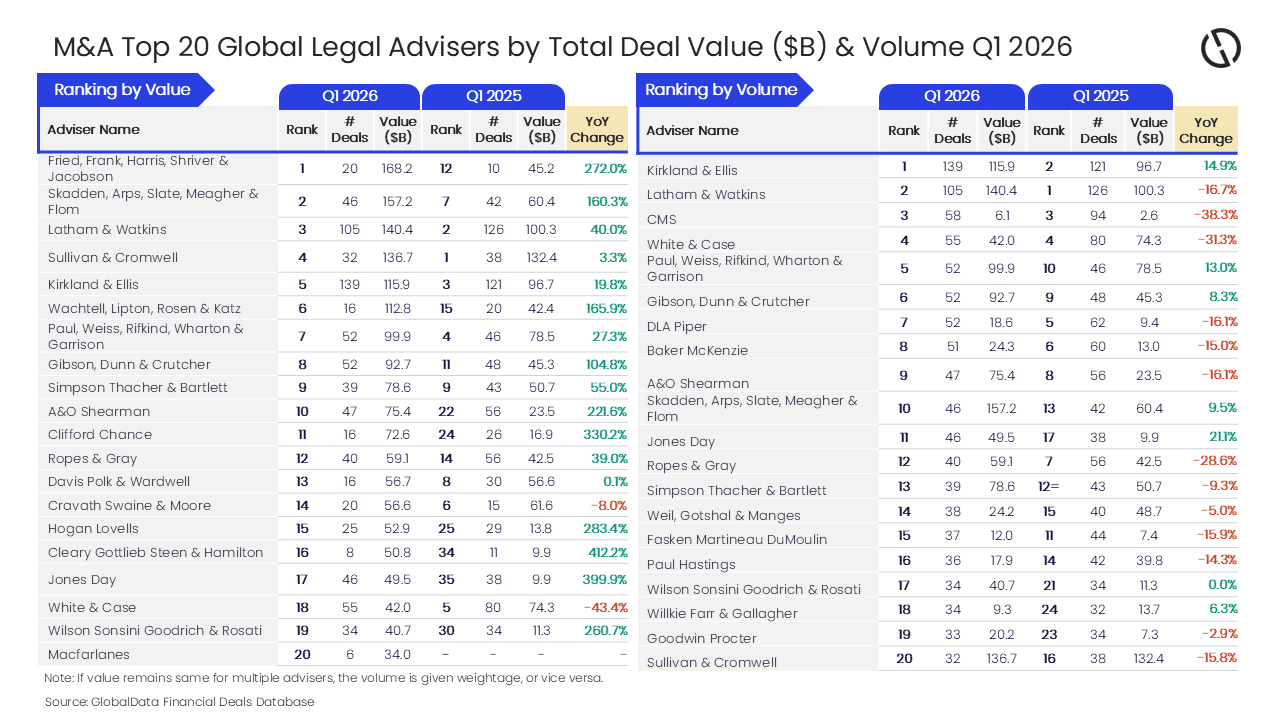

Fried, Frank, Harris, Shriver & Jacobson and Kirkland & Ellis led the Q1 2026 M&A legal adviser rankings in both deal value and volume. This dominance indicates a strategic pivot toward large-scale corporate consolidations and private equity exits, driven by stabilizing global interest rates and aggressive sector integration.

The legal leaderboard is rarely about the lawyers; it is a heatmap of where the world’s largest pools of capital are flowing. When firms like Kirkland & Ellis and Fried Frank dominate the rankings, it signals a specific market regime. In this case, the Q1 data confirms that the “wait-and-see” posture of 2024 and 2025 has been replaced by a rush to consolidate market share. This is not a random surge, but a calculated response to the current macroeconomic environment where the cost of debt has reached a predictable plateau, allowing for more accurate discounted cash flow (DCF) modeling.

The Bottom Line

- Private Equity Resurgence: Kirkland & Ellis’s volume lead suggests a return to aggressive leveraged buyouts (LBOs) as **Blackstone (NYSE: BX)** and **KKR (NYSE: KKR)** deploy significant dry powder.

- Strategic De-risking: The preference for top-tier legal advisers reflects a market terrified of antitrust litigation; firms are paying a premium for “safe” execution to avoid FTC roadblocks.

- Sector Concentration: Deal value is being driven by a handful of massive “mega-mergers” in the AI infrastructure and energy transition sectors rather than a broad market recovery.

The Private Equity Pivot: Why Kirkland’s Volume Matters

To understand why Kirkland & Ellis is topping the volume charts, one must look at the nature of the deals. Kirkland is the primary engine for the private equity (PE) world. Their lead suggests that the “deal gap” has finally closed. For the past 24 months, the disparity between buyer and seller expectations on valuation was too wide to bridge. Now, that gap is narrowing.

