2024-04-09 12:52:05

Learn how to declare your assets invested in Warren in Income Tax 2024

In 2024, you have until May 31st to submit your declaration to the Revenue.

In this article, we detail everything you need to know about declaration of your investments in Warren.

Follow along!

How to find the Income Statement at Warren

The first step to declaring your investments in Warren is to generate the Income Report.

The Warren Income Report can be found through the logged in area accessed via app or browser.

Just do the following: Menuclick in My Investments. Then in Report income. If access is via an app, the path is the same, you will need to scroll down and find the “My Investments” menu, then click on “Statements and Reports” to then find the “Income Report” part.

Declaring portfolio investment funds

Some Warren investment portfolios include products such as investment funds.

Each product included in the portfolios must be declared individually in the declaration, in accordance with the specifications contained in the Income Report.

We will see the details of each product below, starting with the investment funds.

Firstly, it is necessary to understand that investment funds must be declared in two moments in your Income Tax declaration.

O balance relating to each investment fund must be entered as “Assets and rights”, within the “Assets and Debts” tab (found in the menu on the left).

Income from applications must be entered as “Exclusive Tax Income”, within the Income tab.

Therefore, each investment fund will appear twice in your declaration. First, to declare that you own them. Then, to declare the respective income.

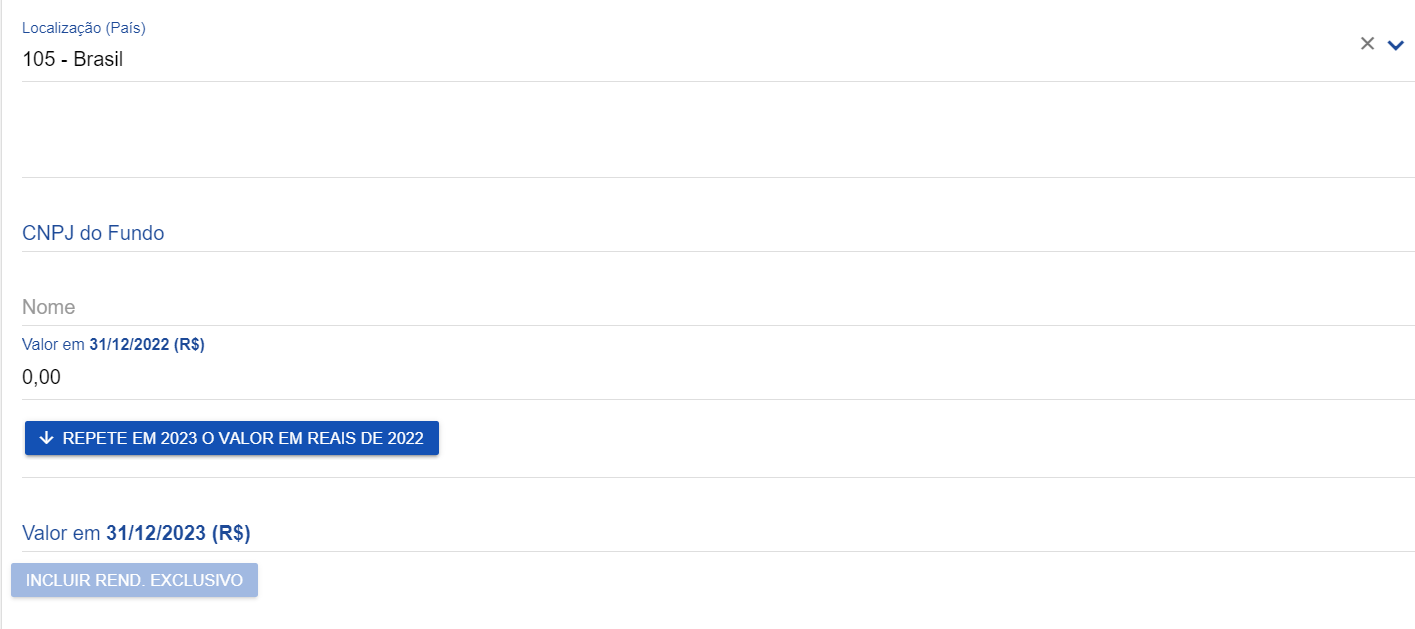

In the Assets and Debts tab

Starting with the tab Assets and Debtseach fund will be declared according to its specific code – first, you must select the code 07 – Funds.

Check your income report that you obtained from Warren for the name, CNPJ and code of each fund in your portfolio.

After the code and CNPJ of the investment fund, you need to specify the operation, in the “Discrimination”.

There, gather the information you have about the investment, detailing the fund name it’s yes institution that distributes it.

In the field below, which asks for the situation on 12/31/2022 and 12/31/2023, enter the amount you had invested in the fund on each date (the information appears in the Income Report).

If you invested for the first time in 2023, the field for 2022 will be reset to zero.

