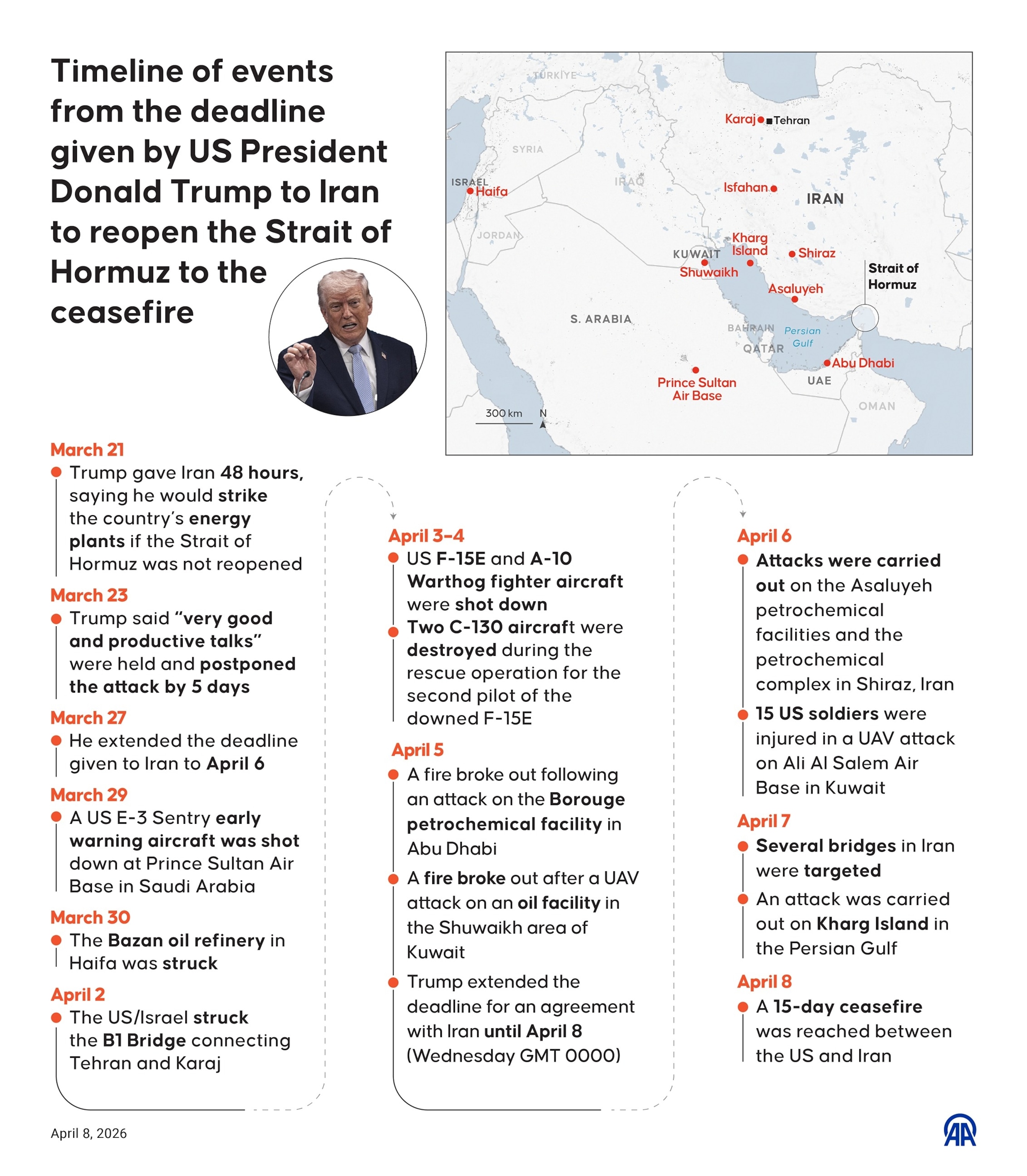

The U.S. And Iran are negotiating a fragile ceasefire extension and potential reopening of the Strait of Hormuz, a critical maritime chokepoint through which 20% of global oil trade passes. Earlier this week, indirect talks in Oman revealed progress on curbing Houthi attacks in the Red Sea while easing Iranian-backed militia pressure in Iraq and Syria. Here’s why this matters: A collapse of the deal could trigger a regional oil shock, destabilize global supply chains, and force Western powers to choose between sanctions relief and military escalation. But there is a catch—Tehran’s leverage depends on whether Washington can deliver sanctions relief before the next U.S. Election cycle. The stakes? Nothing less than the future of the Middle East’s energy arteries and the geopolitical balance between Washington, Riyadh, and Beijing.

