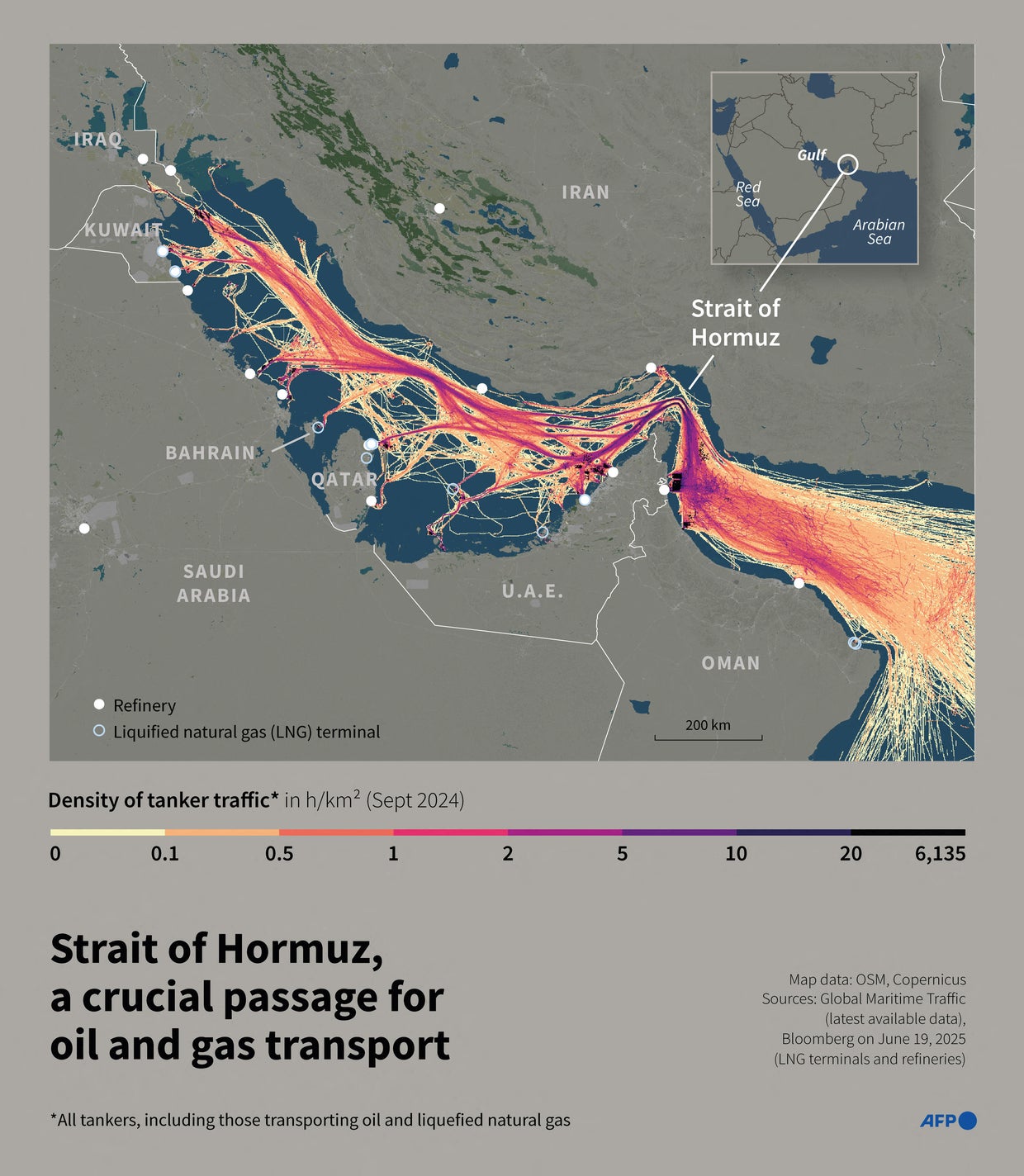

The Strait of Hormuz has remained effectively closed to commercial tanker traffic for 100 days as of June 14, 2026, following a surge in regional maritime hostilities. Despite the suspension of transit through this critical energy chokepoint—which historically facilitates the movement of approximately 20 to 21 million barrels of oil per day—global crude oil prices have remained range-bound, held in check by expanded domestic production in the Americas and strategic shifts in global supply chains.

