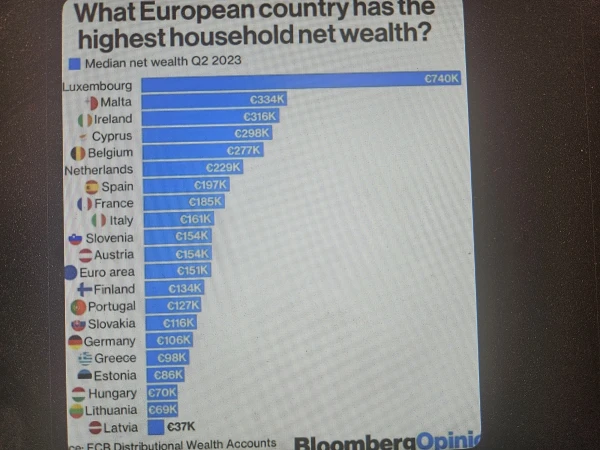

Latvia currently holds the lowest household wealth position across the European Union, according to recent economic data highlighting a stark disparity in asset accumulation compared to its Baltic neighbors and Western European peers. This financial lagging is not merely a matter of lower salaries, but a systemic gap in net assets—the total value of what households own minus what they owe—that leaves the Latvian population uniquely vulnerable to economic volatility.

For anyone tracking the Baltic trajectory, this is a sobering realization. We often group Estonia, Latvia, and Lithuania together as a “Baltic Tiger” bloc, but the wealth data reveals a fragmented reality. While the region has seen aggressive GDP growth over the last two decades, that prosperity hasn’t trickled down into the private coffers of the average Latvian household. It is the difference between a country that looks successful on a government spreadsheet and a population that feels the pinch every time they check their savings account.

Why Latvia Trails Estonia and Lithuania

The gap isn’t just about the numbers; it’s about the nature of the assets. In Estonia, a more aggressive pivot toward digitalization and a robust startup ecosystem have created a new class of equity-wealthy citizens. In Lithuania, a more diversified industrial base has provided a steadier climb. Latvia, however, has struggled with a slower transition of its primary industries and a more cautious approach to private investment.

According to data from Eurostat, the disparity is most evident when looking at “net wealth,” which includes real estate and financial assets. A significant portion of Latvian household “wealth” is tied up in primary residences—homes people live in rather than assets they can leverage for growth. When you strip away the roof over their heads, the liquid capital available to the average Latvian family is among the lowest in the Eurozone.

This creates a dangerous cycle. Without a cushion of liquid assets, households cannot invest in education, entrepreneurship, or home improvements that drive further value. They are effectively locked in a survivalist economic mode, where a single medical emergency or job loss can be catastrophic.

The Ghost of Post-Soviet Asset Management

To understand why Latvia is in last place, we have to look at the historical baggage of asset ownership. The transition from a planned economy to a market economy in the 1990s was messy. While land and property were privatized, the process didn’t always favor the broad middle class. Instead, wealth concentrated in a few hands, leaving the general population with a cultural distrust of long-term financial instruments like stocks or bonds.

This lack of “investment culture” is a silent killer of wealth. Many Latvians still prefer keeping savings in low-interest bank accounts or physical assets, missing out on the compounding growth of global markets. The OECD has frequently noted that financial literacy and access to diverse investment vehicles are critical drivers of household wealth—areas where Latvia has historically lagged.

“The challenge for Latvia is not just increasing the nominal income of its citizens, but transforming that income into sustainable wealth through diversified assets and improved financial inclusion.”

How Recent Inflation Eroded the Safety Net

The timing of this wealth slump is particularly brutal. Between 2022 and 2024, Latvia faced some of the highest inflation rates in the EU, driven largely by skyrocketing energy costs and food prices. For a household already sitting at the bottom of the wealth ladder, inflation isn’t just a headline; it’s a thief that steals the remaining shreds of their purchasing power.

When the cost of living spikes, those without significant assets are forced to dip into their meager savings or take on high-interest debt. This “negative wealth accumulation” means that while the GDP might be growing, the actual financial health of the individual is deteriorating. We are seeing a phenomenon where the macro-economy is thriving while the micro-economy—the kitchen table budget—is in crisis.

The Bank of Latvia has consistently monitored these pressures, noting that while labor markets remain tight and wages are rising, the real-term gains are being swallowed by the cost of basic necessities, preventing the build-up of the very household wealth the country so desperately needs.

Breaking the Cycle of Financial Fragility

Getting out of last place requires more than just a few years of GDP growth. It requires a structural shift in how wealth is generated and protected in Latvia. This means moving beyond a reliance on real estate and fostering a culture of equity investment and entrepreneurship.

One potential lever is the modernization of the tax code to incentivize long-term savings and private pensions. If the government can make it more attractive to invest in the market than to leave money in a stagnant savings account, the needle on household wealth could finally move. Additionally, increasing the competitiveness of the SME (Small and Medium Enterprise) sector would allow more citizens to own the means of production, rather than just selling their labor.

The stakes are high. A country with the lowest household wealth in the EU is a country with a fragile social contract. When people feel they have no stake in the economic success of their nation because they aren’t seeing it in their own bank accounts, social cohesion begins to fray.

The bottom line: Latvia’s position at the bottom of the wealth rankings is a wake-up call. It tells us that growth without distribution is an incomplete victory. The goal now isn’t just to grow the economy, but to ensure that the people living in it actually own a piece of that growth.

Do you think the focus should be on raising minimum wages or providing better tax incentives for private investments to bridge this gap? Let’s discuss the most effective way to build generational wealth in the Baltics.