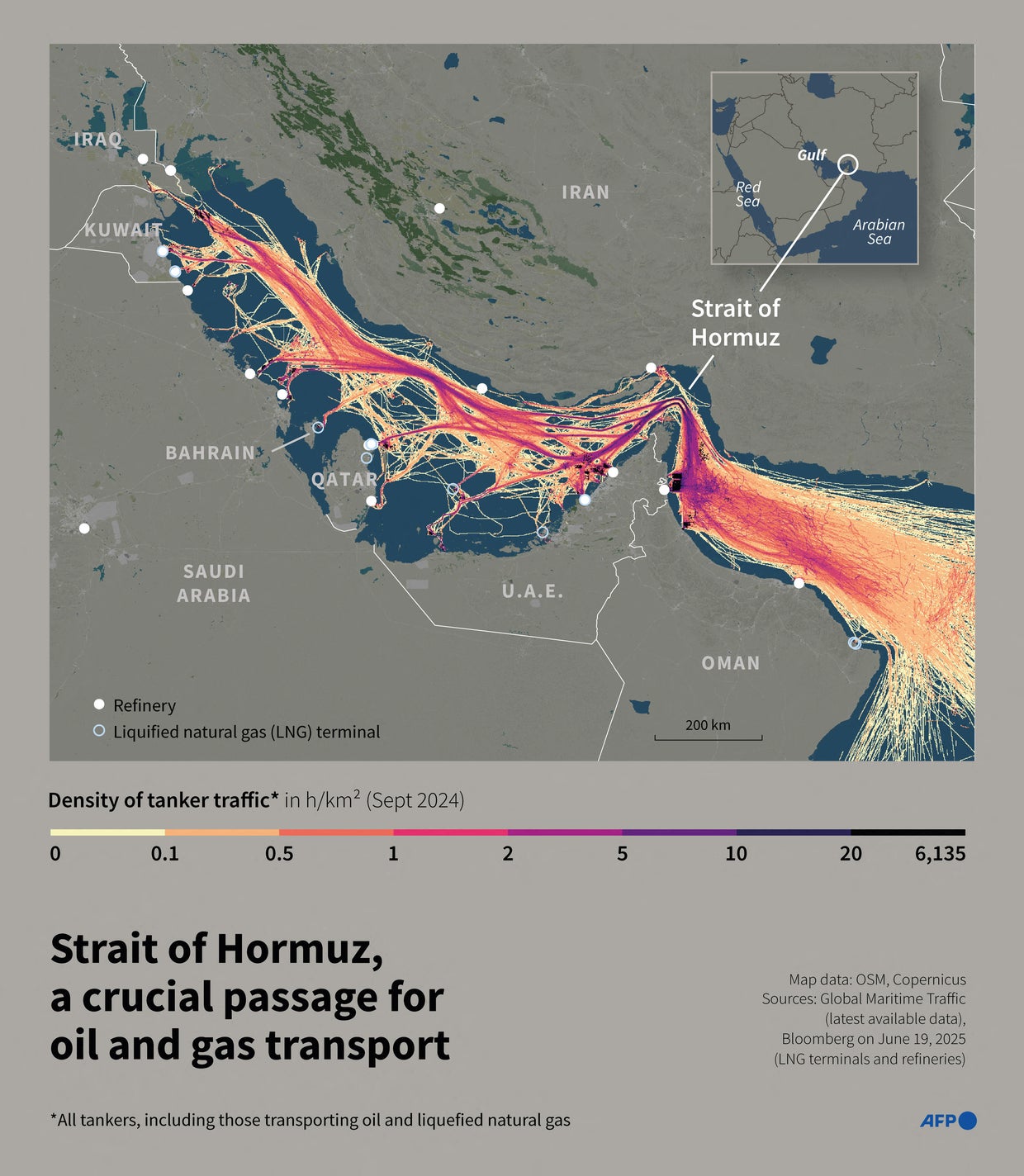

Diplomatic failure in the Strait of Hormuz has triggered a total blockade, threatening approximately 20% of global oil supplies. This energy asphyxiation disrupts international trade, spikes Brent Crude futures, and forces immediate strategic pivots for global energy firms and central banks to mitigate systemic inflationary shocks across G20 economies.

