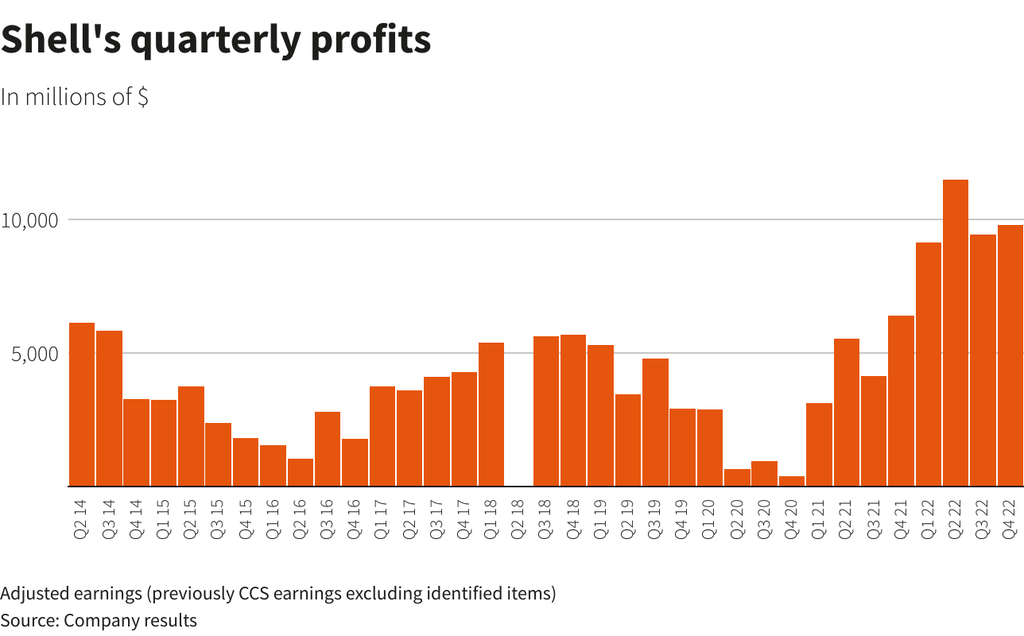

Shell (NYSE: SHEL) reported a first-quarter profit of $6.9 billion, exceeding analyst expectations. The earnings growth, including a 19% increase in quarterly profit, was primarily driven by elevated global oil prices linked to geopolitical instability in Iran, despite a strategic decision to reduce the company’s share buyback program.

This earnings beat is a textbook example of the “geopolitical premium.” While Shell’s operational efficiency plays a role, the primary catalyst here is external. The market is currently pricing in a high degree of risk regarding Middle Eastern supply chains, which has inflated the price of Brent Crude and provided a windfall for integrated oil majors. However, for the sophisticated investor, the headline profit is a distraction from the more telling movement: the reduction in capital returned to shareholders via buybacks.

The Bottom Line

- Windfall over Wellness: Profits were driven by external price surges (geopolitical risk in Iran) rather than internal cost-cutting or volume growth.

- Capital Discipline Shift: The reduction in share buybacks suggests a strategic pivot toward debt reduction or increased capital expenditure (Capex) for future energy transitions.

- Macro Sensitivity: Shell’s current valuation remains hyper-sensitive to OPEC+ quotas and Iranian stability, creating a high-beta environment for shareholders.

The Geopolitical Hedge: Why Iran’s Instability Fuels the Bottom Line

The math is straightforward. When conflict disrupts the Strait of Hormuz or threatens Iranian production, the global supply curve shifts left, pushing prices higher. Shell, with its massive upstream portfolio, captures this margin expansion almost instantly. But the balance sheet tells a different story.

Current market data indicates that Brent Crude has maintained a volatility index significantly higher than the five-year average. For Shell (NYSE: SHEL), this volatility acts as a double-edged sword. While it boosts immediate quarterly earnings, it complicates long-term planning for their “Powering Progress” strategy. The company is essentially benefiting from a “war premium” that is inherently unsustainable.

Here is the broader context: the energy sector is currently grappling with a contradiction. While the International Energy Agency (IEA) forecasts a long-term decline in fossil fuel demand, the short-term reality is that geopolitical shocks are making oil more profitable than ever. This creates a “transition trap” where companies are tempted to double down on hydrocarbons just as the regulatory environment tightens.

