In July, the pension funds in the UBS sample achieved an average performance of 2.57% following deducting fees. Thus, the return since the beginning of the year is -6.60%.

After a first semester that many would prefer to forget, the month of July was a little less stormy. Inflation continued to be a major concern. The European Central Bank raised its key interest rate by an astonishing 0.50 percentage point to zero. The US Fed raised its own by another 0.75 percentage points in the final days of July. Markets saw it positively and a large portion of stocks and bonds ended the month up slightly. On the other hand, the earnings release season was good, which gave the markets an extra boost. However, in addition to price increases, the focus is increasingly on economic momentum: some leading economic indicators paint a less confident picture. Thus, the upside potential on the financial markets should be limited in the coming months.

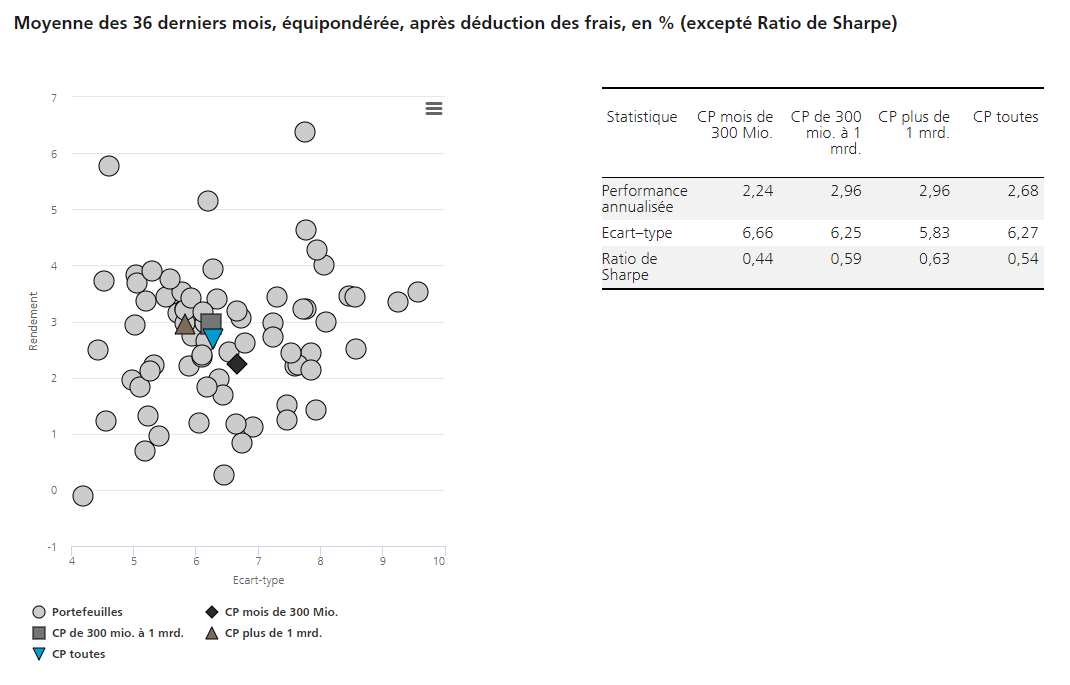

The performance range for all pension funds was 4.53% last month. The best result of 4.51% was obtained by a large pension fund with more than CHF 1 billion in assets under management, the worst with -0.02% comes from a small pension fund with less than CHF 300 million in assets under management. At 3.11%, the performance range was the lowest among large pension funds. It was 3.14% for medium-sized funds and 4.05% for small funds.

