Oil prices retreated on May 13, 2026, following a period of high volatility driven by escalating tensions in the Strait of Hormuz and stalled diplomatic negotiations between Washington and Tehran. The correction follows a sharp 4% increase, as traders pivot from geopolitical fear to fundamental data regarding US crude inventories.

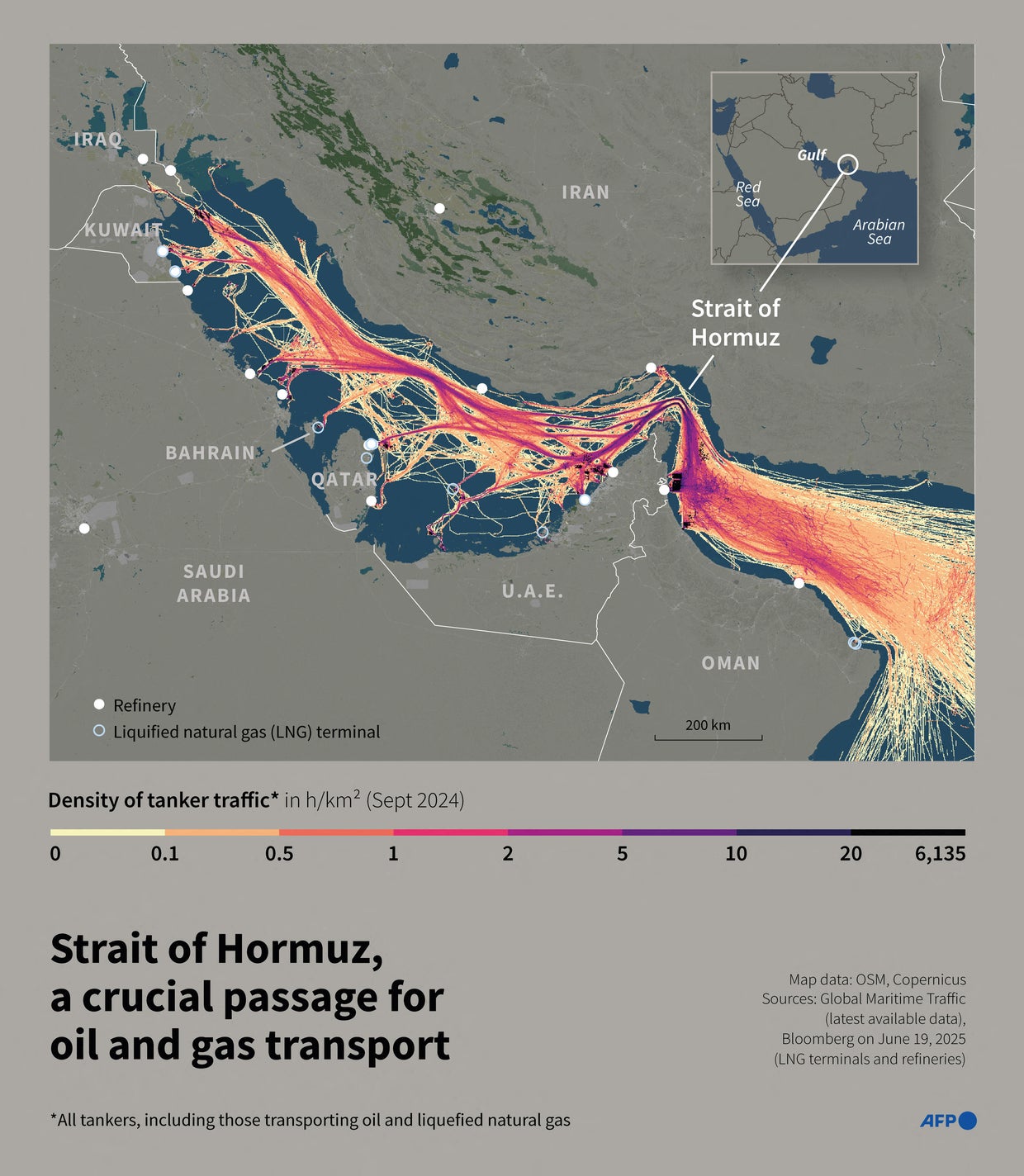

This price action is more than a simple daily fluctuation; it represents the struggle between the “geopolitical risk premium” and the underlying macroeconomic reality. For institutional investors, the volatility in the energy complex serves as a leading indicator for global inflation and a primary driver for the Federal Reserve’s interest rate trajectory. When the market prices in a potential closure of the Strait of Hormuz—a chokepoint for roughly 20% of global petroleum consumption—the risk premium expands rapidly. However, as seen in the current correction, that premium evaporates quickly when the physical supply data, specifically from the US Energy Information Administration (EIA), suggests a surplus.