The Buyback Paradox and Capital Allocation

In a typical bull market, a profit beat of this magnitude would be followed by an aggressive increase in share buybacks to boost Earnings Per Share (EPS). Shell did the opposite. By reducing buybacks, management is signaling a shift in priority. What we have is a move often seen when a company anticipates a period of higher volatility or intends to fund a major acquisition.

When we compare this to ExxonMobil (NYSE: XOM), the strategy diverges. While Exxon has remained steadfast in its commitment to massive shareholder returns, Shell appears to be hedging. This suggests that Shell (NYSE: SHEL) may be preparing for a more aggressive pivot into LNG (Liquefied Natural Gas) or renewing its investment in carbon capture technology to avoid future regulatory penalties from the EU.

“The trend of reducing buybacks amidst record profits often indicates a management team that is more concerned with the 2030 balance sheet than the 2026 stock price. Shell is playing a longer, more cautious game than its US peers.”

To understand the scale of this performance, we must look at the hard numbers compared to the previous cycle.

| Metric | Q1 2025 (Est.) | Q1 2026 (Actual) | Variance (%) |

|---|---|---|---|

| Net Profit | $5.79 Billion | $6.9 Billion | +19.1% |

| Brent Crude Avg | $78.50 / bbl | $86.20 / bbl | +9.8% |

| Buyback Allocation | $3.5 Billion | $3.1 Billion | -11.4% |

| Operating Margin | 12.4% | 13.1% | +0.7% |

The Competitive Ripple Effect: BP and Chevron

Shell does not operate in a vacuum. Its earnings report sends a signal to BP (NYSE: BP) and Chevron (NYSE: CVX). When one major reduces buybacks, it often signals a sector-wide shift in how “excess cash” is viewed. If Shell is hoarding cash to weather a potential downturn or to fund a transition, its competitors may be forced to re-evaluate their own dividend sustainability.

the reliance on Iranian instability for profit is a precarious position. If a diplomatic resolution occurs, the “premium” vanishes overnight. This makes the stock more of a geopolitical play than a pure-play energy investment. Investors should monitor the Bloomberg Commodity Index closely; any sharp decline in oil volatility will likely lead to a correction in Shell’s valuation.

The relationship between these entities is symbiotic. They all rely on the same OPEC+ pricing floor, but their internal strategies for the “energy transition” are diverging. While Shell (NYSE: SHEL) is leveraging its LNG dominance to bridge the gap, BP (NYSE: BP) has historically been more aggressive—and volatile—in its shift toward renewables.

Macroeconomic Headwinds: Inflation and Interest Rates

Beyond the boardroom, Shell’s profitability has a direct impact on the global economy. High oil prices, while great for the Shell (NYSE: SHEL) balance sheet, are inflationary. This creates a feedback loop: high energy costs drive up CPI (Consumer Price Index), which prompts central banks to maintain higher interest rates. Higher rates, in turn, increase the cost of borrowing for the very infrastructure projects Shell needs to build for its transition.

For the business owner, this means the “Shell windfall” is essentially a tax on the rest of the economy. When energy majors report record profits due to supply shocks, it typically correlates with increased logistics costs and lower consumer discretionary spending. We are seeing a redistribution of wealth from the consumer to the energy producer, mediated by geopolitical instability.

According to recent Reuters energy analysis, the market is now pricing in a “permanent volatility” regime. This means the days of stable $70 oil are gone, replaced by a swing between $60 and $100 based on headlines from Tehran or Riyadh.

The Forward Outlook: Speculation vs. Strategy

Looking ahead to the close of the next quarter, the key metric will not be the net profit, but the Capex breakdown. If the reduced buybacks are diverted into high-yield LNG assets, the move is a masterstroke. If the cash is simply sitting in low-yield reserves due to management indecision, It’s a missed opportunity.

Investors should look for the next SEC filing to see exactly where the “saved” buyback capital is being allocated. The delta between “profit” and “value creation” is currently wide at Shell. The company is making money, but it is not yet clear if it is making the *right* money for a post-carbon world.

The trajectory is clear: Shell is currently a hedge against global instability. As long as the Middle East remains a powder keg, the stock will likely outperform. But the moment the world stabilizes, the market will stop rewarding the windfall and start demanding a coherent, profitable plan for the energy transition.