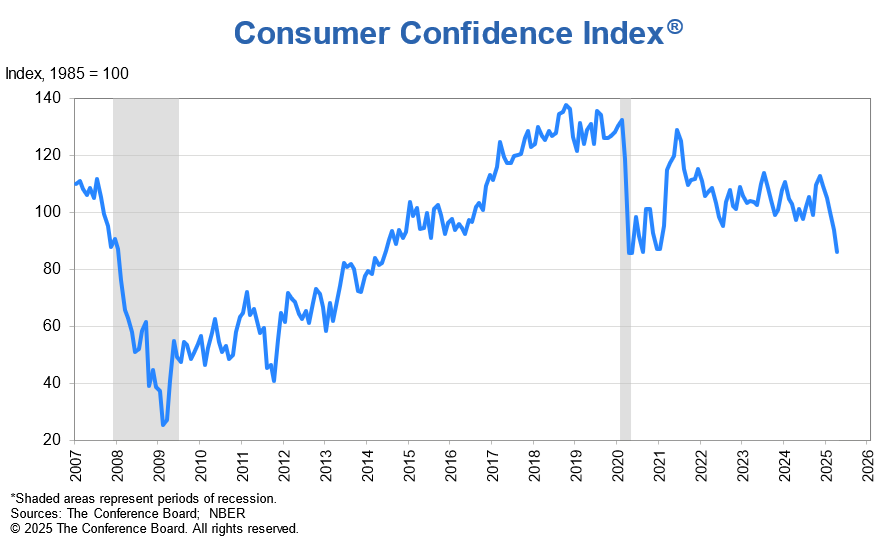

U.S. Consumer confidence collapsed to its lowest level since 1978 in April 2026, driven by surging fuel prices and inflation fears as the Iran conflict entered its third month, according to the University of Michigan’s Surveys of Consumers, with the index falling to 58.2 from 64.7 in March, reflecting heightened anxiety over purchasing power and economic stability ahead of the Federal Reserve’s May policy decision.

The Bottom Line

- The Michigan Consumer Sentiment Index dropped 10.0 points month-over-month, its steepest decline since the 2008 financial crisis.

- Real disposable income growth slowed to 0.8% YoY in Q1 2026, down from 2.1% in Q4 2025, per Bureau of Economic Analysis data.

- Energy sector stocks outperformed, with **ExxonMobil (NYSE: XOM)** rising 4.3% and **Chevron (NYSE: CVX)** gaining 3.8% intraday on April 24, while consumer discretionary shares fell broadly.

Fuel Inflation Triggers Broad-Based Consumer Retreat

The sharp decline in consumer confidence was primarily fueled by a 22.6% month-over-month increase in regular gasoline prices to $4.89 per gallon nationally, according to the U.S. Energy Information Administration (EIA), as refining disruptions and geopolitical risk premiums amplified costs. This surge pushed transportation expenses to consume 12.4% of average household budgets in April, up from 9.1% in March, squeezing non-essential spending capacity. The University of Michigan survey revealed that 68% of respondents cited fuel costs as a “major financial strain,” the highest share since tracking began in 1980.

Retail and Auto Sectors Face Immediate Demand Pressure

Consumer discretionary retailers reported early signs of demand softening, with **Walmart (NYSE: WMT)** noting a 3.1% decline in same-store sales for non-food categories in its April 22 trading update, while **Target (NYSE: TGT)** reported a 2.8% drop in home goods sales. Auto manufacturers also felt the impact, as **Ford (NYSE: F)** saw new vehicle orders fall 5.2% week-over-week in mid-April, per Cox Automotive data, with incentives rising to 8.9% of transaction value to offset buyer hesitation. These trends signal a potential shift toward essential goods and delayed big-ticket purchases.

Inflation Expectations Rise, Complicating Fed Policy

One-year-ahead inflation expectations jumped to 4.9% in April from 4.2% in March, the highest since 2023, while five-year expectations held steady at 2.8%, indicating persistent near-term price anxiety. This divergence complicates the Federal Reserve’s balancing act, as policymakers weigh transitory energy shocks against entrenched services inflation. In a Bloomberg interview on April 23, former Minneapolis Fed President Neel Kashkari stated,

“We cannot ignore that households are now pricing in sustained pain at the pump, which risks becoming embedded in wage negotiations and rent cycles if relief does not come by summer.”

Corporate Earnings Guidance Begins to Reflect Caution

Several major corporations adjusted forward guidance amid weakening consumer sentiment. **Procter & Gamble (NYSE: PG)** lowered its FY 2026 organic sales growth forecast to 2.0–3.0% from 3.0–4.0%, citing “reduced elasticity in price-sensitive categories” during its April 20 earnings call. Similarly, **Coca-Cola (NYSE: KO)** noted a 1.5 percentage point headwind to volume growth from consumer trade-down effects in its Q1 report. These revisions contributed to a 1.9% decline in the S&P 500 Consumer Discretionary Select Sector SPDR Fund (XLY) on April 24, while the Consumer Staples Select Sector SPDR Fund (XLP) rose 0.7%, reflecting a classic defensive rotation.

| Indicator | March 2026 | April 2026 | Change |

|---|---|---|---|

| U. Of Michigan Consumer Sentiment Index | 64.7 | 58.2 | -10.0 |

| Regular Gasoline Price ($/gal) | $3.99 | $4.89 | +22.6% |

| 1-Year Inflation Expectation | 4.2% | 4.9% | +0.7 pts |

| Real Disposable Income (YoY) | 2.1% (Q4 2025) | 0.8% (Q1 2026) | -1.3 pts |

Labor Market Resilience Offers Limited Offset

Despite weakening sentiment, the labor market remains a buffer, with initial jobless claims at 218,000 for the week ending April 19, near historic lows, and hourly wages rising 4.1% YoY in March, per the BLS. However, the Conference Board’s Labor Market Index showed a 0.6-point decline in April, suggesting early signs of hiring hesitation in rate-sensitive sectors. Economist Claudia Sahm, former Federal Reserve staffer, warned in a Reuters interview on April 22:

“Consumers can absorb higher fuel costs if they feel secure in their jobs, but when confidence cracks, even strong employment data can’t prevent a pullback in spending — especially if they start saving for uncertainty.”

Market Implications: Stagflation Risks Resurface

The convergence of falling confidence, rising inflation expectations, and stagnant real income growth raises concerns about a stagflationary impulse, reminiscent of the 1970s–80s era that the Michigan index was designed to capture. While GDP growth remains positive at 1.8% annualized in Q1 2026, the Atlanta Fed’s GDPNow model revised Q2 estimates down to 1.2% from 1.6% on April 23, citing weaker consumption forecasts. Equity markets reacted accordingly, with the S&P 500 down 0.9% on April 24, but sector rotation favored energy and utilities, while technology and consumer discretionary lagged. The 10-year Treasury yield held at 4.35%, reflecting mixed signals on future rate cuts.

Looking ahead, the next Michigan survey in May will be critical to determine whether this confidence drop is a transient shock or the start of a sustained downturn. If fuel prices remain above $4.50/gal and inflation expectations fail to retreat, Q2 consumer spending could contract by 0.5–1.0%, posing material risk to full-year GDP growth. For now, businesses are advised to tighten inventory controls, prioritize value-tier offerings, and monitor leading indicators like retail card spending and durable goods orders for early confirmation of a broader pullback.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.