And the Renditions

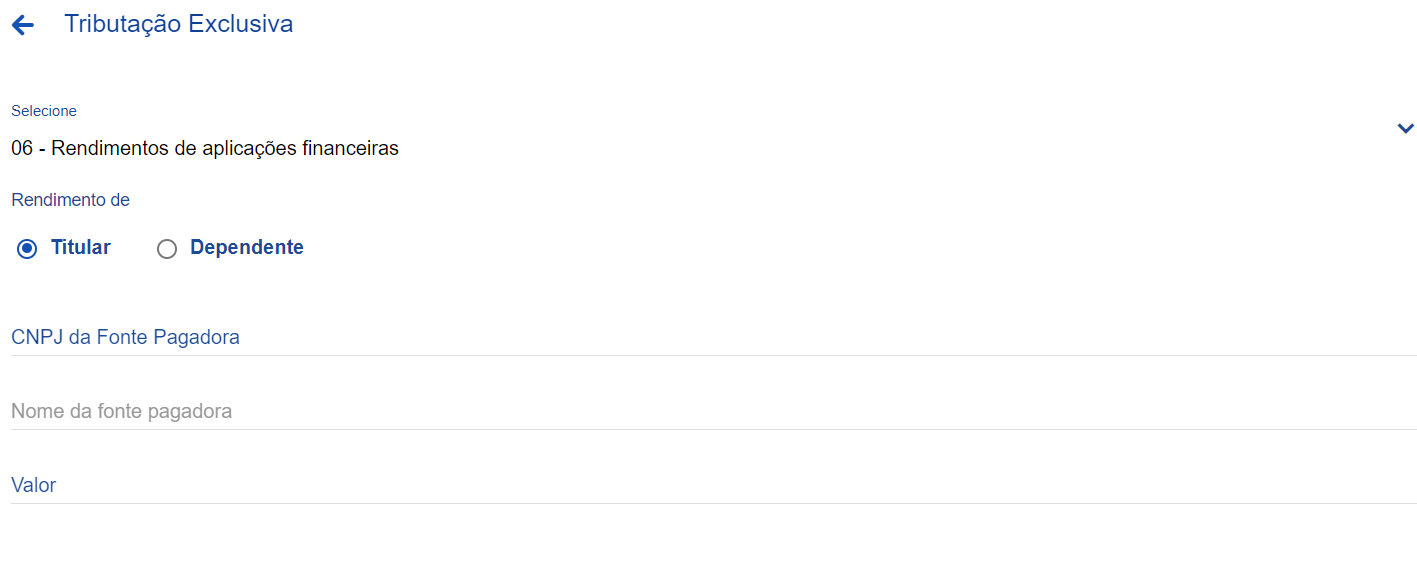

Now that you have declared the balance you had in the funds, you need to declare the income earned, as shown in the Income Report.

To do this, access the tab Income, and then add the type of income “Exclusive Taxation”. Then select the line “06 – Income from financial investments”.

Filling in is simple:

- Type of beneficiary: must not be modified unless you are not the owner;

- CNPJ of the paying source: it is the CNPJ of the person making the payment, in this case, the CNPJ of each of your funds (check your income report);

- Name of paying source: following the same logic as the CNPJ, you must provide the name of the paying source;

- Valor: the amount obtained in 2023, according to the Income Report.

Declaring Fixed Income

Treasury, CDB’s and Common Debentures

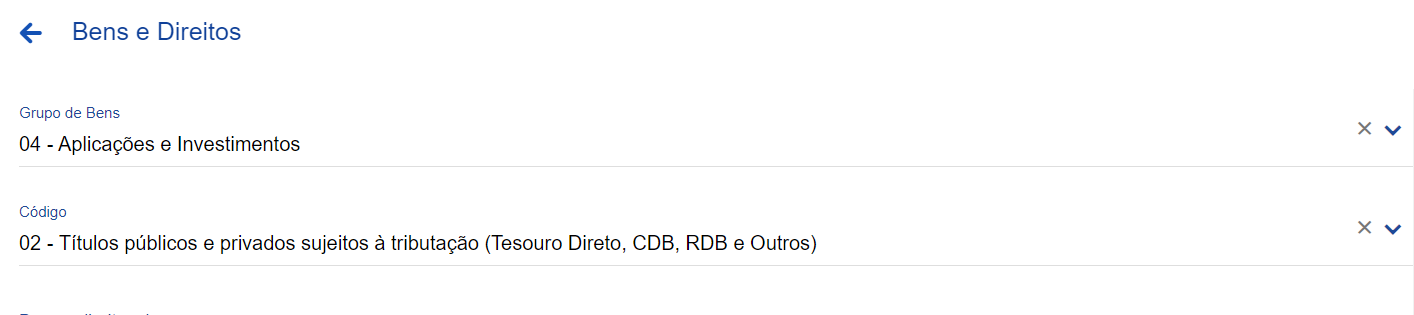

To declare Treasury bonds and CDBs, access the tab “Assets and Debts”patch me “Assets and rights”select the Group “04 – Applications and Investments” and use the code “02 – Public and private securities subject to taxation (Tesouro Direto, CDB, RDB and others)”.