But there is a catch. The volume is not coming from mid-market deals. Instead, we are seeing a concentration of activity in “take-private” transactions. PE firms are targeting public companies whose stock prices have failed to keep pace with their intrinsic value, leveraging the current stability in the credit markets to fund these acquisitions. Here is the math: with interest rates stabilizing, the cost of financing a $10 billion acquisition is now predictable, making the internal rate of return (IRR) calculations viable again.

This trend is heavily influenced by the current guidance from the Federal Reserve. As the market prices in a neutral rate environment, the leverage ratios that were considered “toxic” in 2023 are once again being utilized to amplify returns. This puts immense pressure on mid-cap companies that lack the scale to defend against hostile takeovers.

Antitrust Friction and the “Safe Harbor” Legal Strategy

While Kirkland handles the volume, Fried Frank’s presence at the top of the value rankings points to a different phenomenon: the mega-merger. When a deal’s value enters the tens of billions, the primary risk is no longer financial—it is regulatory. The relationship between the Federal Trade Commission (FTC) and the Department of Justice (DOJ) has become the single greatest variable in deal closure.

Why does this favor the top-ranked firms? Because the “cost of failure” for a blocked merger is now catastrophic. Between break-up fees and the public signal of a failed strategy, CEOs are opting for legal advisers with the deepest benches of former regulatory officials. We are seeing a shift toward “defensive lawyering,” where the legal strategy is designed to preemptively appease regulators through surgical divestitures before the deal is even announced.

“The current M&A landscape is defined by a paradox: capital is plentiful, but the path to closing is narrower than it has been in a decade. The winners are not those who find the best deals, but those who can navigate the regulatory gauntlet without losing the deal’s original synergy.”

This environment creates a virtuous cycle for the top firms. The more they win, the more they understand the current regulatory “mood,” which in turn attracts more high-value mandates from entities like **Goldman Sachs (NYSE: GS)** and **JPMorgan Chase (NYSE: JPM)**.

The Valuation Gap: Bridging the Divide in 2026

The Q1 2026 data reveals a stark contrast in how different sectors are being valued. In the AI and semiconductor space, companies like **Nvidia (NASDAQ: NVDA)** have set a valuation ceiling that is almost impossible for others to reach. This has led to a “clustering” effect where smaller AI firms are being absorbed by legacy tech giants to avoid the risk of obsolescence.

But the balance sheet tells a different story in the industrial sector. There, we are seeing a focus on “accretive” acquisitions—deals that immediately increase earnings per share (EPS). The following table illustrates the shift in deal dynamics from the previous year.

| Metric | Q1 2025 (Actual) | Q1 2026 (Projected/Current) | Variance (%) |

|---|---|---|---|

| Avg. Deal Value (Top 10) | $4.2 Billion | $6.8 Billion | +61.9% |

| PE-Backed Volume | 142 Deals | 218 Deals | +53.5% |

| Regulatory Block Rate | 12.4% | 18.1% | +45.9% |

| Avg. EBITDA Multiple | 9.2x | 11.4x | +23.9% |

The increase in the average EBITDA multiple suggests that buyers are once again paying a premium for growth. However, this premium is heavily skewed toward companies with proprietary data sets or critical infrastructure, while “generalist” software firms are seeing their multiples compress. This bifurcation is exactly why legal advisers are focusing on rigorous due diligence to ensure that the “synergy” promised in the pitch deck is actually present in the SEC filings.

Strategic Implications for Mid-Cap Competitors

For the mid-cap business owner, the dominance of these legal giants is a warning sign. As the top firms facilitate the consolidation of the “big players,” the middle of the market is being hollowed out. We are entering a phase of “forced consolidation,” where companies must either scale up rapidly or become a target for the PE firms represented by Kirkland & Ellis.

The result? A tighter labor market for specialized executives and a higher barrier to entry for new competitors. When the top legal firms are this busy, it means the “big fish” are eating the “medium fish” to protect their moat. The strategic imperative for 2026 is clear: optimize the balance sheet for either a high-value exit or a defensive posture. Waiting for the market to “settle” is no longer a viable strategy; the market has settled, and the consolidation phase has begun.

Looking ahead to the close of Q2, expect the trend to accelerate. As more companies report their annual earnings, the disparity between the “AI-winners” and the “legacy-laggards” will become even more pronounced, fueling a second wave of strategic acquisitions. The legal rankings will likely remain top-heavy, as the complexity of these deals precludes the use of smaller, boutique firms.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.