The Bottom Line

- Risk Premium Decay: The market is currently pricing out an immediate total closure of the Strait of Hormuz, shifting focus back to inventory levels.

- Inventory Headwinds: Unexpected builds in US crude stocks are capping the upside for ExxonMobil (NYSE: XOM) and Chevron (NYSE: CVX).

- Macro Inflationary Pressure: Sustained oil volatility threatens the Fed’s 2% inflation target, potentially delaying anticipated rate cuts in Q3.

The Geopolitical Risk Premium vs. Fundamental Reality

For the past several trading sessions, the narrative was dominated by the failure of truce negotiations between the US and Iran. This diplomatic deadlock triggered a reflexive buy-side response, pushing prices up by 4% as traders hedged against supply disruptions. But the balance sheet tells a different story.

The market is currently grappling with a “fear trade” that has decoupled from physical demand. While the threat of strikes against Iranian infrastructure creates short-term spikes, the long-term trend is anchored by global demand forecasts. If the Strait of Hormuz were to experience a partial or total blockage, the impact would be immediate and severe, but the market knows that the International Energy Agency (IEA) and OPEC+ possess strategic levers to mitigate short-term gaps.

Here is the math: A 1% disruption in global supply typically adds a significant premium to the barrel, but without a sustained physical shortage, that premium is a speculative bubble. The current dip indicates that speculators are closing their long positions to lock in profits before the next round of EIA data.

“The market is currently oscillating between a geopolitical nightmare and a fundamental surplus. Until we see a physical disruption in flow, the ‘Hormuz Premium’ will remain a transient volatility event rather than a structural price floor.”

The EIA Variable and the Inventory Surplus

While headlines focus on Tehran and Washington, the real driver of the current price retreat is the US inventory data. The market is anticipating a build in crude oil stocks, which signals a mismatch between production and consumption.

When US inventories rise, it puts downward pressure on West Texas Intermediate (WTI). This creates a divergence between the geopolitical narrative (which suggests scarcity) and the warehouse narrative (which suggests plenty). For logistics giants like FedEx (NYSE: FDX) and UPS (NYSE: UPS), this volatility is a nightmare for fuel hedging strategies. A sudden 4% jump followed by a sharp correction makes it nearly impossible to lock in predictable operating costs.

Let’s look at the performance metrics leading into the May 13 window:

| Benchmark | Price Action (7-Day) | Volatility Index (VIX-Energy) | Primary Driver |

|---|---|---|---|

| Brent Crude | +2.1% (Net) | High | Hormuz Tensions |

| WTI Crude | +1.4% (Net) | Medium | US Inventory Builds |

| Gasoline Futures | +0.8% (Net) | Low | Seasonal Demand |

The Macro Ripple Effect: Inflation and the Federal Reserve

The volatility in oil prices does not exist in a vacuum. It flows directly into the Consumer Price Index (CPI), which in turn dictates the Federal Reserve’s policy. If oil prices remain elevated due to geopolitical instability, “cost-push inflation” becomes a reality, forcing the Fed to maintain higher interest rates for longer.

This creates a secondary shock for the broader economy. High interest rates increase the cost of capital for business owners, slowing down CapEx spending. For the energy sector, this is a double-edged sword. While Saudi Aramco (TADAWUL: 2222) benefits from higher prices, the broader industrial sector suffers from the increased cost of borrowing and transportation.

But there is a catch. If the correction continues and prices drop significantly, we may see a shift in the Bloomberg Commodity Index, signaling a broader slowdown in global economic activity. The market is essentially searching for a “Goldilocks” price—high enough to support producer margins but low enough to prevent an inflation spiral.

Institutional investors are now closely watching the Reuters feed for any sign of a renewed diplomatic breakthrough. A successful negotiation between the US and Iran would likely strip the remaining risk premium from the market, potentially sending prices toward the $70- $75 range per barrel.

The Strategic Trajectory

Moving forward, the market will likely remain range-bound until one of two things happens: a physical disruption in the Strait of Hormuz or a definitive shift in US Federal Reserve guidance. The current dip is a rational correction, not a trend reversal.

For the pragmatic investor, the play here is to ignore the noise of “strikes” and “tensions” and focus on the EIA’s weekly reports. The physical reality of how many barrels are sitting in Cushing, Oklahoma, will always outweigh the rhetoric coming out of diplomatic summits in the long run.

Expect continued volatility through the end of Q2. The intersection of geopolitical instability and fluctuating US inventories creates a high-beta environment where quick pivots are necessary. The smart money is not betting on a crash or a spike, but on the volatility itself.