Fill in the values for each title on 12/31/2022 and 12/31/2023. In the breakdown part, inform the name of the security and the financial institution where it is applied.

NOTE: If the title was acquired in 2023, leave the 12/31/2022 field blank. If you sold the paper last year, leave the 12/31/2023 field blank.

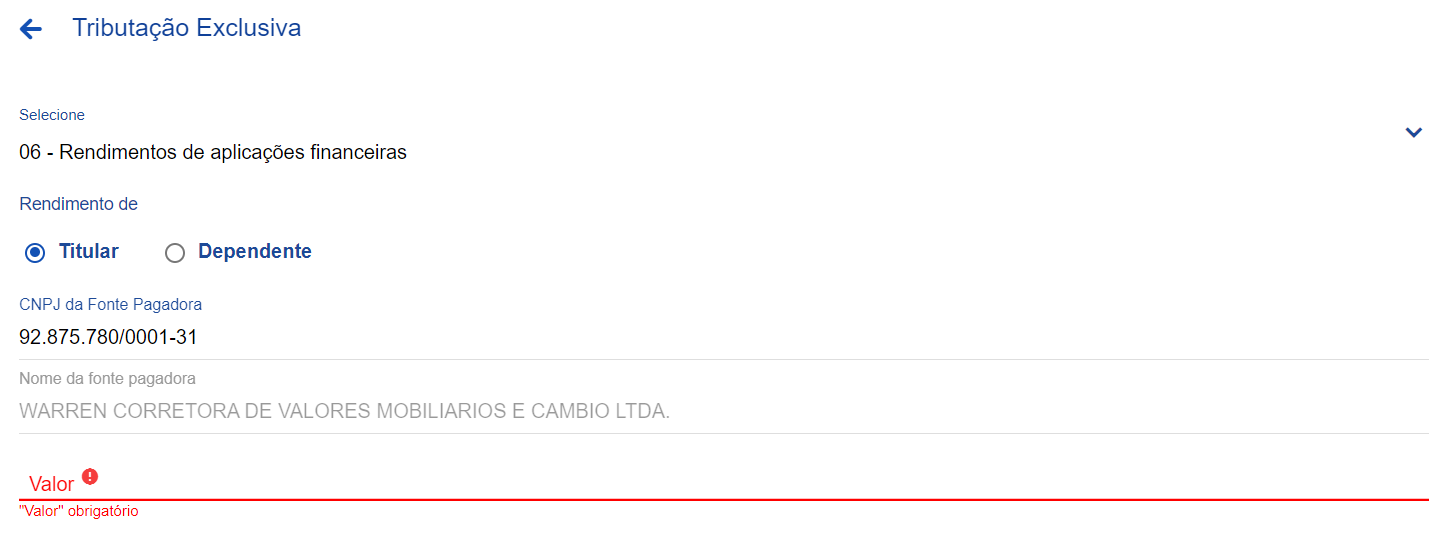

Next, it’s time to declare your income. In the tab “Income”go to the section “Exclusive Taxation” and access the item “06 – Income on financial investments”.

Enter the CNPJ of the paying source, in this case the Warren Securities and Exchange Brokerage (CNPJ:92.875.780/0001-31)and the value of the income indicated in the Income Report.

Securities exempt from IR

Applications in CRI’s, CRA’s, LCI’s, LCA’s and Incentive Debentures are exempt from Income Tax. Therefore, you must follow the following steps:

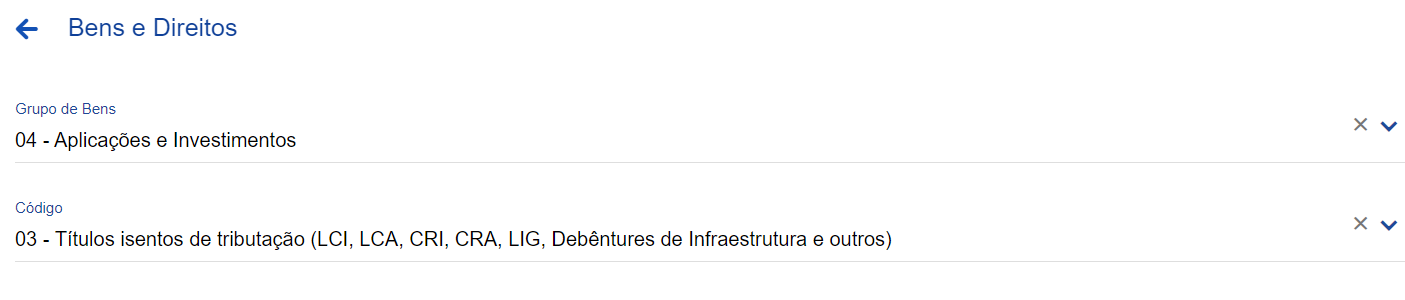

In the Assets and Debts tab

Patch me “Assets and rights”select the Group “04 – Applications and Investments” and use the code “03 – Tax-exempt securities (LCI, LCA, CRI, CRA, LIG, Infrastructure debentures and others).

