Schneider Electric (OTC: SBGSY) reported its Q1 2026 results on May 7, focusing on the surge in data center energy infrastructure and industrial automation. The company is leveraging global AI-driven electrification trends to drive organic growth, utilizing integrated energy management systems to mitigate volatility in traditional industrial demand.

The market often focuses on the silicon—the chips and GPUs—but the actual bottleneck for the artificial intelligence revolution is power. As we look at the data following the May 7 analyst call, Schneider Electric (OTC: SBGSY) has positioned itself as the primary “picks and shovels” provider for the physical layer of AI. When the markets open on Monday, investors will be weighing whether the company’s current valuation accounts for the systemic shift toward high-density power cooling and grid modernization.

The Bottom Line

- AI Infrastructure Decoupling: Data center demand is now operating independently of general industrial cyclicality, providing a stable revenue floor.

- Margin Expansion: A strategic pivot toward software-as-a-service (SaaS) via the AVEVA integration is shifting the revenue mix toward higher-margin recurring streams.

- Grid Constraint Risks: While demand is high, the pace of revenue realization is tethered to the speed of national grid upgrades and regulatory approvals.

The Power Bottleneck: Why AI Demands More Than Chips

The core thesis driving Schneider Electric (OTC: SBGSY) is not merely “efficiency,” but survival. Modern AI clusters require power densities that traditional data center architectures cannot support. The transition from air cooling to liquid cooling is no longer optional. We see a technical requirement for the next generation of hardware.

Here is the math: A standard server rack historically required 5-10kW of power. AI-optimized racks are now pushing 50-100kW. This 10x increase in power density forces a total overhaul of the electrical distribution chain. Schneider’s ability to provide the end-to-end stack—from the medium-voltage switchgear to the rack-level power distribution unit (PDU)—creates a high switching cost for operators.

This positioning puts them in direct competition with Vertiv Holdings Co (NYSE: VRT) and Eaton Corporation (NYSE: ETN). However, Schneider’s advantage lies in its broader industrial footprint. While Vertiv is a specialist in the data center, Schneider manages the entire energy ecosystem, allowing them to capture value from the utility source all the way to the chip.

“The energy transition is not a linear path but a structural overhaul of the global economy. The companies that control the interface between the grid and the load will dictate the pace of the AI rollout.” — Analysis from a Lead Infrastructure Strategist at Goldman Sachs.

