{kind=link}

Breaking: FHA Mortgage Ban Excludes H‑1B and Other Non‑Permanent Residents, Sparking Market Ripples

Table of Contents

- 1. Breaking: FHA Mortgage Ban Excludes H‑1B and Other Non‑Permanent Residents, Sparking Market Ripples

- 2. What Happened And Who Is Impacted

- 3. Why This Matters For Buyers, Renters And Local markets

- 4. Markets Most Exposed

- 5. Broader Context: migration, Hiring, And Rental Demand

- 6. Short‑Term Effects Versus long‑Run Shifts

- 7. Where Conventional Lending Stands

- 8. Questions For Readers

- 9. Evergreen Analysis: What Investors And Policymakers Should Watch

- 10. frequently Asked Questions

- 11. Okay, here’s a breakdown of the provided text, summarizing the key data and organizing it for clarity. I’ll focus on the core changes, implications, and advice.

- 12. FHA Rule Shuts Down Mortgage Lock Surge for Non-Permanent Residents

- 13. What the New FHA Rule Entails

- 14. Impact on Mortgage rate Locks

- 15. 1. Lock‑Duration Limits

- 16. 2. Re‑underwriting Requirement

- 17. 3. Lender Compliance Checklist

- 18. Eligibility Changes for Non‑Permanent Residents

- 19. Practical implication

- 20. Practical Tips for Prospective Borrowers

- 21. Case Study: Real‑World Example (2025 Q2)

- 22. Benefits and Drawbacks of the New Rule

- 23. Benefits

- 24. Drawbacks

- 25. Guidance for Lenders and Mortgage Professionals

- 26. Frequently Asked Questions (FAQ)

Published: 2025-12-06

Federal Rules That blocked H‑1B Holders From New FHA Loans Began In Late May 2025, And The Change Has Already Driven A Dramatic Fall In FHA Mortgage Locks For Non‑Permanent Residents.

What Happened And Who Is Impacted

Federal Policy That Took effect In Late May 2025 Bars H‑1B Visa Holders And Other Non‑Permanent Residents from Obtaining New FHA Mortgages.

Data Tracked Through September 2025 Shows The Share Of FHA mortgage Locks by Non‑Permanent Residents Dropped From 3.8 Percent In September 2024 To 0.2 Percent A Year Later.

