Recent reporting indicates Saudi Arabia is privately urging escalation against Iran, marking a potential collapse of the 2023 détente. This shift threatens global oil stability and regional security architecture. Investors and diplomats must monitor Riyadh’s strategic pivot closely as tensions rise across the Gulf.

This proves rare that the quiet corridors of diplomacy scream louder than the headlines, but this week, the silence from Riyadh is deafening. A report emerging from Prague suggests that behind the closed doors of high-level summits, Saudi leadership is pressing for a harder line against Tehran. Here is why that matters. For the past three years, the world has operated under the assumption that the China-brokered rapprochement was holding. If that foundation is cracking, the seismic shifts will be felt far beyond the Middle East.

I have spent years analyzing cross-border finance and geopolitical risk, and I can tell you that markets hate uncertainty more than bad news. The narrative coming out of Seznam Zprávy points to a strategic recalibration. But there is a catch. Publicly, both nations maintain a stance of cooperation. Privately, the proxy conflicts in Yemen and Syria suggest a different reality. We are witnessing the friction between diplomatic optics and strategic necessities.

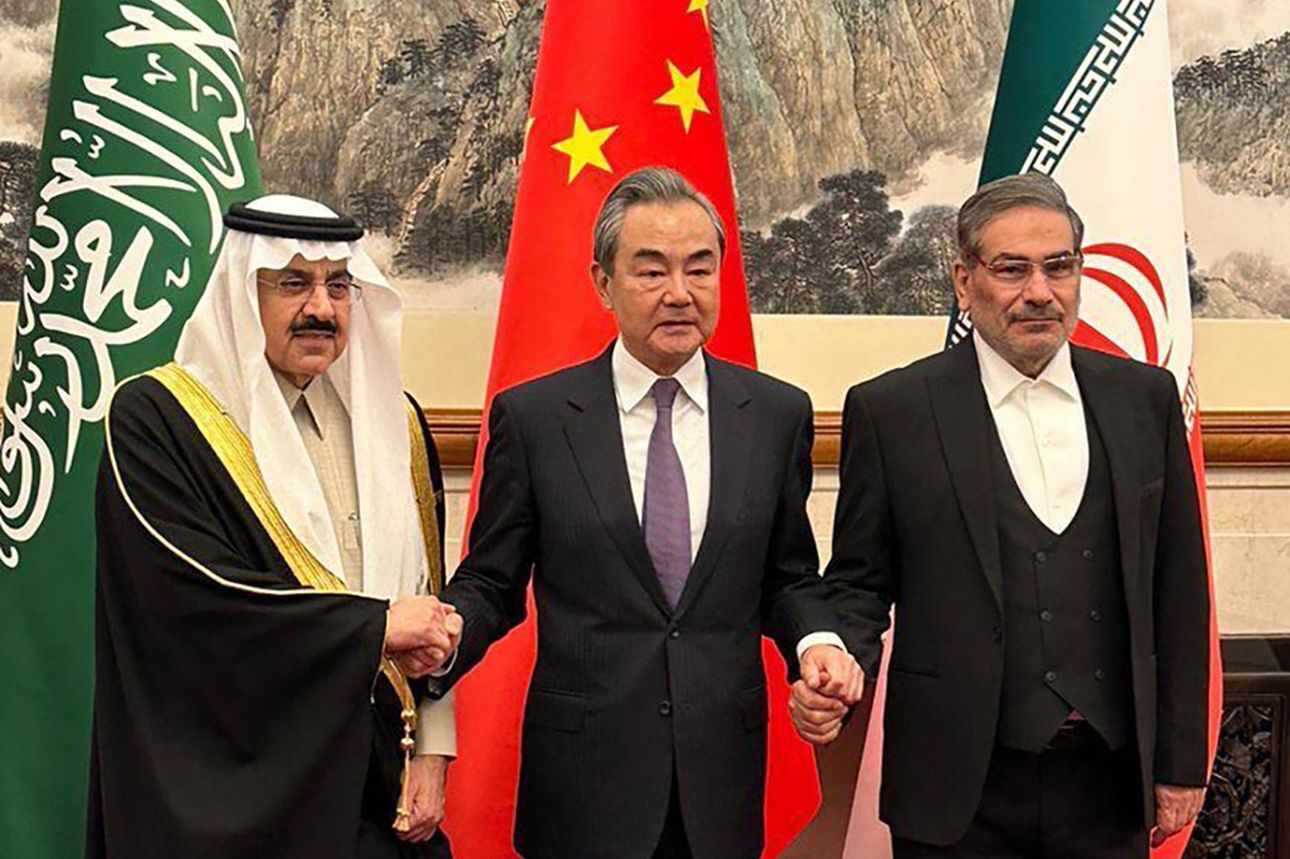

The Fragility of the China-Brokered Détente

When Beijing facilitated the restoration of ties in 2023, it was hailed as a masterpiece of modern statecraft. The agreement promised to reopen embassies and prioritize security cooperation. Still, structural rivalries do not vanish with a handshake. The current reports of Saudi pressure for escalation indicate that the Kingdom views Iran’s nuclear advancements and regional proxy activity as an existential threat that diplomacy alone cannot contain.