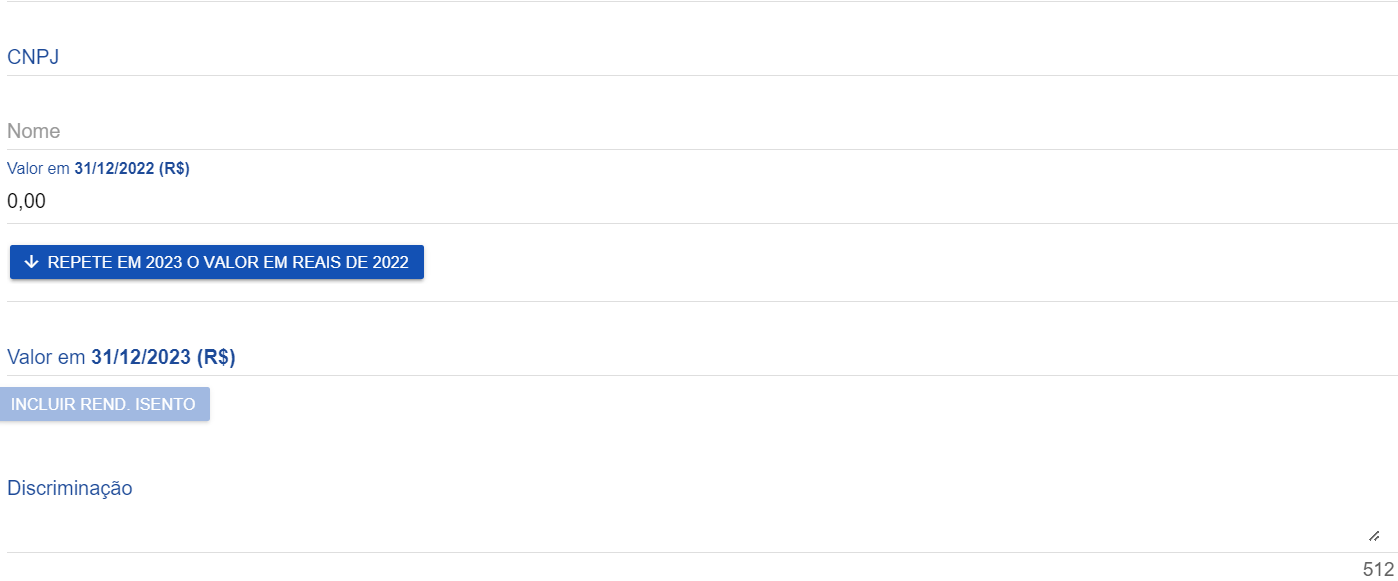

Fill in the values for each title on 12/31/2022 and 12/31/2023. In the breakdown part, inform the name of the security and the financial institution where it is applied.

