Global oil markets are shifting as tanker operators redirect vessels toward the Middle East in anticipation of the Strait of Hormuz reopening. Following a U.S.-Iran diplomatic deal promising toll-free transit, logistics firms are positioning fleets to capture immediate demand, though insurers and industry leaders remain cautious regarding actual implementation.

The Logistics of a High-Stakes Pivot

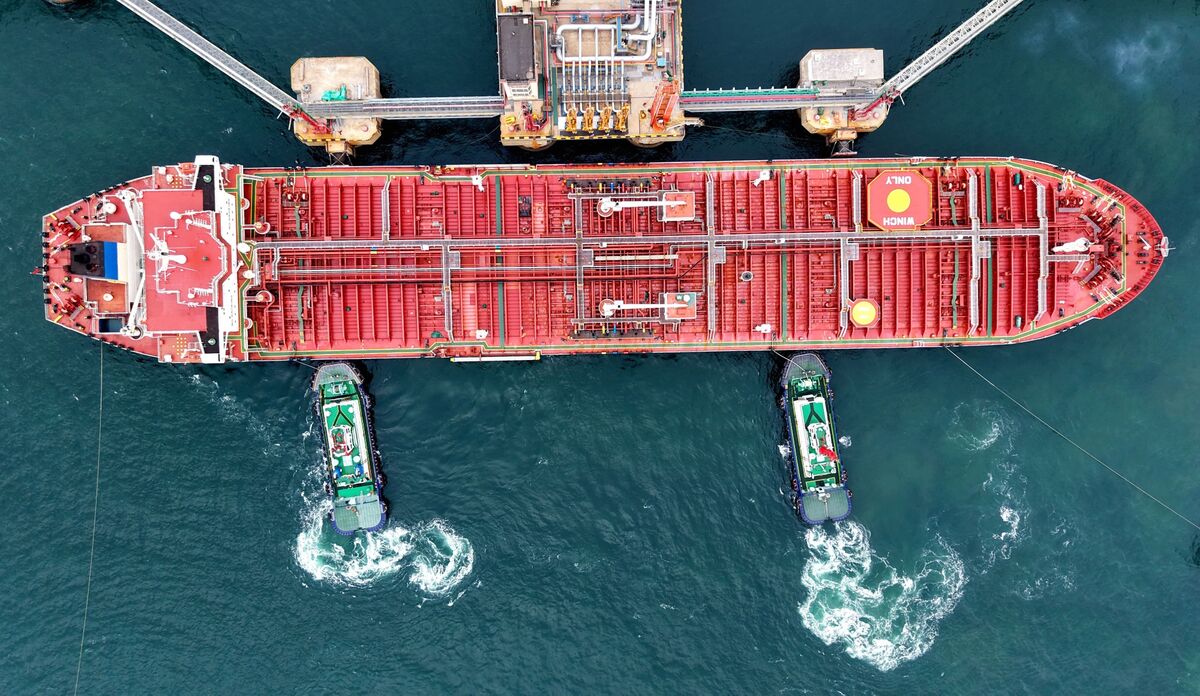

The maritime industry is currently witnessing a massive, coordinated U-turn of crude oil tankers. Earlier this week, satellite tracking data indicated that scores of vessels previously diverted around the Cape of Good Hope—a route that adds thousands of miles and significant fuel costs—have reversed course toward the Persian Gulf. This movement is a direct response to reports that the United States and Iran have reached a preliminary agreement to ensure the Strait of Hormuz remains toll-free and accessible for international commercial shipping.

But there is a catch. While ship owners are eager to reclaim the efficiency of the shorter route, the “rush” is as much about positioning as it is about optimism. By the time these vessels reach the mouth of the Strait, operators intend to be at the front of the queue if the waterway is declared safe for passage. However, as noted by the Financial Times, major tanker operators are demanding “material” proof of safety before committing their multi-million dollar assets to the chokepoint.

Why Transit Remains a Precarious Calculus

Restoring normal traffic is not merely a matter of political rhetoric. The Strait of Hormuz handles roughly one-fifth of the world’s daily oil consumption, making it the most critical energy artery on the planet. Even with a diplomatic framework in place, the physical and legal infrastructure of the region remains complex.

According to analysis from BBC News, three primary hurdles remain: the presence of naval mines or remnants of previous skirmishes, the lack of standardized maritime security protocols, and the reality that insurance premiums for “war risk” zones have not yet been adjusted downward. Until these factors align, the “reopening” remains a theoretical event rather than a verified reality.

"The market is pricing in a return to normalcy, but the technical reality of maritime security in a contested zone is not flipped by a single signature on a document," says Dr. Elena Rossi, a senior fellow at the Global Maritime Security Institute. "Until the underwriters see boots on the ground—or, more accurately, clear radar signatures of a de-escalated Iranian naval posture—the transit risk premium will stay elevated."

Comparative Risk and Regional Dynamics

To understand the current volatility, it is necessary to compare the incentives driving this rush against the structural risks that have defined the past year of shipping disruptions. The following data highlights the divergence between market optimism and operational reality.

| Factor | Pre-Agreement Status | Post-Agreement Expectation |

|---|---|---|

| Route Efficiency | Cape of Good Hope (Long) | Strait of Hormuz (Short) |

| Insurance Premiums | Prohibitive (War Risk) | Gradual Normalization |

| Operational Certainty | High Risk of Seizure | Diplomatic Guarantee |

| Supply Chain Impact | Severe Delays | Market Stabilization |

Geopolitical Ripple Effects

The implications of this shift extend far beyond the energy sector. For global investors, the reopening of the Strait serves as a bellwether for broader Middle Eastern stability. If the U.S.-Iran deal holds, it could signal a tactical cooling of tensions that have strained global supply chains since 2024. Conversely, any failure to maintain the “toll-free” status will likely trigger an immediate, sharp spike in crude prices, as the market is currently operating on very thin margins.

"The global macro-economy is currently held together by the thread of energy transit," observes Marcus Thorne, a lead trade economist at the Sovereign Risk Group. "If the Strait of Hormuz remains a bottleneck, the inflationary pressures we have seen in the manufacturing sector will not dissipate. The reopening is not just about oil; it is about the cost of goods for every consumer in the G7."

The Road Ahead: Verification Over Promises

As of this morning, the shipping industry is in a state of “wait and see.” While the U.S. government has expressed confidence in the deal’s durability, the actual movement of oil will be dictated by the behavior of regional actors on the ground. The next 72 hours will be critical; we expect to see whether the first tankers attempting to transit the Strait are met with safe passage or bureaucratic harassment.

For now, the tanker “U-turn” represents a fragile gamble. If the diplomatic path remains clear, we may see a stabilization of global fuel prices by the end of the month. If not, the industry may find itself in an even more precarious position than before, with assets stranded in a region that has proven increasingly unpredictable. How do you view the impact of this diplomatic shift on your own local energy costs? The situation is fluid, and we will continue to track the tanker movements as they reach the critical threshold of the Strait.