The collapse of negotiations in the Strait of Hormuz is not merely a geopolitical crisis. it is a fundamental supply-side shock that invalidates the 2026 inflation forecasts of most major central banks. When a primary artery for global energy is severed, the resulting volatility isn’t limited to oil prices—it ripples through the cost of plastics, fertilizers, and transport, creating a cost-push inflation cycle that is notoriously difficult for monetary policy to resolve.

The Bottom Line

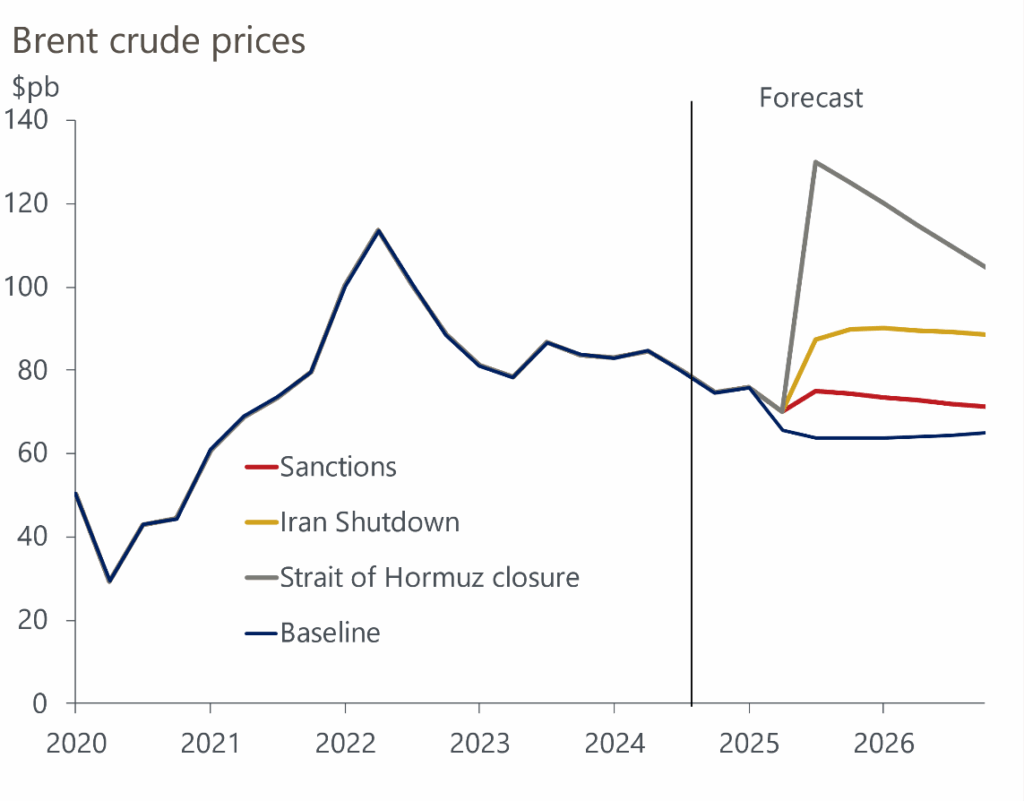

- Energy Volatility: Brent Crude futures are projected to trade at a 25% to 40% premium as markets price in a prolonged supply deficit.

- Logistical Collapse: War risk insurance premiums for tankers are expected to increase by 500% or more, effectively halting non-insured transit.

- Macroeconomic Headwinds: Expected GDP contractions in energy-dependent regions, particularly the EU, as industrial input costs rise sharply.

The Brent Crude Surge and the Inflationary Spiral

The market’s reaction to the blockade is immediate and clinical. Because the Strait of Hormuz is the only exit for exports from the Persian Gulf, the loss of this chokepoint removes millions of barrels per day from the global ledger. For companies like ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX), this creates a paradoxical environment: while upstream revenues increase due to higher prices, the systemic risk to global demand increases.

Here is the math. If Brent Crude shifts from a baseline of $80 to $115 per barrel, the direct impact on the Consumer Price Index (CPI) in energy-importing nations is immediate. We are seeing a correlation where every $10 increase in oil typically adds 0.2% to 0.5% to headline inflation, depending on the region’s energy mix.

