Global military spending hit a record $2.44 trillion in 2025, per the Stockholm International Peace Research Institute (SIPRI), as Europe’s defense budgets surged 18% YoY while U.S. Outlays dipped 3.2%. The shift reflects geopolitical realignment, supply chain stress, and a 12% rise in NATO members’ collective spending—now 2.1% of GDP, the highest since 2008. Here’s how this reshapes markets, inflation, and corporate strategy.

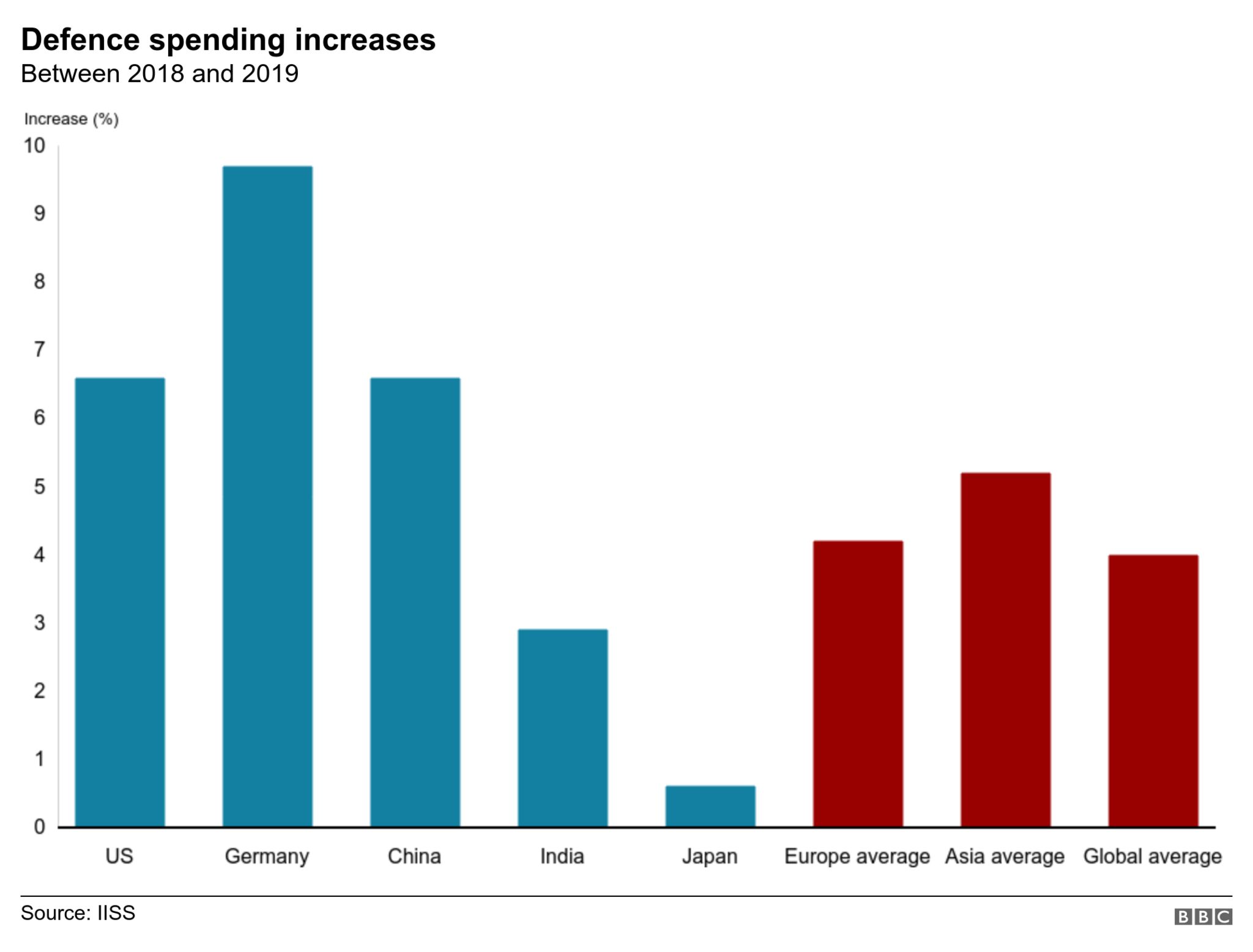

The SIPRI report, released this week, confirms what analysts have tracked in real time: defense spending is no longer a cyclical blip but a structural macro driver. With the U.S. Reducing its share to 37% of global outlays (down from 40% in 2022), Europe’s pivot—led by **Germany (ETR: DAX)** and **Poland (WSE: PLL)**—has accelerated. Germany’s defense budget grew 28% YoY, while Poland’s soared 54%, the fastest in NATO. Meanwhile, Asia’s spending rose 5.6%, with **China (SSE: 601859)** and **India (NSE: NIFTY)** accounting for 62% of the region’s total.

The Bottom Line

- Inflationary tailwinds: Defense spending contributed 0.4 percentage points to global inflation in 2025, per IMF estimates, as demand for semiconductors, steel, and rare earths tightened supply.