And the Renditions

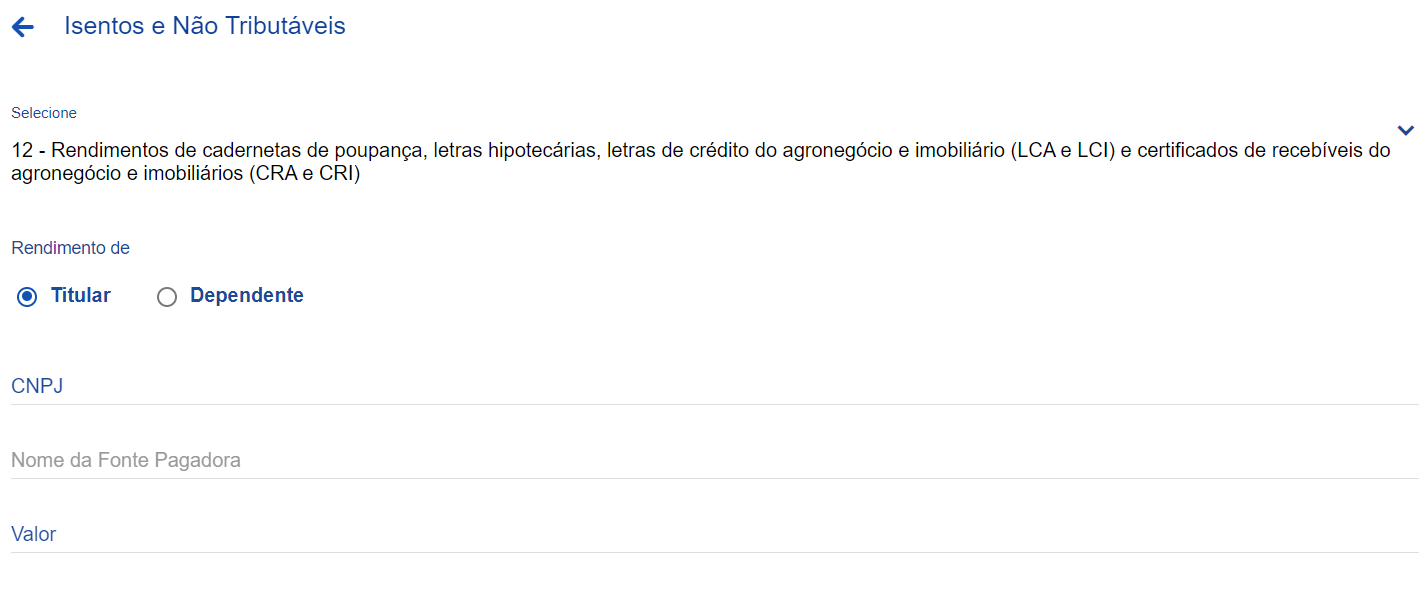

Go to the “Exempt and Non-Taxable” section and access the item “12 – Income from savings, mortgage bills, agribusiness and real estate credit bills (LCI and LCA) and agribusiness and real estate receivables certificates (CRA and CRI)”.

Enter the CNPJ of the paying source, in this case Warren Corretora de Valores Mobiliários e Câmbio (CNPJ:92.875.780/0001-31), and the value of the income indicated in the Income Report.

Declaring the assets of your Stock tab

Through the Stock Exchange tab, Warren clients can buy and sell securities traded on the Stock Exchange. Investors in managed portfolios of our shares must also declare each of the assets that comprise it.

It is important to remember that assets such as Shares, BDRs, ETFs and FIIs It is the administrators’ responsibility to send you information related to quantity, average price and values.

Again, it all starts with the Income Report, which is sent to investors by administrators.

Assets and Debts Tab

In the item Goods and Rights, again:

- To declare shares, use item “3 – Corporate Interests” and then code 01 – Shares (including those listed on the stock exchange).

- To declare BDRs, choose the item “4 – Applications and Investments”, and then 04 – Assets traded on exchanges in Brazil”.

- To declare FIIs, choose the item “7 – Funds” and then “3 – Real Estate Investment Fund (FII)”.

- To declare ETFs, choose the item “7 – Funds” and then “9 – Other Market Index Funds (ETFs).

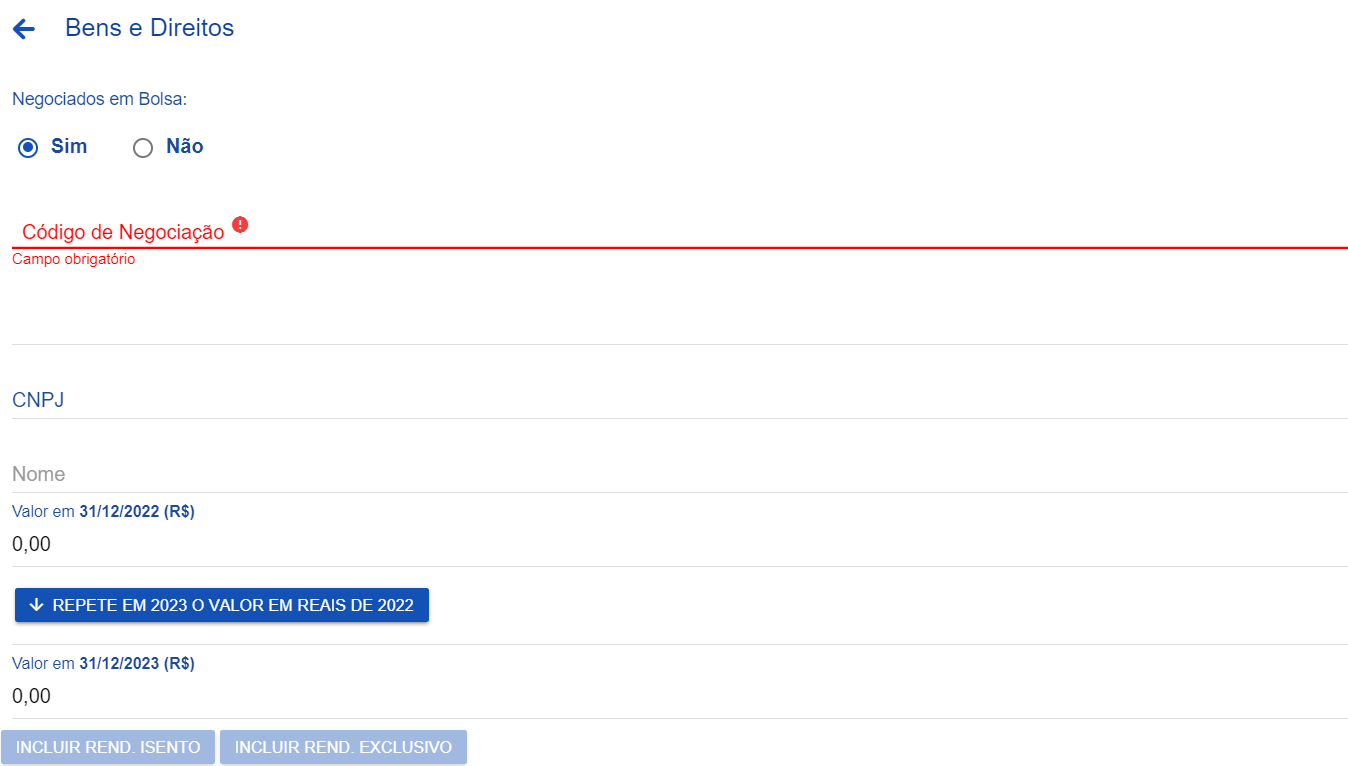

Enter the CNPJ of the company you are investing in. In the breakdown, you must enter the number of shares for this specific share.