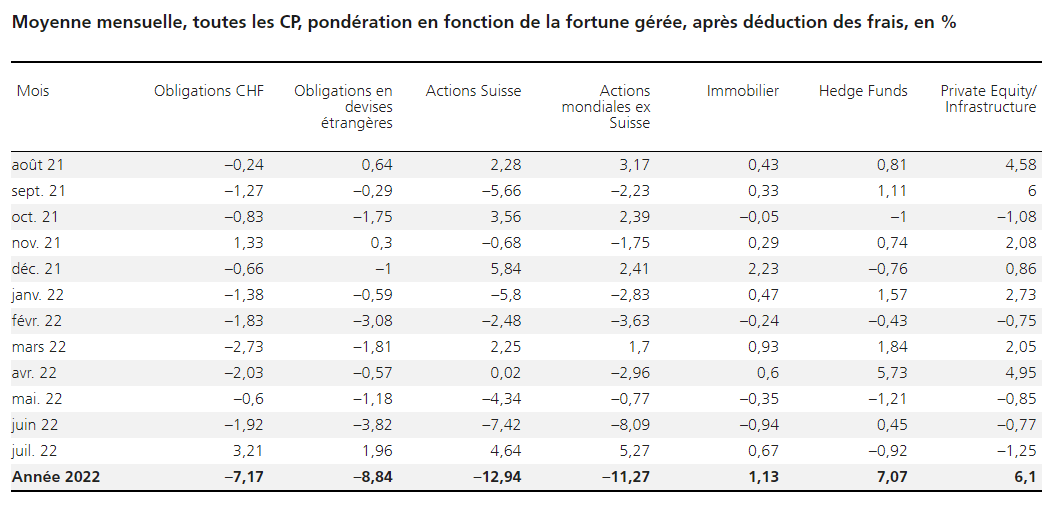

Bonds and equities closed the month in the green with 5.27% for international equities, 4.64% for Swiss equities, 3.21% for Swiss franc bonds and 1.96% for bonds in foreign currency. At 0.67%, real estate was slightly positive while hedge funds and private equity fell 0.92% and 1.25% respectively. However, alternative asset classes still show a positive year-to-date performance.

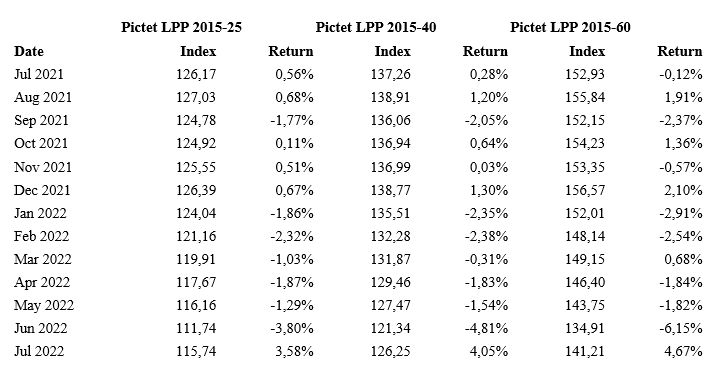

The Pictet LPP indices show us a positive performance for the month of July regardless of their weighting in the various asset classes. Given the very good performance of the equity markets, the index in which they are most represented (Pictet 60), posted the best score.

With an average of 0.54, the Sharpe ratio (over the last 36 months) was higher than the previous month (0.46). Large (0.63) and medium-sized (0.59) funds had higher risk-adjusted returns than smaller funds (0.44).

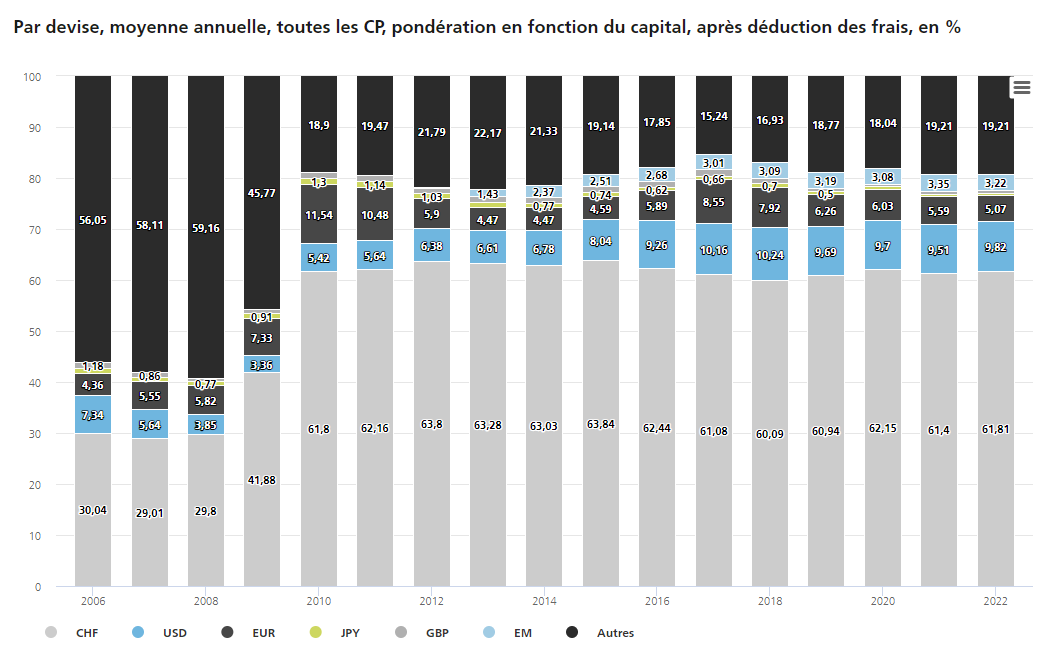

This last graph tells us that since 2010, Swiss pension funds have largely preferred the local currency for their investments. The weakness of the euro is obviously not unrelated to this situation.