{kind=link}

Table of Contents

- 1. Breaking: Viral TikTok PSA on Car-Accident Claims Fuels National Debate Over Filing Routes

- 2. Who To Call After A Car Accident?

- 3. Spotting divergent advice and what it means for you

- 4. At a glance: post-accident contact options

- 5. >collision or thorough coverage – If you plan to file a claim for vehicle repair, you must activate the coverage by notifying the insurer quickly.

- 6. When to Call Your Insurance: Legal and Policy Triggers

- 7. Immediate Steps Before Making the Call

- 8. How to Prepare Your Information for the Insurance Representative

- 9. The Benefits of Notifying Your Insurer Promptly

- 10. Potential Risks of Delaying the Call

- 11. Common Misconceptions about Calling After a Crash

- 12. Real‑World Example: A 2023 multi‑Vehicle Accident in Texas

- 13. Practical Tips for a Smooth Insurance Notification

- 14. Frequently Asked Questions

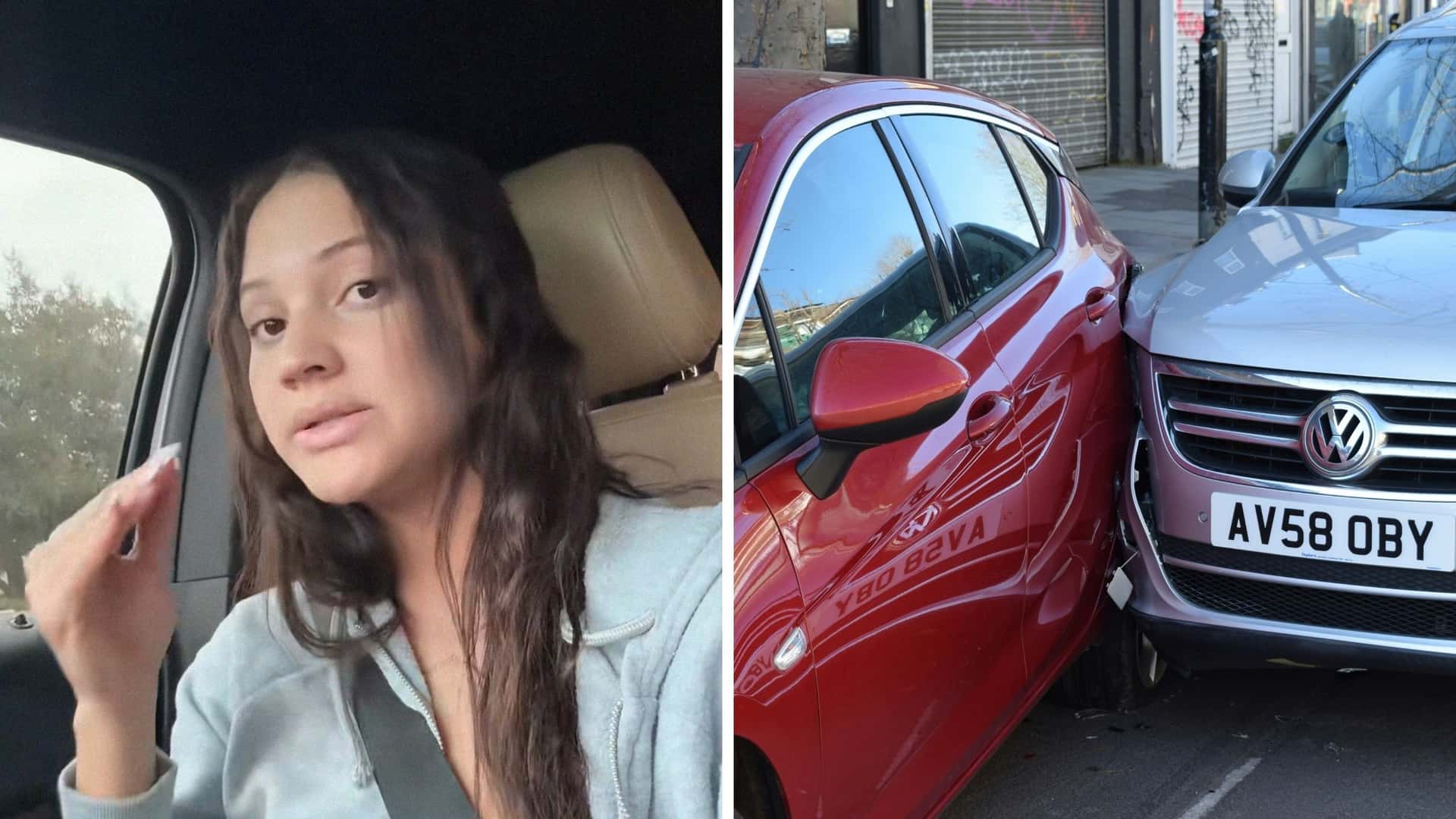

A Florida driver’s social-media post has ignited a nationwide discussion about the best way to file a car-accident claim. A video posted by a Florida woman known on TikTok as @incasethemayanswe argues that, if the crash wasn’t your fault, you should not contact your own insurer to start a claim.The clip has drawn millions of views and sparked both praise and pushback from viewers and legal experts alike.

