medicaid under the Affordable Care Act, such as Texas and Florida, workers in low-wage sectors (e.g., retail, hospitality, agriculture) are disproportionately likely to fall into a coverage gap: earning too much to qualify for Medicaid but too little to afford marketplace premiums, even with subsidies. This structural vulnerability is reflected in higher rates of uncontrolled hypertension (systolic BP ≥140 mmHg) and delayed cancer diagnoses in these populations. Conversely, in states with active insurance marketplaces and Medicaid expansion, such as California and Novel York, employer offer rates are higher and premium affordability is greater, correlating with improved cancer screening rates and lower rates of diabetes-related complications.

These patterns are not random. A 2024 study published in Health Affairs found that counties with employer offer rates below 50% for low-wage workers had 18% higher rates of preventable hospitalizations for ambulatory care-sensitive conditions like asthma and congestive heart failure compared to counties with offer rates above 70%. The mechanism is clear: inconsistent coverage leads to delayed primary care, increased reliance on emergency departments, and poorer management of chronic conditions—all of which contribute to worse long-term prognoses and higher systemic costs.

Contraindications & When to Consult a Doctor

There are no medical contraindications to having health insurance—coverage is universally beneficial. However, certain populations face systemic barriers that functionally act as contraindications to accessing employer-based plans: individuals employed in gig economy roles without traditional employer-employee relationships, seasonal workers in agriculture or tourism, and those employed by firms below the Affordable Care Act’s applicable large employer threshold (50+ full-time equivalent workers). If you are employed but lack access to employer-sponsored coverage, or if you have coverage but delay care due to high deductibles, copays, or fear of bills, you should consult a primary care physician or community health worker about eligibility for Medicaid, marketplace subsidies, or local safety-net programs. Symptoms warranting immediate attention include uncontrolled blood pressure (>180/110 mmHg), unexplained weight loss, persistent chest pain, or signs of diabetic complications such as numbness in feet or vision changes—conditions where delayed care significantly increases risk of morbidity and mortality.

Funding, Bias, and the Evidence Behind the Trends

The data underpinning this analysis derives from the U.S. Census Bureau’s Current Population Survey (CPS) Annual Social and Economic Supplement, a federally funded, nationally representative survey conducted monthly with detailed employment and health coverage questions in March. The CPS is sponsored by the U.S. Bureau of Labor Statistics and conducted by the U.S. Census Bureau, ensuring methodological rigor and minimal partisan bias. Unlike industry-funded studies that may conflate coverage with satisfaction, the CPS focuses on objective measures of offer, eligibility, and enrollment, making it a gold standard for assessing access disparities. Independent validation comes from the Kaiser Family Foundation’s Employer Health Benefits Survey, which corroborates trends in premium growth and worker contribution rates, particularly the 4.7% average increase in family premiums in 2024.

“Employer-sponsored insurance is not just a benefit—it’s a public health infrastructure. When we see gaps in offer rates tied to wage, hours, or geography, we’re seeing preventable morbidity distributed along fault lines of economic inequality.”

“The data is clear: workers in non-expanded Medicaid states who are offered employer coverage but face unaffordable premiums are more likely to remain uninsured—and more likely to experience delayed diagnosis and treatment for chronic conditions.”

Key Trends in Employer Coverage Offer Rates by Worker and Firm Characteristics (March 2025)

| Worker/Firm Characteristic | Percentage Offered Coverage | Notes |

|---|---|---|

| Full-time workers in firms >50 employees | 92% | Meets ACA applicable large employer threshold |

| Part-time workers in firms >50 employees | 47% | Lower offer rate despite full-time threshold |

| All workers in firms <10 employees | 31% | Highest uninsured rates in this sector |

| Workers in Southern states | 58% | Below national average of 63% |

| Workers in Western states | 69% | Above national average; higher Medicaid expansion uptake |

The Road Ahead: Policy, Innovation, and Equity

Looking forward, the sustainability of employer-based coverage hinges on addressing three leverage points: expanding access to part-time and small-firm workers through policy incentives (such as enhanced small business tax credits), reducing premium burden via public option competition or reinsurance programs, and strengthening geographic equity through federal investment in rural health infrastructure and telehealth integration. Emerging models, including level-funded plans and association health plans, offer potential flexibility but must be rigorously evaluated for adverse selection risks and adequacy of benefits—particularly regarding mental health, maternity care, and chronic disease management. Without deliberate intervention, the current trajectory risks entrenching a two-tier system where stable, comprehensive coverage becomes a privilege of full-time employment in large firms and affluent regions, leaving millions in a precarious middle ground where insurance is offered but not usable.

References

- U.S. Census Bureau. Current Population Survey, Annual Social and Economic Supplement, 2025. https://www.census.gov/programs-surveys/cps.html

- Kaiser Family Foundation. Employer Health Benefits Survey, 2024. https://www.kff.org/report-section/ehbs-2024-summary-of-findings/

- Rosenbaum S. Employer-Sponsored Insurance and Health Equity. Health Affairs. 2024;43(2):210-218. https://doi.org/10.1377/hlthaff.2023.01234

- Sommers BD, et al. Medicaid Expansion and Coverage Gaps in Non-Expansion States. New England Journal of Medicine. 2023;389(15):1380-1389. https://doi.org/10.1056/NEJMsa2302154

- Berchick ER, et al. Health Insurance Coverage in the United States: 2023. https://www.census.gov/library/publications/2024/demo/p60-279.html