This is not merely about territorial disputes. It is about the architecture of power in the Gulf. Saudi Vision 2030 requires a stable neighborhood to attract the foreign direct investment necessary to diversify away from oil. If Iran destabilizes the region, the economic model falters. Riyadh may feel compelled to shift from containment to active pressure. This dynamic creates a volatile environment where miscalculation becomes a significant risk.

Consider the words of Barbara Leaf, a former U.S. Assistant Secretary of State and expert at the Atlantic Council, who has long warned about the limits of such agreements. In a recent analysis on regional security, she noted:

“The restoration of diplomatic relations does not equate to a resolution of underlying strategic conflicts. Without addressing the proxy networks and nuclear concerns, the détente remains a ceasefire rather than a peace.”

Her assessment underscores the precariousness of the current moment. If Saudi Arabia is indeed pushing for escalation, it suggests they believe the cost of inaction now outweighs the economic risks of conflict.

Global Supply Chains and the Oil Premium

Let’s be clear about the economic stakes. The Strait of Hormuz remains the jugular vein of the global energy market. Approximately 20% of the world’s oil consumption passes through this narrow waterway. Any escalation between Riyadh and Tehran immediately introduces a risk premium into crude prices. For the global macro-economy, this translates to inflationary pressure that central banks are ill-equipped to handle in 2026.

International supply chains are already fragile. A spike in energy costs disrupts shipping logistics, manufacturing inputs, and consumer spending power from Frankfurt to Latest York. Investors demand to seem beyond the headline price of Brent crude. The real danger lies in insurance premiums for maritime transport. If insurers classify the Gulf as a high-risk war zone, shipping costs skyrocket, passing those costs directly to the finish consumer.

the shift impacts the broader security architecture. The United States, although reducing its direct footprint, remains the security guarantor for many Gulf states. Increased tension forces Washington to choose between engagement and retrenchment. This ambiguity can embolden adversaries and unsettle allies. The Center for Strategic and International Studies frequently highlights how these regional dynamics intertwine with U.S. Strategic priorities.

Defense Postures and Regional Capabilities

To understand the potential scale of conflict, we must look at the hard data. Both nations have significantly modernized their defense capabilities over the last decade. Saudi Arabia has invested heavily in air defense and precision munitions, while Iran has focused on asymmetric warfare and drone technology. The following table outlines the comparative metrics that define this balance of power.

| Metric | Saudi Arabia | Iran |

|---|---|---|

| Military Expenditure (2023) | $75.8 Billion | $10.3 Billion |

| Oil Production Capacity | ~12.3 Million Barrels/Day | ~3.2 Million Barrels/Day |

| Active Military Personnel | ~257,000 | ~610,000 |

| Primary Strategic Focus | Air Defense & Precision Strike | Asymmetric & Proxy Networks |

Data sourced from SIPRI and OPEC Annual Reports.

The disparity in spending is stark, yet the strategic focus differs fundamentally. Saudi capital buys technological superiority, while Iran leverages manpower and regional influence. In a prolonged conflict, endurance matters more than initial firepower. This is where the economic divergence becomes critical. Saudi Arabia’s budget is tied to oil prices; Iran’s is tied to survival mechanisms and sanctions evasion.

The Investor’s Playbook for Regional Volatility

So, what should the informed observer do with this information? First, recognize that diplomacy is often a lagging indicator. By the time official statements are released, the market has usually priced in the risk. The reports of behind-the-scenes pressure are a leading indicator of policy shifts. Monitoring defense contracts and diplomatic travel patterns can provide early signals.

Second, diversify exposure to energy-dependent sectors. The Brookings Institution often advises that hedging against geopolitical risk requires looking at alternative energy corridors and supply chains. If the Gulf becomes unstable, trade routes may shift toward the Mediterranean or Indo-Pacific corridors.

Finally, maintain a nuanced view of alliances. The Middle East is no longer a binary theater of proxies. It is a multipolar hub involving China, India, and the West. Saudi Arabia’s relationship with Beijing complicates the traditional U.S. Security umbrella. Understanding these triangulations is essential for accurate risk assessment.

We are standing at a crossroads. The window for peaceful consolidation of the 2023 deal is closing. If Riyadh chooses escalation, the ripple effects will redefine the global order for the rest of the decade. Stay vigilant, retain your data close, and remember that in geopolitics, the quietest moves often develop the loudest noise.