Why This Matters For Buyers, Renters And Local markets

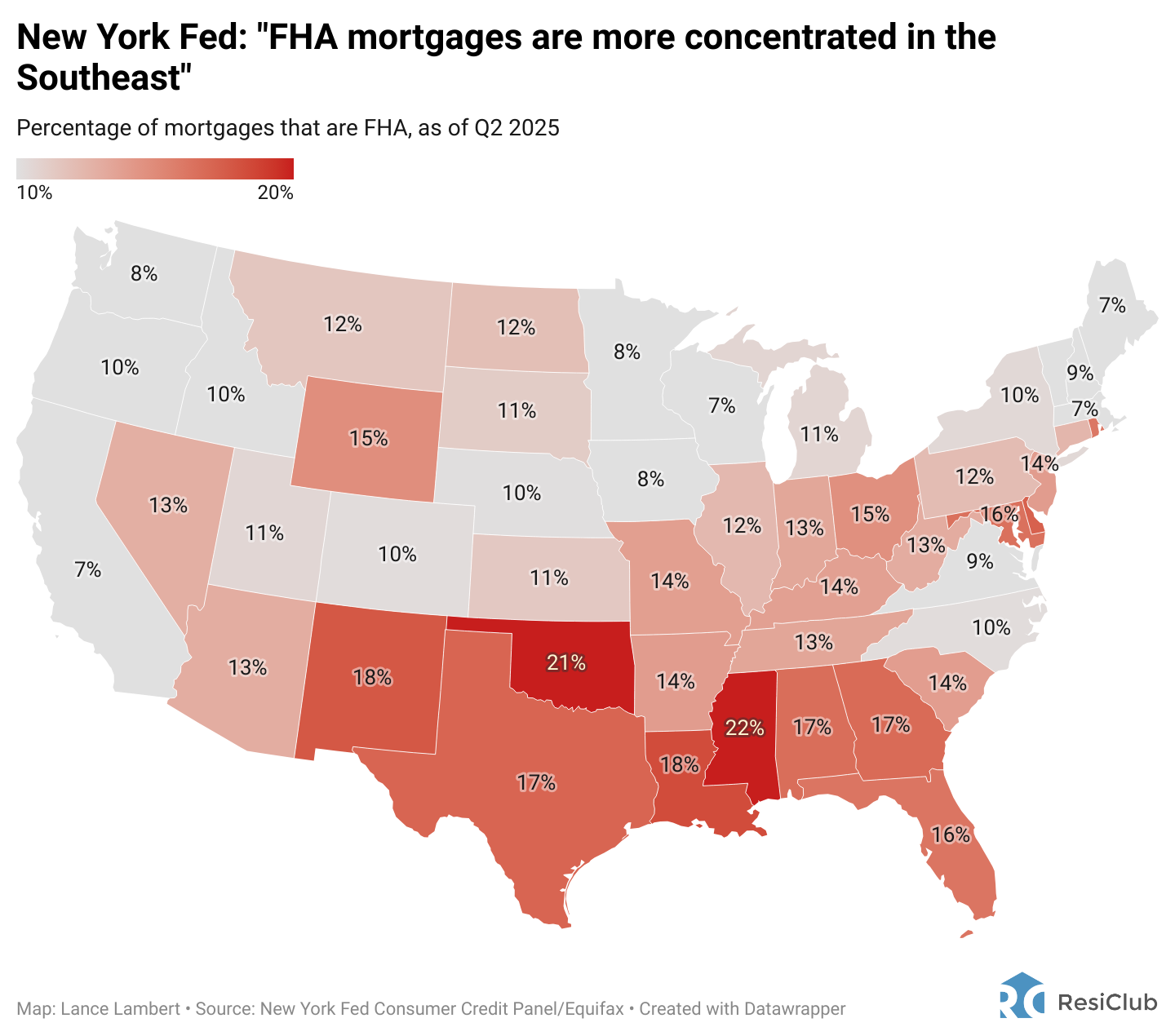

FHA Loans Represent A Noticeable Slice of Purchase activity But only A Minority Of Total Mortgage Debt.

Optimal Blue Reported FHA Loans Accounted For About 22.0 Percent Of U.S. Mortgage‑Purchase Locks In September 2025, While The federal Reserve Bank Of New York estimates FHA Debt At roughly 12 Percent Of The Nation’s $12.94 Trillion Mortgage Stock As Of June 2025.

| Item | Key Fact |

|---|---|

| Policy Change | H‑1B And Other Non‑Permanent Residents Banned From New FHA Mortgages (Effective Late May 2025) |

| Impact on FHA Locks | Share For Non‑Permanent Residents Fell From 3.8% (Sept 2024) To 0.2% (Sept 2025) |

| FHA Share Of Purchase Locks | 22.0% Of U.S. Purchase Locks (Sept 2025) – Optimal Blue |

| FHA Share Of mortgage Debt | Approx. 12% Of $12.94 Trillion Mortgage Debt (June 2025) – New York Fed |

| Net Migration Forecast | AEI Range For 2025: +115,000 To -525,000 |

Markets Most Exposed

States And Metro Areas With The Highest Concentration Of High‑Salary H‑1B Workers Include Washington, California, New York, New Jersey, Texas, And The District Of Columbia.

Growth Markets With Substantial Homebuilding Activity – Such As Dallas, Fayetteville, And Durham – Could Feel A Sharper Near‑Term Slowdown In Demand From This Specific FHA Policy Shift.

Did You Know? The Share Of FHA Mortgage Locks Held By Non‑Permanent Residents Spiked Between 2020 And 2024 Before Collapsing After The 2025 Policy Change.

Broader Context: migration, Hiring, And Rental Demand

The Surge In Net International Migration From 2021 Through Mid‑2024 Helped Support Rental And Entry‑level Homebuying Demand.

That Wave Has Receded, And Forecasts Such As Those From The American Enterprise Institute Show A wide Range For 2025 Migration, From A Modest Inflow To A Moderate Outflow.

Employers That Rely on H‑1B Talent Have Reacted To Related Policy Moves; Some Reported Pauses In new H‑1B Hiring In Late 2025 After Proposed Fees And Restrictions.

Pro Tip: Landlords And Investors Should Monitor Local Mortgage Originations, Visa‑petition Activity, and employer Hiring Trends To Gauge Short‑Run Rental demand.

Short‑Term Effects Versus long‑Run Shifts

All Else Equal, Fewer New Immigrants And Restricted Access To FHA Financing For Non‑permanent Residents Will Likely Lower Aggregate Rental Demand At The Lower End Of The Market.

Major Metro Areas That Drew Large Numbers Of Immigrants In Recent Years-Including New York, Miami, Dallas, And Houston-Are Most Likely To See Noticeable Effects.