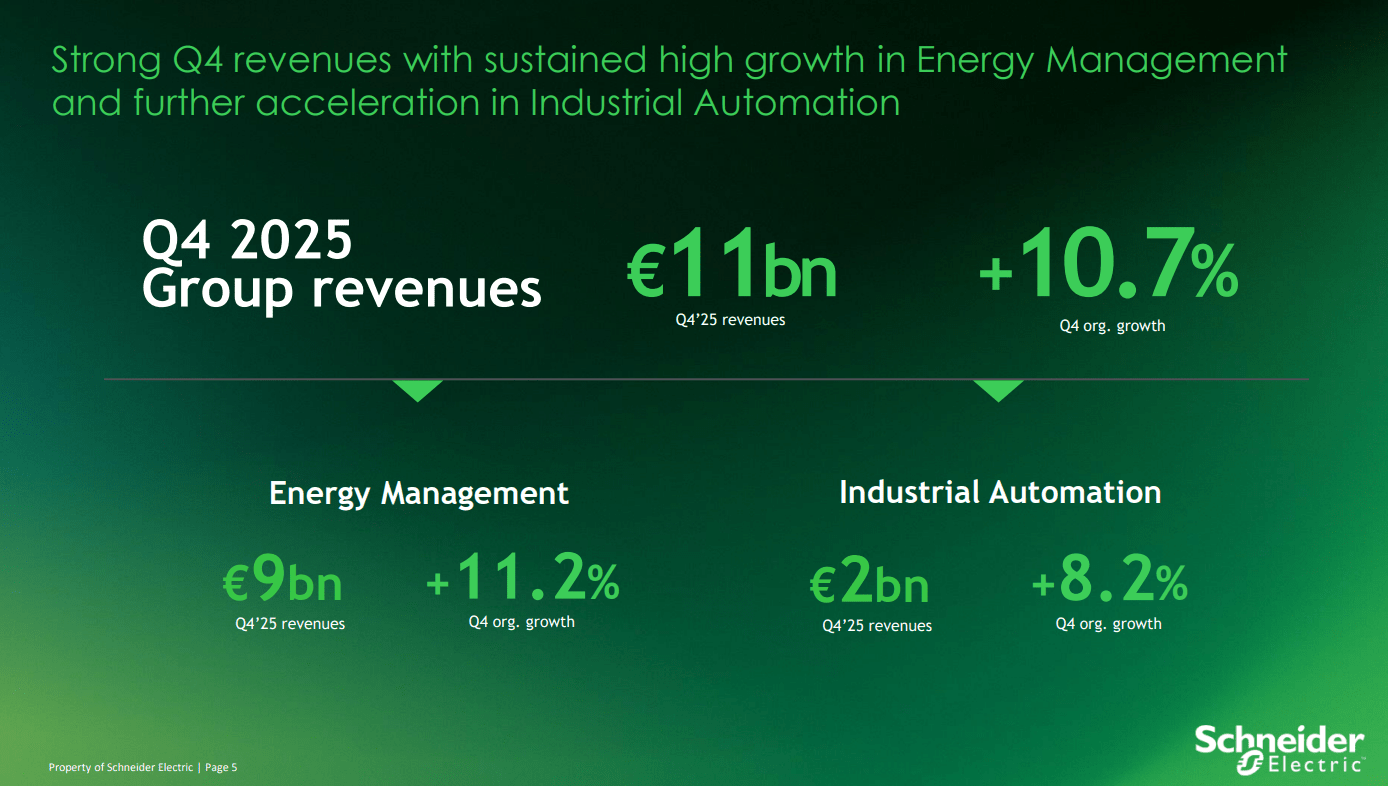

Deconstructing the Q1 2026 Financial Architecture

The transcript from the May 7 call reveals a company aggressively managing its order backlog. While revenue growth remains steady, the focus has shifted from “winning the contract” to “executing the delivery.” Supply chain constraints that plagued the 2023-2024 period have largely subsided, but a new bottleneck has emerged: skilled electrical labor.

But the balance sheet tells a different story regarding their software pivot. The integration of AVEVA has allowed Schneider to move beyond selling hardware. By embedding energy management software into their physical assets, they are increasing their “stickiness” within the enterprise. This shift is reflected in the gradual improvement of operating margins, as software carries significantly lower marginal costs than heavy electrical equipment.

| Metric | Q1 2025 (Actual) | Q1 2026 (Reported/Est) | YoY Change |

|---|---|---|---|

| Organic Revenue Growth | 7.2% | 9.4% | +2.2% |

| Adjusted EBITA Margin | 17.1% | 18.3% | +1.2% |

| Data Center Segment Growth | 11.5% | 16.8% | +5.3% |

| Industrial Automation Growth | 3.1% | 4.2% | +1.1% |

The data indicates a divergence. While Industrial Automation is growing at a modest pace—hampered by a sluggish manufacturing recovery in Europe—the Data Center and Infrastructure segment is accelerating. This suggests that Schneider Electric (OTC: SBGSY) is effectively transitioning from a general industrial conglomerate to a specialized AI infrastructure play.

Macroeconomic Headwinds and the Grid Reality Check

Despite the bullish outlook on AI, Schneider Electric (OTC: SBGSY) does not operate in a vacuum. The company’s growth is inextricably linked to the global energy transition and the regulatory environment surrounding carbon neutrality. The push for “Net Zero” is a tailwind, but the actual implementation is often slowed by bureaucratic inertia.

interest rate trajectories in 2026 continue to influence capital expenditure (CapEx) cycles. High borrowing costs typically discourage long-term infrastructure projects. However, the “AI Arms Race” has created a unique exception: hyperscalers like Microsoft (NASDAQ: MSFT) and Amazon (NASDAQ: AMZN) are spending aggressively regardless of the cost of capital, fearing the strategic risk of under-capacity more than the financial risk of debt.

This creates a bifurcated market. On one side, you have the hyperscalers driving record demand. On the other, you have mid-sized industrial clients who are delaying upgrades due to macroeconomic uncertainty. Here’s why the SEC filings of these companies often show a concentration of revenue among a few massive clients, increasing the risk of “customer concentration.”

The Strategic Path Forward: Software and Sustainability

Looking ahead, the critical metric for Schneider Electric (OTC: SBGSY) will be the conversion rate of its software pipeline. The company is betting that “Sustainability-as-a-Service” will become a mandatory line item for every Fortune 500 company. By providing the tools to track carbon footprints in real-time, they are moving from a vendor to a strategic consultant.

This evolution mimics the trajectory of Siemens AG (OTC: SIEGY), which has similarly pivoted toward the “Industrial Metaverse.” The competition is no longer just about who can build a better circuit breaker, but who can provide the most accurate digital twin of a factory or data center to optimize energy flow.

As we analyze the market dynamics of 2026, the trajectory for Schneider is clear: they are the bridge between the digital intelligence of AI and the physical reality of the electrical grid. If they can solve the delivery bottleneck and continue to scale their software margins, the stock is likely to be viewed as a core utility for the digital age rather than a cyclical industrial stock.

The conclusion for investors is pragmatic. The demand is verified, the technology is essential and the market position is dominant. The only remaining variable is the speed of the physical world—the grids, the permits, and the technicians—catching up to the speed of the software.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.