In her message, she stresses that not all crashes require you to reach out to your own insurance first. “do not call your car insurance company if the accident is not your fault,” she writes in the clip, explaining that the other driver’s insurer should be contacted to file a claim. She says she learned the tactic after a prior incident where filing through her own insurer led to higher costs and a negative mark on her record.

Her experience appears to have two turns. In a later incident, she says she followed the other driver’s insurance route and, after filing, received payment without a premium increase. The video’s claims have resonated with many drivers who say they were unaware they could, or should, file with the at-fault driver’s insurer.

Who To Call After A Car Accident?

Practical guidance varies by state. In Texas, such as, drivers can file a claim directly with the at-fault driver’s insurer. Key step: gather the other driver’s name, insurance company, policy number, license plate, and documentation such as photos, witness contacts, and a police report. Legal experts note that, in many cases, it’s wiser to alert your own insurer first so you can manage communications and preserve your rights under your policy.

Officials emphasize that the other insurance company will look out for its insured, not necessarily your best interests. In Florida, you are not legally required to speak with the other driver’s insurer, but if you do, you should share only basic details, avoid recorded statements, and refrain from discussing fault. Having your own insurer—or a lawyer—handle the claim can protect you if fault later becomes contested.

From there, drivers have options. If you hold the appropriate coverages, your insurer may start repairs or advance payment and then seek reimbursement from the at-fault driver’s insurer. If the other party is cooperative and clearly at fault, filing with their insurer is another viable route, though caution is advised.

Spotting divergent advice and what it means for you

Critics of the viral PSA argue that after a crash, you often need to notify your own insurer to ensure a formal report exists and to coordinate any subsequent dealings with the other side. Some commenters say their claims were better handled by contacting their own insurer first, which sometimes helped protect their rates and coverage. Others point out that, in certain circumstances, going straight to the at-fault driver’s insurer can work—and it did for the author of the viral clip.

Nonetheless of the approach, experts urge drivers to stay organized: document the scene, collect contact and policy details, photograph damage, and obtain an accident report. When in doubt, consult a lawyer to navigate fault disputes and policy language.

At a glance: post-accident contact options

| Scenario | Who To Call | Pros | Important Considerations |

|---|---|---|---|

| Not at fault, fault clearly rests with other driver | Other driver’s insurer (file a claim) or your own insurer | Direct route to compensation; potential for quicker resolution | Other insurer looks out for their client; your own insurer can coordinate recovery |

| Not at fault, fault unclear or disputed | Your own insurer (and possibly a lawyer) | Better claim management and protections if fault is disputed | State rules vary; documentation is essential |

| Florida or similar state nuance | Not required to speak with other driver’s insurer; you may contact them if you choose | Limit exposure and statements; preserve your rights | If you do contact them, share only basic information and avoid recorded statements |

| Direct filing with your own insurer (if coverage allows) | Your own insurer (or a lawyer) | Repair payments and cost recovery can be initiated smoothly | Your premium impact depends on fault determination and policy terms |

Note: Insurance rules vary by state. This article provides general guidance and should not replace professional legal or insurance advice.always verify current laws and policy terms for your location.

Breaking insights aside, the core message for drivers is clear: stay informed about your options, document every detail, and seek professional guidance when fault is in dispute. The evolving advice around post-accident filings underscores how personal experience, policy language, and local rules can shape the right path for your claims journey.

Share your experience: have you successfully filed a claim by contacting the other driver’s insurer, or did you start with your own coverage? Do you want more clarity on what to do after a crash in your state?

What’s your take on the best approach to filing after a crash? Let us know in the comments or join the discussion below.

Disclaimer: This article is for informational purposes and does not constitute legal advice. Laws and insurance practices vary by state.

>collision or thorough coverage – If you plan to file a claim for vehicle repair, you must activate the coverage by notifying the insurer quickly.

When to Call Your Insurance: Legal and Policy Triggers

- State law requirements – most states mandate that you report any accident that results in injury, death, or property damage exceeding a specific dollar threshold (frequently enough $500‑$1,000).