- Example: 100 Petrobras shares (PETR4), with an average price of XX R$. The average price is the average of the total value you paid for the company’s shares. This process also applies to shares of FIIs, ETFs and BDRs.

- In the trading code field, you must enter the share/quota code. In the previous example, it would be PETR4.

- In the “Status” field, on 12/31/2022 and on 12/31/2023, you must inform the acquisition value of the shares, regardless of the day of the year you purchased them;

- If the purchase was made in 2023, the 12/31/2022 field is cleared;

- If the sale of all shares was made in 2023 and now the investor no longer has the share in their portfolio, the 12/31/23 field must be cleared – and in the description, the details of the sale must be included;

Note that you will not mention the current value of the shares here, but rather the value that paid for the purchase. This information can be consulted through the average price reported in B3’s CEI system.

After all, by multiplying the average price by the total number of shares you have, you can know the total amount invested.

It is not necessary to specify the broker through which you purchased the products.

And aba yields

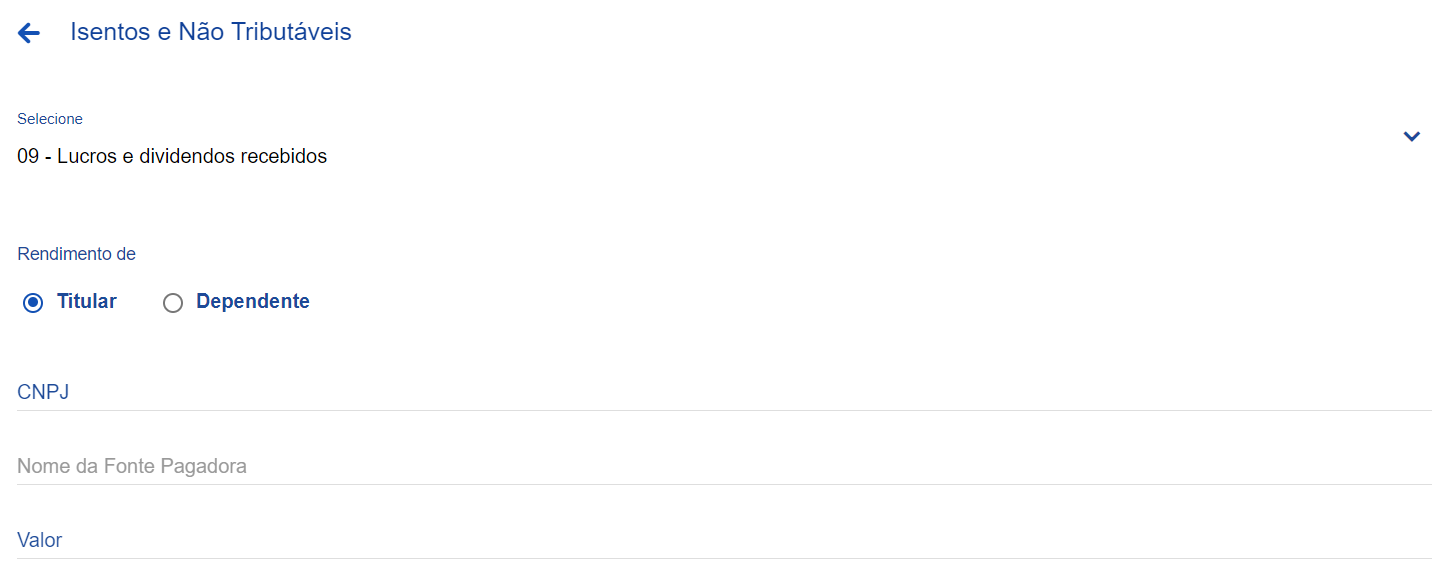

Dividends received must be declared in the tab Income, in the Exempt and Non-Taxable itemselecting the option “09 – Profits and dividends received”, as stated in the Income Report.

Fill in the CNPJ of the company that paid the dividends, the name of the company and the amount of dividends received in the year. You must do the process for each different share you have.

Interest on Equity (JCP) must be declared in the Income tab, in the Subject to Exclusive Taxation item, with the option “10 – Interest on equity”. Do the same filling process as before.