The Nut Graf: Why the Strait of Hormuz Is the World’s Most Dangerous Chokepoint

The Strait of Hormuz isn’t just a waterway—it’s the world’s most strategically vulnerable economic artery. Imagine a 21-mile-wide bottleneck where 17 million barrels of oil pass daily, supplying China, India, and Europe. In 2019, when tensions between the U.S. And Iran flared, oil prices spiked by 20% in weeks. Today, with global demand recovering post-pandemic and Russia’s oil exports under sanctions, any disruption here would send shockwaves through energy markets. Here’s the kicker: Iran’s Islamic Revolutionary Guard Corps (IRGC) has repeatedly threatened to block the strait if sanctions aren’t lifted. The current ceasefire, brokered by China and Oman, is a temporary bandage—but it’s holding only because both sides fear the alternative.

How the U.S.-Iran Stalemate Reshapes Global Alliances

This isn’t just about oil. It’s about who controls the narrative in the Middle East. The U.S. Is caught between two imperatives: preventing a regional war that could destabilize allies like Israel and Saudi Arabia, and avoiding a diplomatic win for Iran that could embolden Hezbollah and the Houthis. Meanwhile, China—already deepening ties with Tehran through oil-for-infrastructure deals—stands to benefit from any U.S. Retreat. Here’s the leverage breakdown:

| Actor | Key Demand | Potential Concession | Wildcard Factor |

|---|---|---|---|

| United States | Ceasefire extension, Houthi de-escalation | Limited sanctions relief (e.g., oil waivers, SWIFT re-entry) | 2024 election cycle—Biden administration may avoid major deals |

| Iran | Full sanctions rollback, Strait of Hormuz security guarantees | Reduced Houthi attacks, indirect talks with Saudi Arabia | Domestic protests over economic stagnation could derail negotiations |

| China | Stable oil supply, Iranian market access | Diplomatic cover for U.S.-Iran détente | Beijing’s “no limits” partnership with Moscow complicates U.S. Strategy |

| Saudi Arabia | Houthi containment, U.S. Security guarantees | Oil production increases to offset Iranian disruptions | Crown Prince Mohammed bin Salman’s re-election gambit depends on stability |

But here’s the geopolitical twist: Iran’s recent overtures to Saudi Arabia—including indirect talks in Baghdad—suggest Tehran may prioritize regional stability over maximalist demands. As one Middle East analyst told Archyde, “Iran knows it can’t win a war with Israel or the U.S., but it can force concessions through asymmetric pressure. The question is whether Washington is willing to pay the price before the election.”

“The Strait of Hormuz is the ultimate geopolitical pressure point. If Iran closes it, the global economy doesn’t just slow down—it seizes up. And the U.S. Has no good military option to reopen it without risking a wider conflict.”

The Economic Domino Effect: How Oil Markets and Supply Chains Hang in the Balance

Let’s talk numbers. The Strait of Hormuz accounts for 40% of global seaborne oil exports. A disruption would force tankers to reroute around the Cape of Good Hope, adding $10–$15 to the cost of every barrel. For India, which imports 80% of its oil through Hormuz, the impact would be catastrophic—pushing inflation higher and weakening the rupee. Meanwhile, European refiners, already grappling with Russia’s oil price cap, would face a double whammy: higher Brent crude prices and potential Iranian retaliation for supporting Israel.

Here’s the ripple effect:

- Energy Markets: Brent crude could spike by 15–25% if attacks resume, triggering a global reflationary shock. Bloomberg’s commodity analysts warn that even a temporary closure would send signals comparable to the 1973 oil crisis.

