On April 21, 2026, the Strait of Hormuz reopened after a 72-hour closure triggered by Iranian naval exercises, sending Brent crude prices surging past $90 a barrel as global markets reacted to eased fears of prolonged supply disruption. The reopening followed intense diplomatic backchannel talks between Oman and Qatar, which facilitated a temporary de-escalation despite Tehran’s continued insistence that it will never relinquish strategic control of the waterway. While shipping lanes have resumed normal operations, analysts warn the underlying volatility remains, with Iran’s Islamic Revolutionary Guard Corps Navy maintaining a heightened presence and conditional threats to reclose the strait if U.S.-led sanctions on its oil exports are not lifted.

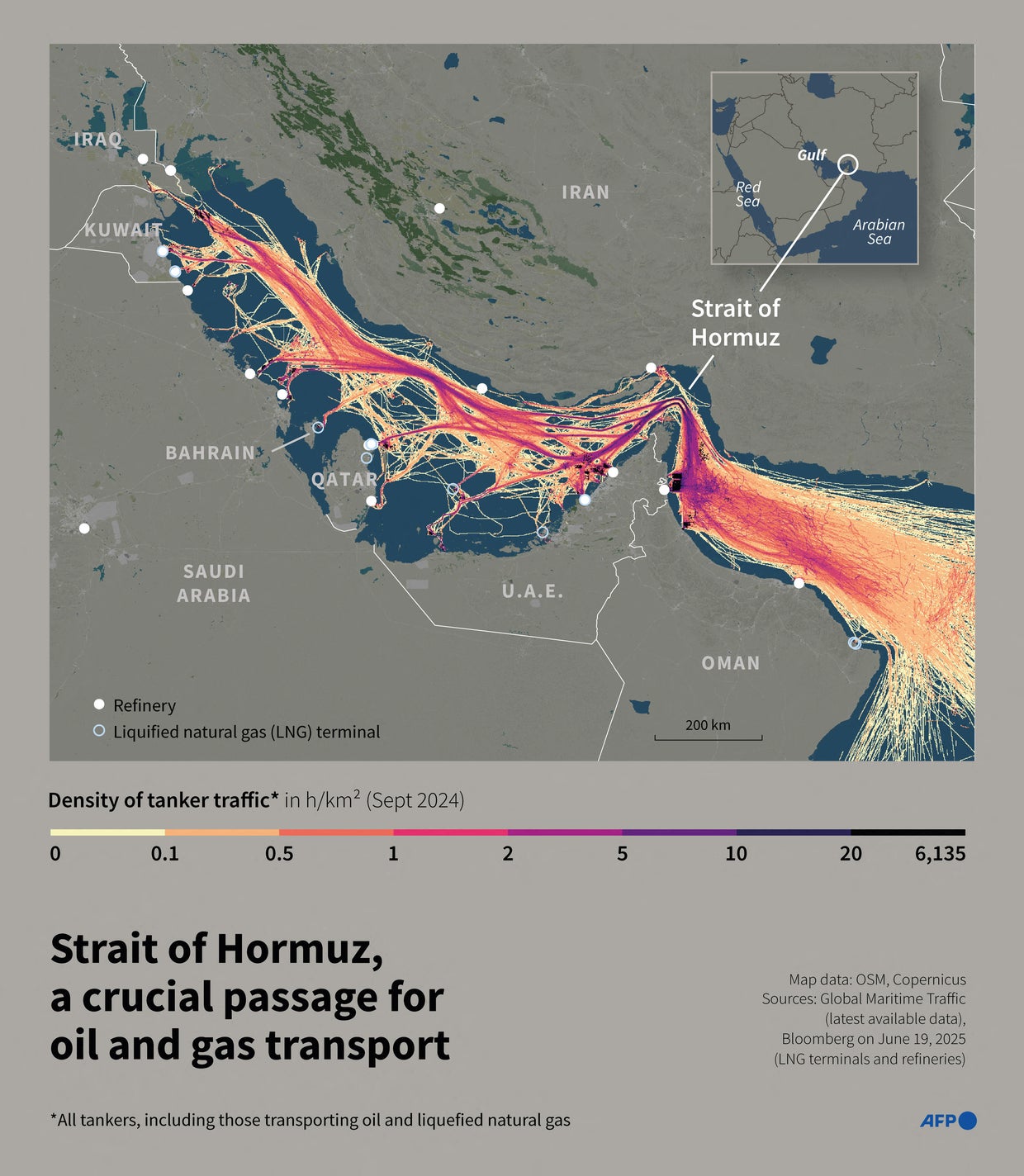

This latest flare-up in the Strait of Hormuz is more than a temporary blip in energy markets—We see a critical pressure point in the evolving architecture of global energy security. Roughly 20% of the world’s oil supply and one-third of liquefied natural gas trade pass through this 21-mile-wide chokepoint between Oman and Iran, making any disruption a direct threat to industrial economies from Germany to Japan. The recurrence of closures, even brief ones, exposes the fragility of just-in-time supply chains still recovering from pandemic-era shocks and the Ukraine war’s energy aftershocks. For markets already navigating sticky inflation and divergent central bank policies, Hormuz volatility acts as a threat multiplier, amplifying risk premiums across freight, insurance, and derivatives trading.

