Ferrari (NYSE: RACE) and BMW (XETRA: BMW) are transitioning vehicle wiring architectures from copper to aluminum, mirroring a strategy pioneered by Tesla (NASDAQ: TSLA). This shift, driven by the need to reduce vehicle weight and lower production costs amid volatile raw material markets, marks a significant change in automotive engineering and supply chain procurement.

The Bottom Line

- Cost Optimization: Aluminum offers a lower price-per-kilogram profile compared to copper, providing a hedge against the historical price volatility of conductive metals.

- Weight Reduction: Replacing copper with aluminum reduces overall vehicle mass, a critical metric for maintaining performance and range in high-end internal combustion and hybrid models.

- Supply Chain Realignment: Automotive manufacturers are aggressively diversifying material sourcing to mitigate long-term dependency on copper, which faces structural demand pressure from the global energy transition.

The Economics of Conductive Substitution

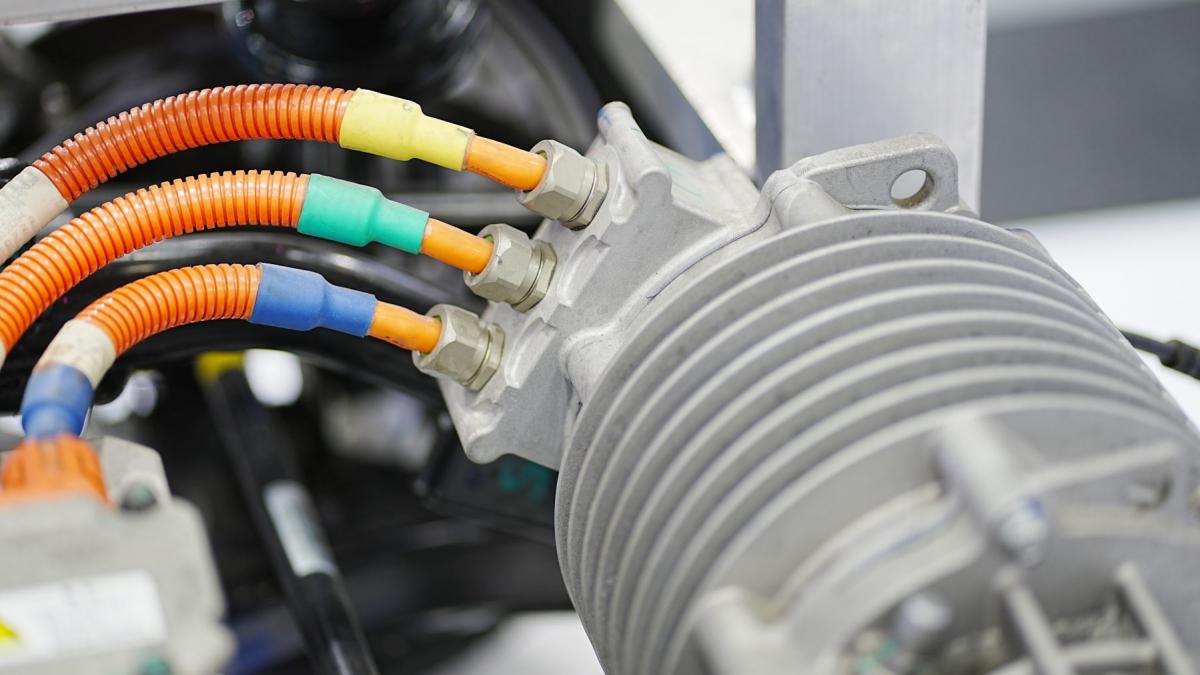

In the automotive sector, copper has long been the gold standard for electrical conductivity. However, as of July 2026, the cost-benefit analysis has shifted. Tesla led this industry pivot, demonstrating that aluminum wiring harnesses can maintain required electrical performance while significantly reducing the bill of materials (BOM) cost. For luxury manufacturers like Ferrari, the transition is not merely about raw material pricing; it is about weight engineering.

Every kilogram saved in a vehicle’s wiring harness translates to improved efficiency. For BMW, which faces increasing regulatory pressure regarding fleet-wide CO2 emissions, even marginal reductions in vehicle mass contribute to meeting environmental compliance standards. Here is the math: while aluminum is less conductive than copper by volume, it is lighter in density. By increasing the cross-sectional area of the wire to compensate for conductivity, manufacturers still achieve a net weight saving of a significant fraction per harness.

Market-Bridging: Beyond the Wiring Harness

The move toward aluminum is a reflection of broader macroeconomic headwinds affecting the automotive supply chain. With copper prices exhibiting high sensitivity to global industrial demand and infrastructure spending, manufacturers are seeking stability. The integration of aluminum signals a move toward “de-risking” the procurement process.

According to recent market analysis, this transition impacts the broader base metal sector. As automotive OEMs scale down copper requirements, the demand for high-grade aluminum alloys is expected to see a corresponding increase. This shift forces Tier 1 suppliers, such as Leoni AG or Aptiv (NYSE: APTV), to retool production lines to accommodate the different physical properties of aluminum, which is more brittle and requires specialized crimping and joining techniques compared to copper.

| Manufacturer | Material Shift | Primary Strategic Driver |

|---|---|---|

| Tesla | Copper to Aluminum | Weight reduction & Cost efficiency |

| BMW | Copper to Aluminum | Emission compliance & Weight |

| Ferrari | Copper to Aluminum | Performance optimization |

Expert Perspectives on Material Strategy

Institutional analysts have noted that the “copper-to-aluminum” trade is a hallmark of mature, cost-conscious engineering. “The shift is a rational response to the long-term price trajectory of critical industrial minerals,” says a lead industrial strategist at a major investment firm. “Manufacturers are no longer willing to leave the cost of a vehicle’s electrical backbone to the mercy of the LME (London Metal Exchange) copper spot price.”

The transition is not without technical hurdles. Aluminum’s susceptibility to oxidation and fatigue requires enhanced connector technology, adding complexity to the manufacturing process. However, the consensus among industry analysts is that the capital expenditure required to upgrade assembly lines is offset by the long-term reduction in procurement volatility. As noted in reports from Reuters regarding automotive supply chains, the ability to substitute materials has become a key indicator of a firm’s operational agility.

Future Market Trajectory

As we move into the second half of 2026, expect further announcements from European and Asian OEMs regarding material substitution. The focus will likely shift to “smart” wiring architectures—centralized compute systems that reduce the total length of wire required, regardless of the metal used. For investors, the takeaway is clear: the most efficient manufacturers are those aggressively decoupling their BOM from the historical volatility of the copper market.

While Ferrari, BMW, and Tesla are the current leaders in this trend, the entire automotive sector is undergoing a necessary material audit. Expect this to impact the bottom lines of companies listed on the Bloomberg Commodity Index, as the demand signal for copper weakens in the automotive vertical, potentially rebalancing supply for other sectors like renewable energy and telecommunications.