But the balance sheet tells a different story for the broader industrial sector. Manufacturers relying on petroleum-based feedstocks are facing an overnight increase in COGS (Cost of Goods Sold). This forces a choice: absorb the margin compression or pass the cost to the consumer, further fueling the inflationary fire.

To understand the scale of the disruption, consider the following projections for the current quarter:

| Metric | Pre-Blockade (Est.) | Post-Blockade (Projected) | Variance (%) |

|---|---|---|---|

| Brent Crude (per barrel) | $82.00 | $118.00 | +43.9% |

| War Risk Insurance Premium | 0.05% | 0.35% | +600.0% |

| EU Industrial Output (Q2 2026) | +1.2% | -0.8% | -1.5% (Abs) |

| Global Shipping Rates (BDI) | 1,800 | 2,600 | +44.4% |

How Energy Majors Hedge Against Geopolitical Asphyxiation

The “supermajors” are not standing still. BP (NYSE: BP) and Shell (NYSE: SHEL) are currently optimizing their logistics to prioritize non-Gulf sources, shifting focus toward West African and North American shale. However, the physical reality of tanker capacity cannot be solved with a spreadsheet. The redirection of fleets takes weeks, not hours.

The real risk lies in the “just-in-time” inventory models that dominate modern supply chains. Most refineries operate with thin margins of crude inventory. A total blockade creates an immediate liquidity crisis for refineries that lack diversified sourcing, leading to potential outages in gasoline and diesel production.

“The fragility of the global energy architecture is exposed whenever a single geographic chokepoint is weaponized. We are no longer looking at a price fluctuation, but a structural failure of energy security that requires a total redesign of strategic reserves.”

This sentiment is echoed across institutional desks. The Reuters Commodities desk has noted that the market is now pricing in a “permanent risk premium,” meaning prices will not return to previous levels even after a diplomatic resolution, as the perceived reliability of the region has been permanently downgraded.

The Logistics Bottleneck and the Baltic Dry Index

Beyond oil, the blockade creates a contagion effect in global shipping. The Baltic Dry Index (BDI), a bellwether for global trade, is reacting to the sudden scarcity of available vessels. As tankers are rerouted or trapped, the cost of chartering ships increases across all categories.

Here is where it gets complicated. The insurance industry, led by entities like Lloyd’s of London, typically declares “War Risk” zones during such blockades. Once a zone is designated as high-risk, standard policies are voided. Shippers must purchase additional coverage, which is currently priced at exorbitant rates. This effectively taxes every barrel of oil that attempts to bypass the blockade via longer, more expensive routes around the Cape of Good Hope.

For a business owner, In other words the “landed cost” of goods is rising. Whether you are importing electronics or raw materials, the freight surcharge is becoming a dominant line item on the P&L. You can track these systemic shifts through Bloomberg Markets, where the volatility index (VIX) is mirroring the instability in the Strait.

Central Bank Dilemmas: Interest Rates vs. Energy Shocks

The Federal Reserve and the European Central Bank (ECB) are now trapped in a classic macroeconomic vice. Normally, the response to rising inflation is to hike interest rates to cool demand. However, this is a supply-side shock. Raising rates does not produce more oil; it only increases the cost of borrowing for businesses already struggling with higher energy inputs.

If the Fed maintains high rates to fight the energy-driven inflation, they risk triggering a deep recession. If they cut rates to support the economy, they risk letting inflation become entrenched. This is the “Stagflation Trap” that economists have feared since the 1970s.

The relationship between the SEC and public energy companies is too under scrutiny. We expect a surge in 8-K filings as companies disclose “material risks” related to their exposure to the Middle East. Investors should closely monitor the SEC EDGAR database for updates on how Chevron (NYSE: CVX) and others are adjusting their forward guidance in light of these disruptions.

The result? A flight to quality. We are seeing a rotation out of growth stocks and into “hard assets” and energy-independent infrastructure. The market is no longer betting on a quick diplomatic fix; it is pricing in a new era of energy fragmentation.

the blockade in the Strait of Hormuz serves as a brutal reminder that the global economy is only as strong as its weakest chokepoint. For the strategic investor, the play is no longer about timing the dip, but about diversifying away from geographic fragility. Those who fail to hedge against this “asphyxiation” will uncover their margins erased by the time the next quarterly report is due.

For further analysis on global energy trends, refer to the International Energy Agency (IEA) reports on strategic petroleum reserves.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.