- Shipping Costs: The Baltic Dry Index (a freight market benchmark) would surge, increasing costs for grain and container shipments from the Black Sea to Asia. Baltic Exchange data shows that Red Sea disruptions have already added $1.2 billion to global shipping costs this year.

- Currency Wars: The Swiss National Bank and others may intervene again to prop up the franc and yen, while emerging markets like Turkey and Argentina could face capital flight. SNB’s latest forex reserves report indicates preparations for another round of intervention.

But the real wild card? Iran’s ability to weaponize its oil exports. Tehran has already hinted it could redirect tankers to China if sanctions are eased—effectively bypassing U.S. Sanctions and undercutting OPEC+ production cuts. This would directly threaten Saudi Arabia’s market share and force Riyadh to either match output or risk losing influence.

The Security Paradox: Why Military Escalation Is the Last Option

Here’s the uncomfortable truth: Neither the U.S. Nor Iran wants a direct war. But the proxy battles—Houthi attacks on commercial ships, IRGC-backed militia raids in Iraq, and Israeli airstrikes in Syria—are proxy wars by another name. The current ceasefire is held together by three fragile pillars:

- Chinese Mediation: Beijing’s role as a neutral broker is critical. Without Chinese pressure, Iran would have little incentive to negotiate.

- Regional Fatigue: Saudi Arabia and the UAE are exhausted by years of Houthi attacks and don’t want another war. Recent Arab League statements reflect growing impatience with U.S. Military posturing.

- Domestic Constraints: U.S. Hawks in Congress are pushing for a harder line, but Biden’s administration knows a military strike would trigger Iranian retaliation—possibly targeting U.S. Bases in the Gulf.

Yet the biggest risk isn’t an all-out war—it’s miscalculation. Earlier this month, a U.S. Drone strike in Syria killed two IRGC officers, prompting Tehran to threaten “harsh retaliation.” If either side crosses a red line, the ceasefire could unravel in days. As Ambassador Richard Nephew, former U.S. Sanctions negotiator, warns:

“The danger isn’t that Iran will start a war tomorrow. It’s that someone—probably an Iranian general or a U.S. Admiral—will make a decision in the heat of the moment that spirals out of control. That’s how regional wars start.”

The Long Game: What Happens If the Deal Fails?

Scenario planning is essential here. If negotiations collapse:

- Short-Term (0–3 months): Houthi attacks on Red Sea shipping resume, forcing reroutes and a 10–15% spike in oil prices. The U.S. May deploy additional naval assets to the Gulf, but without a clear mandate.

- Medium-Term (3–12 months): Iran accelerates uranium enrichment, pushing closer to a nuclear breakout capability. Saudi Arabia and Israel ramp up covert operations in Syria and Lebanon, creating a new proxy war theater.

- Long-Term (1–5 years): China and Russia deepen their energy partnership with Iran, creating a de facto OPEC+ alternative that undermines Western sanctions. The U.S. Loses leverage in the Gulf, forcing a pivot toward India and Southeast Asia for energy security.

The most likely outcome? A stopgap deal that extends the ceasefire for 6–12 months while keeping the Strait of Hormuz open—but with no real sanctions relief. This would buy time for the next U.S. Administration to decide whether to engage or escalate. The problem? Time is running out. As one Gulf diplomat put it, “We’re playing a game of chicken with a nuclear-powered truck.”

The Takeaway: What’s Next for Global Investors and Policymakers?

Here’s the bottom line: This isn’t just a Middle East story—it’s a global risk assessment. For investors, the key metrics to watch are:

- Brent Crude Futures: Monitor the spread between Brent and WTI as a proxy for Hormuz-related disruptions.

- Iranian Oil Exports: Track tanker movements via Kpler’s maritime data for signs of Iranian rerouting.

- U.S. Sanctions Waivers: Any easing of restrictions on Iranian oil would be a major market mover.

For policymakers, the choice is stark: Double down on military deterrence and risk a wider conflict, or engage in diplomacy and risk appearing weak. The smart money is on a messy compromise—one that keeps the lights on but doesn’t solve the underlying problems. As for the rest of us? Buckle up. The Strait of Hormuz is about to test the limits of global patience.

Now, here’s the question for you: If Iran and the U.S. Can’t agree on a deal, who do you think will blink first—and what happens when they do?