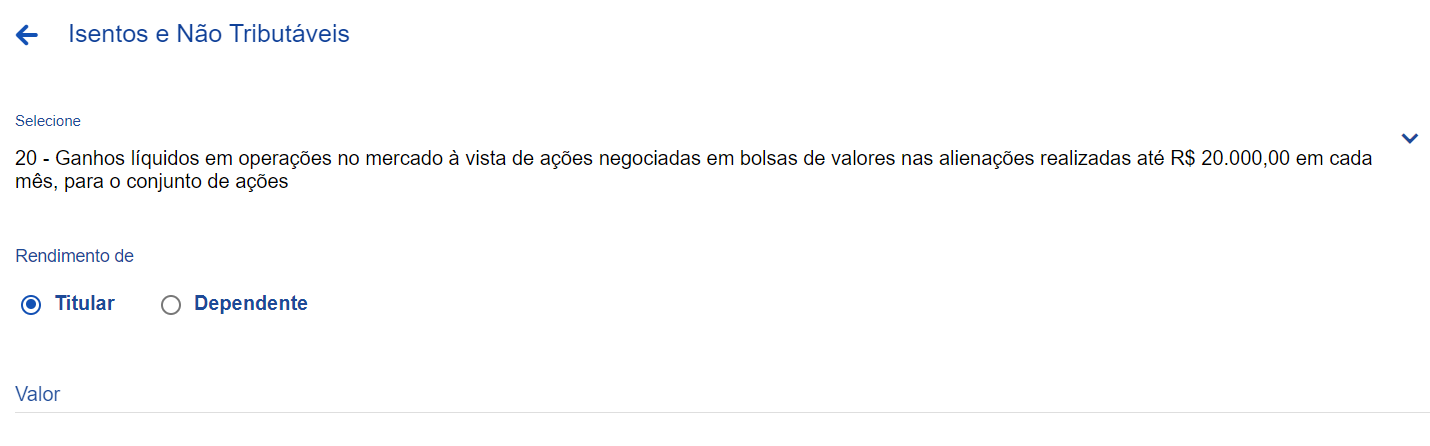

If you sold up to R$20,000 in shares per month

In these cases, the investor is exempt from tax, but must declare the gains under the “Exempt and Non-Taxable” item, with the code 20 – Net gains from operations in the spot market of shares traded on stock exchanges on disposals carried out up to R$20,000.

It is important to highlight that this limit value of R$20,000 refers to the total value of sales in the month, and not a specific action. So, if you sold in the same month, for example, R$15 thousand of one share and another R$10 thousand of another, the total value exceeds this limit and these gains must be declared in the step-by-step guide below.

Fill in how much you earned during the year when selling shares.