- Policy language – Almost every auto policy includes a “prompt notice” clause requiring you to inform the insurer within a reasonable time, typically 24‑72 hours.

- Collision or comprehensive coverage – If you plan to file a claim for vehicle repair, you must activate the coverage by notifying the insurer as soon as possible.

Immediate Steps Before Making the Call

- Secure the scene – Move vehicles out of traffic if they’re drivable; otherwise, turn on hazard lights and set up warning triangles.

- Check for injuries – Call 911 for medical assistance immediately; a police report will also be generated.

- Document the accident – Take photos of all vehicles, street signs, skid marks, and any visible damage. Record the date, time, and whether conditions.

- Exchange information – Collect names, phone numbers, driver’s license numbers, license plates, and insurance details from every party involved.

How to Prepare Your Information for the Insurance Representative

- Policy number – Have your insurance card or online account ready.

- Accident details – Write a concise, factual statement (who, what, where, when, how).

- Police report number – If a report was filed,note the case number and the issuing agency.

- Witness contacts – List names and phone numbers of any bystanders who saw the crash.

- Medical documents – If injuries occured, keep copies of EMT reports, hospital bills, and doctor notes.

The Benefits of Notifying Your Insurer Promptly

- Faster claim processing – Early notification allows the adjuster to begin the inquiry while evidence is fresh.

- Preserves coverage – Meeting the “prompt notice” requirement protects you from potential claim denial.

- locks in rental car benefits – Many policies automatically provide a temporary rental vehicle if you report within the required window.

- Reduces out‑of‑pocket costs – Timely filing can prevent additional fees, such as deductible waivers for uninsured motorists.

Potential Risks of Delaying the Call

- Policy violation – A delayed report can be interpreted as non‑compliance, leading to claim denial or reduced settlement.

- Lost evidence – Photographs,skid marks,and witness recollections fade quickly,weakening the insurer’s ability to assess fault.

- Higher repair costs – If the othre driver’s insurance is involved, a delayed claim may trigger higher repair estimates due to market price changes.

Common Misconceptions about Calling After a Crash

| Myth | Reality |

|---|---|

| “I’ll call onyl after I see the damage.” | Even minor dents can hide hidden structural issues; insurers need the initial report to evaluate all possible losses. |

| “My premium will automatically rise.” | Most insurers offer a “forgiveness” period for a first accident, and many states prohibit immediate premium hikes without a claim. |

| “I don’t need to call if the other driver is at fault.” | Fault is determined after investigation; reporting ensures you’re protected if the other driver’s insurer disputes liability. |

Real‑World Example: A 2023 multi‑Vehicle Accident in Texas

- Scenario: A chain‑reaction crash on I‑35 involved three cars. Driver A (insured with a Texas‑based carrier) sustained a rear‑end collision and minor whiplash.

- Action taken: Driver A called his insurer within one hour, providing the police report number and photos of the damage.

- Outcome: The insurer’s adjuster arrived the next day, coordinated a tow, and secured a rental car under the “rental reimbursement” endorsement. As the claim was opened promptly, the insurer approved a 30 % deductible waiver for the uninsured motorist coverage, saving Driver A $750.

Practical Tips for a Smooth Insurance Notification

- use the insurer’s mobile app – Most carriers now allow you to upload photos, enter police report details, and start a claim with a few taps.

- Stick to the facts – Avoid speculation about fault; let the adjuster and police determine liability.

- Ask for a claim number – Keep this reference for all future communications and follow‑up calls.

- Document every conversation – Note the date, time, representative’s name, and what was discussed. This creates a paper trail if disputes arise.

- Know your coverage limits – Review your policy’s bodily injury, property damage, and uninsured motorist limits before the call so you can ask targeted questions.

Frequently Asked Questions

Q: What if I’m at fault?

A: Reporting the accident is still mandatory. Your liability coverage will handle the other party’s damages, and a prompt claim can help you avoid additional penalties for late notice.

Q: Can I wait until I’ve seen a repair estimate?

A: no. Insurers need to assess damage before any repair work begins; delaying may lead to claim denial or reduced payout.

Q: do I need to call the other driver’s insurer?

A: only if you’re filing a third‑party claim and have permission from the other driver. Typically, you’ll inform your own insurer, who will then coordinate with the other carrier.

Q: How does a claim affect my No‑Claims discount?

A: In many jurisdictions, a single claim may not impact the discount, especially if it’s covered under comprehensive or collision without fault. check your policy’s specific terms.

Q: What if the police didn’t come to the scene?

A: File an accident report with the Department of Motor Vehicles (or equivalent agency) within the required time frame and provide that report number to your insurer.