Where Conventional Lending Stands

ResiClub Observers Note That Conventional Mortgages Backed By Fannie Mae And Freddie Mac Had Not Shown A Comparable Shift At the Time Of Reporting.

Questions For Readers

Do You Live In A Market That Relies Heavily On H‑1B Workers Or Recent Immigrant Inflows?

Are You A Real Estate Professional Tracking How Financing Changes Affect Local Inventory And Rents?

Evergreen Analysis: What Investors And Policymakers Should Watch

Monitor Mortgage Origination mixes, Employer H‑1B filings, And Local Rental Vacancies To assess Whether The Policy Shift Produces Temporary Dislocations Or Longer‑Term Demand changes.

Consult Data From Nationwide Mortgage Processors And central Banks For Timely Signals; Sources Include Optimal Blue, The Federal Reserve Bank Of New york, And Self-reliant Research Firms.

High‑Income Labor Pools Tend To Support Higher Homebuying Rates,So Policy That Constrains Access For Those workers Can Dampen Both For‑Sale And Rental markets.

Financial Disclaimer: This Article Is For Informational Purposes And dose Not Constitute Financial Advice. Consult A Licensed Mortgage Professional for Guidance On Lending Eligibility.

frequently Asked Questions

- What Is The FHA mortgage Ban? the FHA Mortgage Ban Refers To The Late May 2025 Rule That Prevents H‑1B Visa holders And Other Non‑Permanent Residents From Taking Out New FHA Loans.

- Who Fell Most Affected By The FHA mortgage Ban? Non‑Permanent Residents, Including H‑1B Holders, Saw Their Share Of FHA Mortgage Locks Fall Sharply After The Ban.

- How Big Was The drop In FHA Mortgage Locks For Non‑Permanent Residents? The Share Fell From 3.8 Percent In September 2024 To 0.2 percent In September 2025, According to Market Data.

- does The FHA Mortgage Ban Affect Conventional Loans? At The Time Of Reporting,There Was No Comparable Shift Reported In Fannie mae Or Freddie Mac Conventional Lending.

- Which Markets Are most Exposed To The FHA Mortgage Ban? Markets With High Concentrations Of H‑1B Workers, Such As Washington, California, New York, New Jersey, Texas, And The District Of Columbia, are Most Exposed.

Sources And Further Reading: Optimal Blue,Federal Reserve Bank Of New York,American Enterprise Institute,And Market Research On Employer H‑1B Activity.

Okay, here’s a breakdown of the provided text, summarizing the key data and organizing it for clarity. I’ll focus on the core changes, implications, and advice.

FHA Rule Shuts Down Mortgage Lock Surge for Non-Permanent Residents

What the New FHA Rule Entails

Effective Date: January 1 2025

- The Federal Housing Administration (FHA) updated HUD‑FHA 1020.1 to restrict rate‑lock extensions for borrowers who are not U.S. permanent residents.

- Primary change: Mortgage locks that exceed a 45‑day period must be re‑evaluated and can be canceled if the borrower’s residency status remains non‑permanent at lock expiration.

- Goal: Reduce credit‑risk exposure for the FHA’s Mutual Mortgage Insurance Fund while aligning loan eligibility with HUD’s “non‑citizen borrower” policy.

Key terminology

| Term | Definition |

|---|---|

| Mortgage lock | A lender’s promise to hold a specific interest rate for a set period, typically 30-60 days. |

| Non‑permanent resident | Visa holders (e.g.,H‑1B,L‑1,F‑1,J‑1) without a green card or naturalization status. |

| FHA loan eligibility | Criteria set by HUD that determine who may qualify for federally insured mortgages. |

Impact on Mortgage rate Locks

1. Lock‑Duration Limits

- Standard lock: 30 days (no change).

- extended lock: 45 days allowed only if the borrower can provide proof of permanent residency before lock initiation.

2. Re‑underwriting Requirement

- At the 45‑day mark, lenders must submit an updated Residency Verification Form (HUD‑1020‑R).

- Failure to verify permanent status automatically terminates the lock, forcing borrowers to re‑lock at current market rates.

3. Lender Compliance Checklist

- Identify borrower’s immigration status during loan application.

- Flag non‑permanent residents in the loan origination system (LOS).

- Set automated alerts for the 30‑day and 45‑day lock milestones.

- Gather supporting documents (green card, naturalization certificate, or USCIS receipt) before the 45‑day deadline.

- Submit HUD‑1020‑R for approval; if denied, notify borrower of lock cancellation.

