{kind=link}

ACA Marketplace Competition is Surging – And It Could Reshape American Healthcare

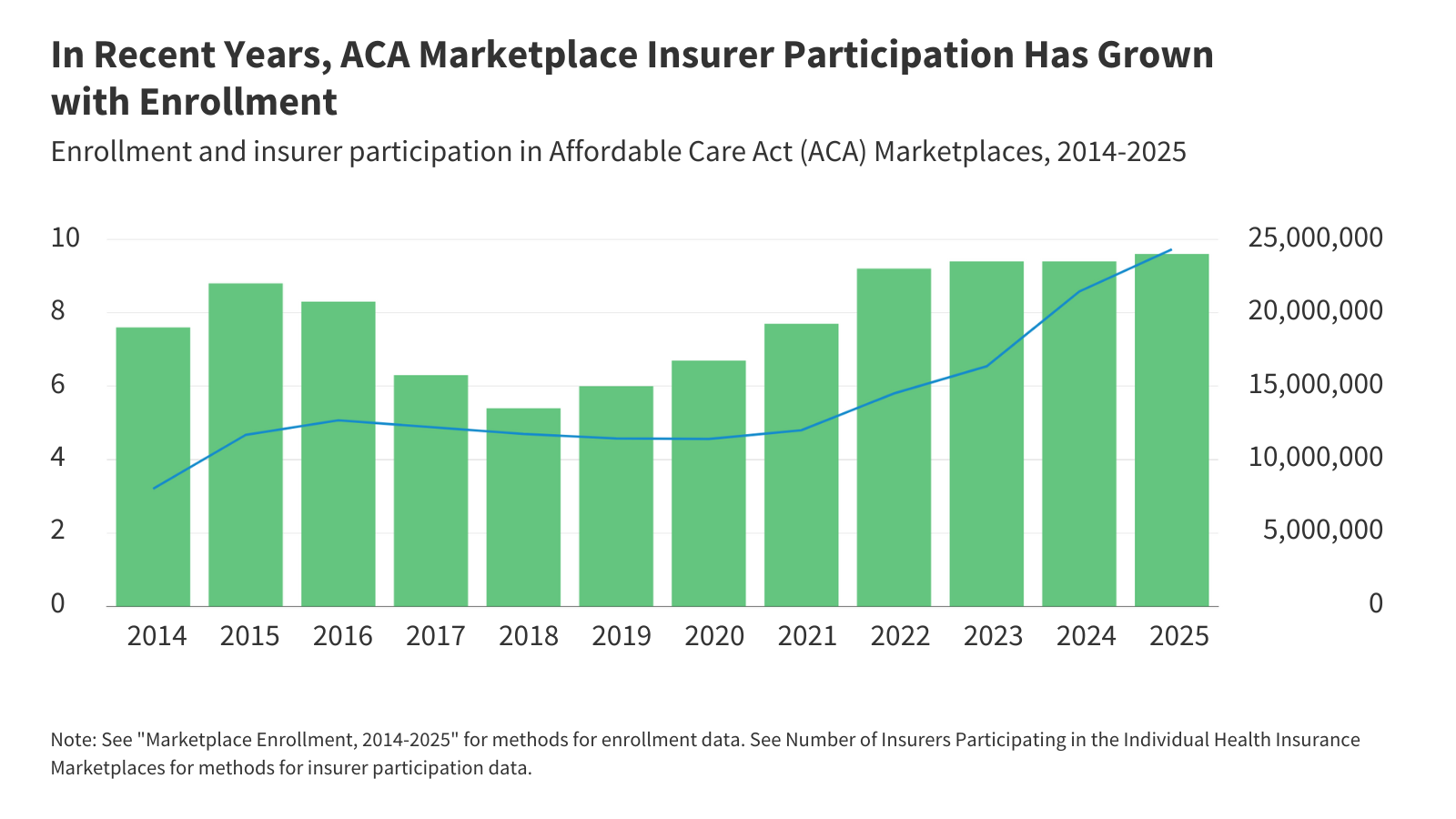

A surprising shift is underway in the U.S. health insurance landscape: while the overall market remains dominated by a few giants, competition within the Affordable Care Act (ACA) Marketplaces is increasing. New data reveals the average market share of the largest insurer in each state’s individual market dropped from 60% to 53% between 2020 and 2023, directly correlating with the expanded premium tax credits introduced in 2021. This isn’t just a statistical blip; it signals a potential turning point in access and affordability, and a future where consumers have more choices.

The Rise of Competition in the Individual Market

For years, the ACA Marketplaces faced criticism for limited insurer participation in many states. But the enhanced premium tax credits – made more generous by the American Rescue Plan – dramatically altered the equation. These credits lowered costs for millions, attracting new enrollees and, crucially, incentivizing more insurance companies to enter the market. The Peterson-KFF Health System Tracker’s recent analysis confirms this trend, showing enrollment growth and a corresponding decline in market concentration. This increased competition isn’t just about more names on a list; it’s about insurers vying for customers through better plans, lower premiums, and improved services.

What’s Driving the Change?

The enhanced premium tax credits are the primary catalyst. By making coverage more affordable, they expanded the potential customer base for insurers. This, in turn, reduced the risk associated with participating in the Marketplaces, encouraging both established players and new entrants. Furthermore, the stability provided by these credits has allowed insurers to plan for the future with greater certainty, fostering a more sustainable competitive environment. This is a stark contrast to the earlier years of the ACA, when uncertainty about the law’s future deterred some insurers.

Employer-Sponsored Insurance: A Different Story

While the individual market is becoming more competitive, the opposite is happening with fully insured employer-sponsored health insurance. Over the past decade, these markets have become less competitive, with fewer insurers offering plans. This consolidation gives employers less leverage in negotiating premiums, potentially leading to higher healthcare costs for both businesses and employees. The reasons for this divergence are complex, but likely include economies of scale, increasing administrative burdens, and the negotiating power of large hospital systems.

The Implications of Concentrated Employer Markets

Reduced competition in employer-sponsored insurance isn’t just a financial issue. It can also limit innovation and choice. When employers have fewer insurers to choose from, they may be forced to accept plans with limited networks or restrictive coverage. This can lead to higher out-of-pocket costs for employees and difficulty accessing the care they need. The trend highlights a growing disparity in the healthcare experience depending on how someone obtains their coverage.

Looking Ahead: Will the Trend Continue?

The future of health insurance competition hinges on several factors. The most critical is the fate of the enhanced premium tax credits. Currently, they are set to expire at the end of 2025. If Congress fails to extend them, enrollment in the ACA Marketplaces is likely to decline, and competition could erode. However, the success of the Marketplaces over the past few years has demonstrated their potential to provide affordable coverage and foster competition. Another key factor is the role of state-based Marketplaces. States that have established their own Marketplaces often have more robust competition and lower premiums than those that rely on the federal Marketplace.

Furthermore, we may see increased consolidation among insurers overall, driven by mergers and acquisitions. This could offset some of the gains in competition within the ACA Marketplaces. The ongoing debate over healthcare reform and the potential for new regulations will also play a significant role. Ultimately, the direction of the health insurance market will depend on the choices policymakers make in the coming years.

The resurgence of competition in the ACA Marketplaces is a positive development, offering a glimpse of a more affordable and consumer-friendly healthcare system. But sustaining this momentum requires proactive policies and a commitment to ensuring that all Americans have access to quality, affordable health insurance. What steps should policymakers take to ensure continued competition and affordability in the individual health insurance market? Share your thoughts in the comments below!