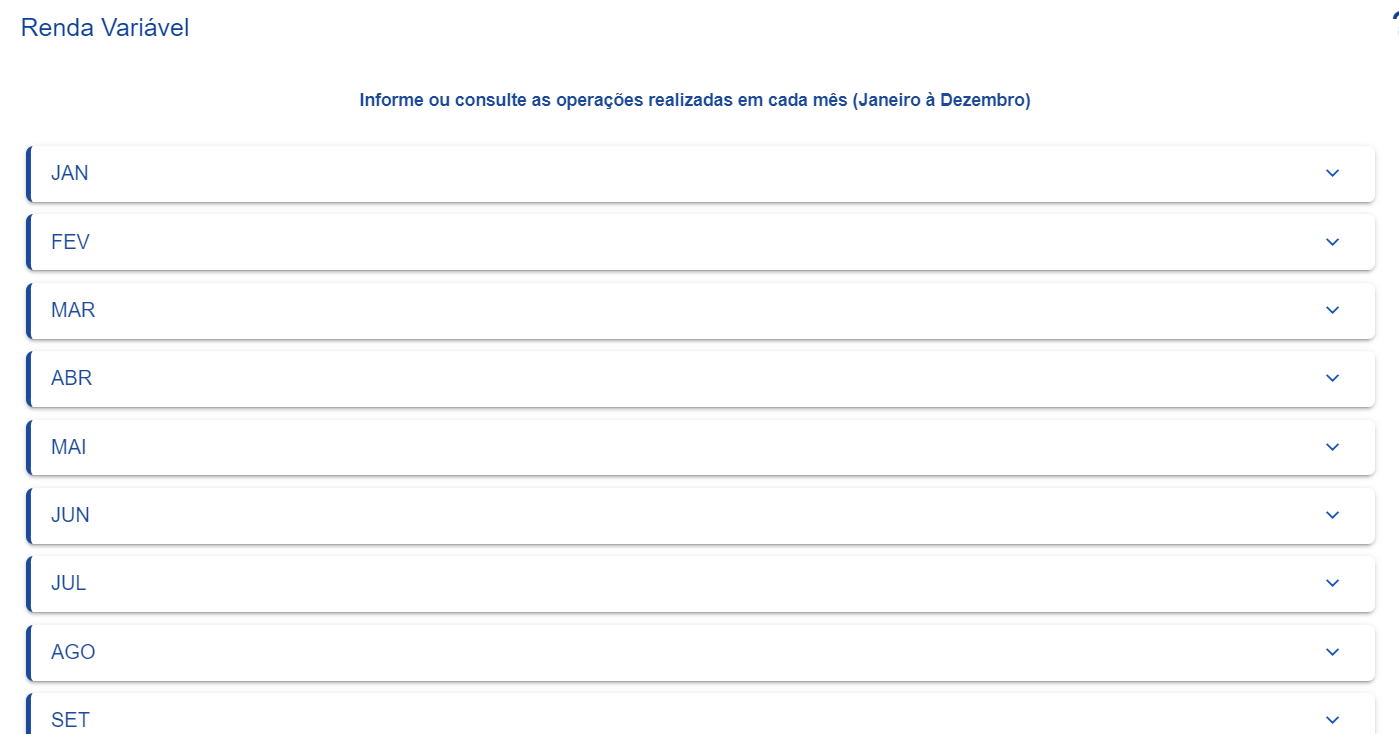

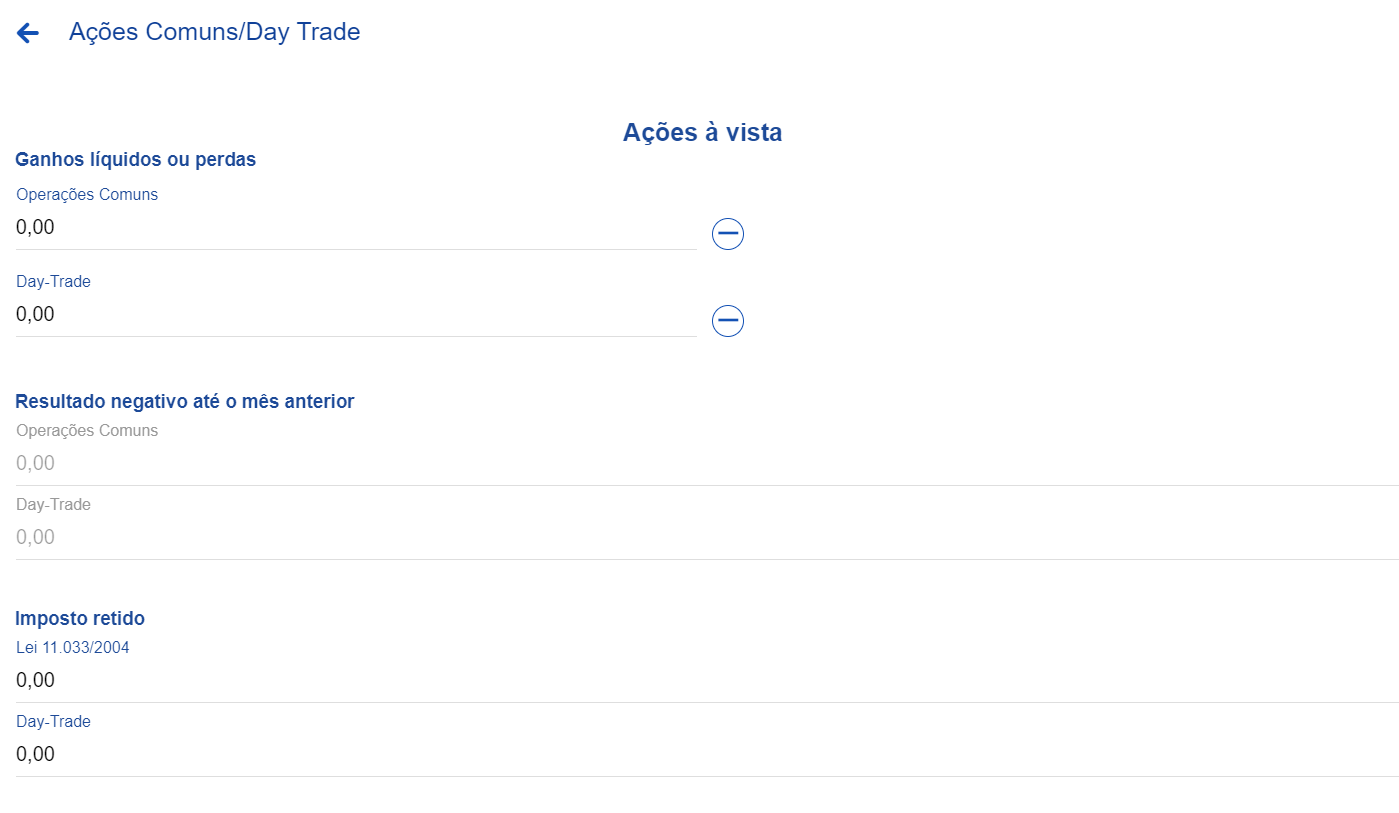

If you sold more than R$20,000 in a few months

Access the variable income tab and fill in the profits obtained month by month. Use the Darf you paid for to fill in this information. At the end, under “tax paid”, you must fill in the total amount you paid in Darf that month.

Click on the month referring to the sale and fill in.

Enter a value equal to zero in the months in which you have not carried out operations and also in those in which share sales totaled less than R$20 thousand (these are included in the “Exempt and Non-Taxable” item).

READ MORE

1713000217

#declare #investments #Income #Tax