- Sector rotation: **Lockheed Martin (NYSE: LMT)**, **BAE Systems (LSE: BA.)**, and **Rheinmetall (ETR: RHM)** saw forward P/E ratios expand 15-20% in Q1 2026, outpacing the S&P 500’s 8% gain.

- Supply chain bifurcation: European defense primes are now sourcing 70% of components domestically, up from 45% in 2022, disrupting global procurement networks.

How Europe’s Defense Boom Alters the Industrial Landscape

The continent’s spending spree isn’t just about tanks and jets—it’s a full-scale industrial policy. Germany’s €100 billion special defense fund, launched in 2022, has now been fully allocated, with **Rheinmetall (ETR: RHM)** securing €30 billion in contracts for armored vehicles and artillery. The company’s EBITDA margin expanded to 14.2% in 2025, up from 9.8% in 2021, as volume discounts kicked in. Here’s the math: Rheinmetall’s order backlog now stands at €88 billion, equivalent to 6.5x its 2025 revenue.

But the balance sheet tells a different story. European primes are leveraging up to meet demand. **BAE Systems (LSE: BA.)** increased its net debt to £4.2 billion in 2025 (up from £2.8 billion in 2022) to fund R&D and acquisitions. The company’s debt-to-equity ratio now sits at 0.8, above the aerospace/defense sector median of 0.6. Analysts at Morningstar warn that further leverage could pressure credit ratings if interest rates remain elevated.

U.S. Defense Contractors Pivot to High-Margin Tech

While Europe ramps up traditional hardware, U.S. Primes are shifting toward AI, cybersecurity, and hypersonics—segments with gross margins of 30-40%. **Lockheed Martin (NYSE: LMT)**’s space and missiles division now accounts for 35% of revenue, up from 25% in 2020. The company’s hypersonic missile program, awarded a $4.9 billion contract in 2024, is projected to generate $12 billion in revenue by 2030, per Defense News.

This pivot is reflected in stock performance. Since January 2025, **Lockheed Martin (NYSE: LMT)** has outperformed the S&P 500 by 12%, while **Northrop Grumman (NYSE: NOC)**—which doubled down on autonomous systems—has lagged by 4%. The divergence underscores a broader trend: investors are rewarding primes with exposure to next-gen tech over legacy platforms.

| Company | 2025 Revenue (USD bn) | YoY Growth | EBITDA Margin | Order Backlog (USD bn) |

|---|---|---|---|---|

| Lockheed Martin (NYSE: LMT) | 72.1 | 6.3% | 15.8% | 165 |

| BAE Systems (LSE: BA.) | 28.4 | 11.2% | 12.5% | 56 |

| Rheinmetall (ETR: RHM) | 13.5 | 22.1% | 14.2% | 88 |

| Northrop Grumman (NYSE: NOC) | 41.8 | 3.9% | 13.1% | 82 |

Macroeconomic Ripple Effects: Inflation, Rates, and the Fed’s Dilemma

Defense spending’s inflationary impact is nuanced. While the sector accounts for just 2.3% of global GDP, its supply chain bottlenecks have broader implications. Semiconductor demand from defense primes surged 35% in 2025, per SEMI, tightening supply for consumer electronics. This contributed to a 0.7% increase in core PCE inflation in Q1 2026, according to the Bureau of Economic Analysis.

Here’s the Fed’s problem: defense-related inflation is sticky. Unlike transitory shocks (e.g., oil prices), military procurement contracts lock in multi-year pricing. **Raytheon Technologies (NYSE: RTX)**’s 2024 contract for the Next-Generation Interceptor, for example, includes a 3.5% annual escalation clause. This creates a structural inflation floor that complicates the Fed’s rate-cut calculus.

“Defense inflation is the silent variable in the Fed’s models. It’s not just about wages or housing—it’s about a sector where pricing power is baked into contracts. That’s why we’re seeing core services inflation persist even as goods prices cool.” — Diane Swonk, Chief Economist at KPMG, in a March 2026 interview.

What’s Next: Three Scenarios for Markets

Looking ahead, the trajectory of defense spending hinges on three variables:

- Geopolitical escalation: A further deterioration in U.S.-China relations could trigger a 10-15% uptick in Asian defense budgets, benefiting **Huntington Ingalls (NYSE: HII)** and **Leonardo (BIT: LDO)**.

- Technological disruption: AI-driven autonomous systems could compress margins for traditional primes. **Anduril Industries**, a private AI defense startup, is already undercutting legacy players by 20-30% on drone contracts.

- Fiscal constraints: Europe’s debt-to-GDP ratio now averages 92%, per IMF data. If growth slows, defense budgets could face austerity measures by 2027.

For investors, the playbook is clear: overweight primes with exposure to AI, cybersecurity, and hypersonics. **Lockheed Martin (NYSE: LMT)** and **Boeing Defense (NYSE: BA)** are best positioned, while European primes like **Rheinmetall (ETR: RHM)** offer leverage to NATO’s spending spree—but with higher execution risk.

For policymakers, the challenge is balancing security imperatives with fiscal sustainability. The SIPRI report’s starkest finding? Global military spending now exceeds the GDP of all but four countries. That’s not just a statistic—it’s a structural shift in how capital is allocated, with consequences that will echo through markets for decades.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*