Global Supply Resilience and Strategic Reserves

The primary factor preventing a sustained price spike is the increased output from non-OPEC producers, specifically in the United States and Brazil, which has offset the loss of Persian Gulf barrels. According to data from the International Energy Agency (IEA), global spare capacity remains at levels sufficient to cover the immediate shortfall created by the closure. The IEA’s Oil Market Report, released in May 2026, underscored that production gains in the U.S. Permian Basin and Brazil’s offshore Pre-Salt fields have effectively repositioned the global supply curve.

Government-mandated releases from strategic petroleum reserves in both the United States and the European Union have provided a liquidity buffer. These releases, initiated shortly after the initial transit disruptions in March, have kept physical markets supplied while refineries adjusted their input slates to favor crude grades from West Africa and the North Sea. The U.S. Department of Energy (DOE) confirmed in its April 2026 status update that reserves were deployed to prevent localized supply crunches in the Gulf Coast refining hub, which relies heavily on medium-sour crude imports that were temporarily disrupted by the maritime standoff.

Shifts in Market Sentiment and Demand Dynamics

Financial markets have largely priced in the closure of the Strait, moving from a state of acute crisis to one of long-term risk management. Analysts at Goldman Sachs noted in a June 10 research briefing that the market’s reaction has been muted because the “fear premium” associated with the closure was front-loaded during the first 30 days of the conflict. This phenomenon reflects historical precedents, such as the market reaction to geopolitical tensions in 2019 and 2022, where initial volatility eventually gave way to a “new normal” as trade routes adjusted.

Current demand data from China and India—the world’s largest importers of oil—shows a slower-than-anticipated growth rate. This cooling in demand has acted as a natural dampener on price volatility. As of mid-June 2026, Brent crude is trading within a $78 to $84 per barrel range, a figure that remains consistent with pricing trends observed throughout the first quarter of the year. Investors are balancing the geopolitical risk against macroeconomic indicators suggesting a deceleration in industrial output across Asia, which has effectively capped the potential for a supply-driven price breakout.

For more on this story, see Tankers Cross Strait of Hormuz as Oil Prices Drop Amid Easing Crisis.

The Role of Alternative Infrastructure

The existence of bypass pipelines has played a critical role in mitigating the impact of the waterway’s closure. The East-West Pipeline (Petroline) in Saudi Arabia, which connects the country’s eastern oil fields to the Red Sea, has been operating at near-maximum capacity. This pipeline serves as the primary artery for Saudi exports when the Strait is inaccessible, providing a direct route to the Red Sea and onwards to European and Western markets.

The ability to redirect a significant percentage of Gulf exports away from the Strait of Hormuz has transformed what would have been a catastrophic supply shock into a manageable, albeit expensive, logistical challenge.

— Sarah Varma, lead energy strategist at Energy Capital Research

This infrastructure, designed specifically for such scenarios, allows producers to export crude without navigating the bottleneck of the Strait. While the shipping costs associated with this route are higher due to the increased distance to primary Asian markets—requiring tankers to navigate around the Arabian Peninsula—the physical flow of oil has not halted entirely. Furthermore, the United Arab Emirates has utilized the Habshan-Fujairah pipeline, which bypasses the Strait entirely to reach storage and export terminals on the Gulf of Oman, providing an additional layer of logistical redundancy that was not available during previous regional crises in the late 20th century.

Future Outlook and Market Uncertainty

The situation remains delicate. While the 100-day mark has passed without a global price explosion, energy analysts warn that the system is operating without a safety net. Any further escalation in the conflict, particularly if it targets the overland pipeline infrastructure or secondary transit hubs, could quickly exhaust current supply buffers. The vulnerability of these fixed land-based assets remains a primary concern for risk managers, as these pipelines lack the mobility of maritime shipping.

Market participants are currently monitoring the June 2026 OPEC+ ministerial meeting, where members are expected to discuss potential production adjustments. According to official OPEC notices, the agenda focuses on balancing the current “supply-demand equilibrium” against the backdrop of the ongoing maritime closure. Whether the coalition chooses to maintain current output levels or increase production to further stabilize prices remains the central question for the remainder of the summer. As of today, the market appears to be betting on the status quo, prioritizing supply-side stability over the geopolitical risks inherent in the region. The outcome of the ministerial meeting will likely dictate the price floor for the third quarter, as traders await clarity on whether the group intends to compensate for the logistical constraints imposed by the ongoing closure.