What the initial reports missed is how this episode accelerates a quieter but profound shift: the diversification of global energy routes away from Middle Eastern chokepoints. Since 2023, Saudi Arabia and the UAE have fast-tracked investments in alternative export infrastructure, including the expansion of the Abu Dhabi Crude Oil Pipeline and the development of Saudi’s Red Sea–to–Mediterranean corridor via Neom. Meanwhile, Japan and South Korea have renewed long-term contracts with U.S. Gulf Coast LNG exporters, reducing their reliance on Gulf supplies by 15% compared to 2021 levels. These moves reflect a strategic hedging behavior among major importers who now view Hormuz not as a reliable conduit but as a geopolitical fault line requiring insurance.

“The Strait of Hormuz remains a dagger pointed at the heart of the global economy, but the world is learning to wear armor,” said Dr. Layla Hassan, senior fellow for energy security at the Chatham House in London. “What we’re seeing isn’t panic—it’s prudence. Nations are no longer betting everything on Tehran’s restraint or Washington’s deterrence. They’re building redundancy.”

Equally significant is the evolving role of regional mediators. Oman, long a quiet backchannel facilitator between Washington and Tehran, has intensified its shuttle diplomacy, leveraging its unique position as the only Gulf state to maintain diplomatic relations with Iran throughout recent tensions. Qatar, too, has expanded its mediation portfolio beyond Gaza, using its LNG wealth and neutral stature to host indirect talks. Their combined efforts prevented what could have been a fifth straight closure this year—a scenario that, according to IMF modeling, would have shaved 0.4% off global GDP growth in Q2 2026 through elevated freight costs and production delays.

Yet the underlying strategic contest persists. Iran continues to frame its control of Hormuz as a non-negotiable pillar of national sovereignty, citing historical treaties dating back to the 1975 Algiers Agreement, which established joint Iraqi-Iranian control of the Shatt al-Arab waterway—a precedent Tehran invokes to justify its regional influence. The U.S., while avoiding direct military confrontation, has increased patrols by the Fifth Fleet and deepened intelligence sharing with GCC allies, signaling that freedom of navigation remains a red line. This dynamic creates a dangerous equilibrium: neither side seeks open conflict, but both are prepared to risk escalation to defend core principles.

To understand the stakes, consider the following comparison of key actors’ strategic priorities and capabilities in the Hormuz theater:

| Actor | Primary Objective | Key Capability | Recent Action (Q1 2026) |

|---|---|---|---|

| Iran | Maintain strategic leverage over Hormuz; resist U.S. Sanctions | IRGC Navy fast-attack craft; missile range covering strait | Conducted 3 naval exercises; threatened closure unless sanctions lifted |

| United States | Ensure freedom of navigation; deter Iranian coercion | USS Carrier Strike Group 5; P-8 surveillance; CENTCOM coordination | Increased destroyer patrols; shared real-time tracking with UAE |

| Oman/Qatar | Prevent escalation; preserve regional stability | Diplomatic access to both Tehran and Washington | Facilitated backchannel talks leading to April 19 reopening |

| China/India | Secure energy imports; avoid supply shocks | Strategic petroleum reserves; long-term chartering of tankers | Diverted 12 VLCCs via Cape of Good Hope during closure |

The global implications extend beyond energy. Shipping delays through Hormuz directly impact trade finance, as letters of credit are often tied to estimated arrival times. During the April closure, Lloyd’s List reported a 22% spike in war risk premiums for tankers transiting the Gulf, increasing transport costs by an estimated $3.20 per barrel. For emerging economies like Pakistan and Bangladesh, which rely on imported fuel for power generation, such spikes can trigger fiscal strain and subsidy pressures. The uncertainty complicates long-term investment decisions in energy-intensive industries, from European steelmakers to Indian fertilizer plants, where margin sensitivity to input costs is high.

There is too a less visible but growing concern: the erosion of multilateral norms governing maritime chokepoints. Unlike the Suez or Panama Canals, which operate under internationally recognized treaties, the Strait of Hormuz lacks a binding legal framework governing passage rights. UNCLOS guarantees transit passage, but enforcement relies on state practice and power politics—making it vulnerable to unilateral assertions. As climate change opens Arctic routes and digital trade reshapes logistics, the world may yet find alternatives to Hormuz. But for now, the strait remains a linchpin of 21st-century geoeconomics, where a single naval maneuver can ripple from Riyadh to Rotterdam.

As markets stabilize and tankers resume their steady flow, the real test lies not in whether the strait stays open today, but whether the international system can build lasting resilience against the next inevitable crisis. The reopening is a relief—but not a resolution.

What do you think: are we witnessing the beginning of a permanent shift away from Hormuz-dependent energy flows, or will geopolitical tensions ensure it remains a permanent flashpoint? Share your perspective below—we’re listening.