Eligibility Changes for Non‑Permanent Residents

| Category | Previous FHA Policy | New FHA Rule (2025) |

|---|---|---|

| Green‑Card Holders | Eligible for full lock periods | No change; can lock up to 60 days. |

| Visa Holders (H‑1B, L‑1, O‑1, etc.) | Eligible for standard 30‑day lock | Must lock ≤ 30 days; any extension requires permanent residency proof. |

| Students (F‑1, J‑1) | Allowed 30‑day lock, but higher documentation | Same lock limit; additional proof of future residency intent required for any extension. |

| Undocumented Applicants | Not eligible for FHA loans | Still ineligible; rule reinforces existing restriction. |

Practical implication

- Non‑permanent residents will experience higher rate‑swap risk because they cannot secure long‑term locks during volatile market periods.

- Mortgage brokers may need to adjust pricing models to reflect the increased uncertainty.

Practical Tips for Prospective Borrowers

- Start the loan process early: Initiate pre‑approval at least 45 days before closing to avoid lock expiration.

- Secure permanent residency documentation: If you have a green‑card application pending, request an I‑485 receipt and submit it promptly.

- consider a “lock‑and‑sell” strategy: Lock at 30 days, then sell the lock to a secondary market (e.g., lock‑swap platforms) if a longer lock is required.

- Work with FHA‑approved lenders: They are more familiar with HUD‑1020‑R filing and can provide fast‑track verification.

- Monitor market trends: Use real‑time rate trackers (e.g., Freddie Mac’s Primary Mortgage Market Survey) to time your lock strategically.

Case Study: Real‑World Example (2025 Q2)

- Borrower: Maria González, H‑1B visa holder, purchasing a condo in Austin, TX.

- Scenario: Requested a 60‑day lock on a 3.75% rate. Under the new rule, the lender flagged the request, limited the lock to 30 days, and advised Maria to submit her green‑card receipt.

- Outcome: Maria received her green‑card within 40 days, filed HUD‑1020‑R, and secured a 45‑day extension at the original rate. The loan closed on schedule, saving an estimated $3,200 in interest‑rate risk.

Benefits and Drawbacks of the New Rule

Benefits

- Reduced insurer exposure: Limits potential loss to the FHA’s Mutual Mortgage Insurance Fund.

- Clearer risk profile: Lenders can more accurately price loans for non‑permanent residents.

- Encourages residency transition: Incentivizes borrowers to pursue permanent status for more favorable loan terms.

Drawbacks

- Higher cost of borrowing: Shorter lock windows may force borrowers into higher rates if markets rise.

- Administrative burden: Additional documentation and LOS alerts increase overhead for lenders.

- Potential market slowdown: non‑permanent resident homebuyers represent ~12 % of the FHA loan pool; tighter restrictions could temper demand.

Guidance for Lenders and Mortgage Professionals

- Update LOS workflows to automatically flag non‑permanent residency status.

- Train underwriting staff on the new HUD‑1020‑R submission timeline.

- Communicate transparently with borrowers about lock limitations during the application interview.

- Partner with immigration attorneys to assist borrowers in accelerating green‑card processing where feasible.

- Track policy compliance using monthly audits; non‑compliance may trigger HUD penalties.

Frequently Asked Questions (FAQ)

Q1: Can a non‑permanent resident still obtain an FHA loan?

A1: Yes, but the borrower is limited to a 30‑day rate lock unless permanent residency is proven before the 45‑day threshold.

Q2: What documentation satisfies the “permanent residency” requirement?

A2: A valid green card, naturalization certificate, or an I‑485 receipt indicating a pending green‑card application accepted by HUD.

Q3: Does the rule affect VA or USDA loans?

A3: No, the rule applies solely to FHA‑insured mortgages. VA and USDA programs maintain their own residency criteria.

Q4: How does this affect refinancing for non‑permanent residents?

A4: Refinances are subject to the same lock limits; however, many lenders allow rate‑float options to mitigate short‑term volatility.

Q5: Are there any state‑specific exceptions?

A5: Some states (e.g., California) have supplementary programs that offer state‑backed mortgage insurance with more flexible lock periods, but FHA rules remain the baseline.

Keywords integrated: FHA rule, mortgage lock, non-permanent residents, FHA loan eligibility, HUD‑1020‑R, rate‑lock extension, permanent residency proof, mortgage underwriting, FHA‑insured mortgage, non‑citizen homebuyer, real estate market impact, mortgage financing, rate‑swap risk, green card, immigration status, loan origination system.