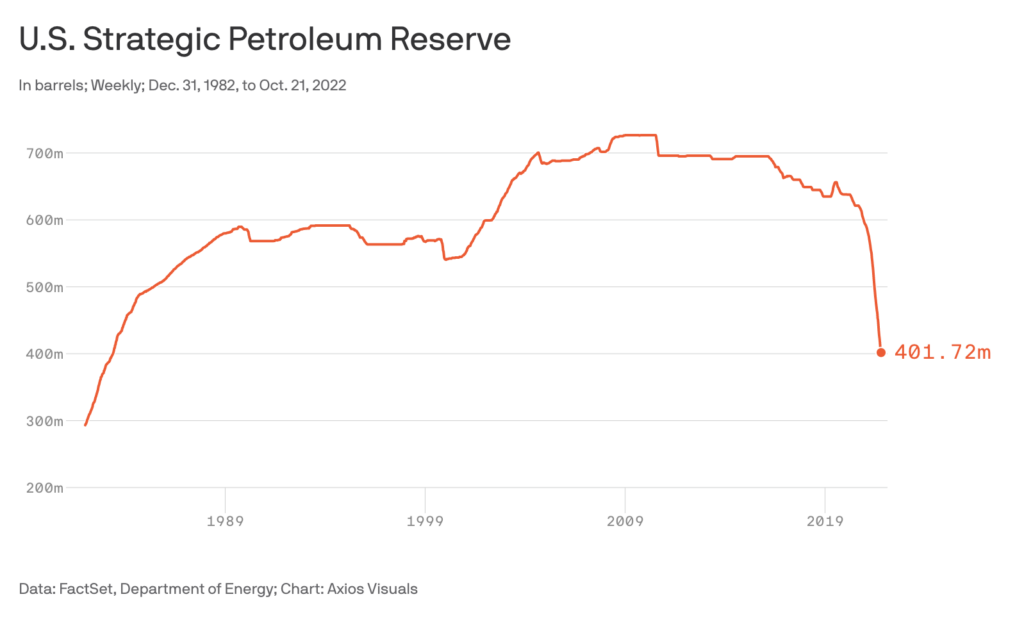

The U.S. Department of Energy announced plans, effective immediately, to loan up to 92.5 million barrels of crude oil from the Strategic Petroleum Reserve (SPR) to six companies. This move, designed to fulfill obligations under the International Energy Agency (IEA) agreement, comes as global energy markets remain volatile. Bids were due May 4th, and the loans aim to replenish the SPR after previous drawdowns. The initiative seeks to stabilize oil prices and ensure energy security.

The decision to utilize a loan mechanism, rather than a direct sale, is a critical nuance often overlooked. It suggests the Biden administration intends to fully restock the SPR once market conditions allow, signaling a belief in a future price environment where repurchase is economically feasible. This contrasts with outright sales, which would permanently diminish the nation’s emergency oil supply. But the market’s reaction, or lack thereof, reveals a deeper skepticism about the long-term efficacy of this strategy.

The Bottom Line

- The SPR loan program is a short-term fix, unlikely to significantly alter global oil supply dynamics.

- The loan structure implies a belief in future price declines, creating a potential repurchase risk for taxpayers.

- **ExxonMobil (NYSE: XOM)** and **Chevron (NYSE: CVX)** are positioned to benefit most from the program, potentially increasing their Q2 revenue.

The IEA’s Role and the War Premium

The impetus for this action stems from a commitment made to the IEA following the energy crisis triggered by the war in Ukraine. As IEA Executive Director Fatih Birol noted, the conflict unleashed the biggest energy crisis in history, disrupting supply chains and driving up prices. The IEA’s reports detail the severity of the disruption and the need for coordinated action among member states.

However, the effectiveness of SPR releases – and now loans – in curbing price volatility is increasingly questioned. While releases can provide temporary relief, they don’t address the underlying geopolitical factors driving prices. The market appears to have largely priced in the SPR’s potential interventions. The initial response to the loan announcement was muted, with West Texas Intermediate (WTI) crude futures showing a modest 0.8% increase on May 1st.

The Loan Structure: A Closer Seem

Here is the math. The loans will be structured with a repayment period of up to one year, with companies paying interest rates tied to the prevailing LIBOR (or its successor, SOFR) plus a premium. The companies selected – **ExxonMobil (NYSE: XOM)**, **Chevron (NYSE: CVX)**, **Marathon Petroleum (NYSE: MPC)**, **Phillips 66 (NYSE: PSX)**, **Valero Energy (NYSE: VLO)**, and **Plains All American Pipeline (NYSE: PAA)** – will be required to maintain the oil in storage and make it available for drawdown if needed.

But the balance sheet tells a different story. These companies aren’t reliant on the SPR for operational needs. They’re already flush with capital and have access to traditional financing. The loans essentially provide them with a low-cost financing option to increase their inventory, potentially positioning them to profit from future price fluctuations. This raises questions about whether the program is truly serving its intended purpose of bolstering energy security for consumers.

Impact on Competitors and Refining Margins

The loan program will likely exacerbate the competitive advantage of the selected companies. **ExxonMobil (NYSE: XOM)**, for example, reported Q1 2026 earnings of $11.4 billion, a 12% increase year-over-year. Their latest earnings report highlights strong refining margins, which are likely to be further bolstered by access to low-cost crude via the SPR loan. This could put pressure on smaller, independent refiners who lack the same access to capital and government programs.

“The SPR loan program is a classic example of regulatory capture,” says Dr. Emily Carter, a senior energy economist at the Peterson Institute for International Economics.

“It disproportionately benefits large, politically connected companies while doing little to address the fundamental challenges facing the energy market.”

Financial Performance Comparison (Q1 2026)

| Company | Ticker | Revenue (USD Billions) | Net Income (USD Billions) | Refining Margin (USD/Barrel) |

|---|---|---|---|---|

| ExxonMobil | NYSE: XOM | 85.6 | 11.4 | 12.5 |

| Chevron | NYSE: CVX | 78.2 | 9.8 | 11.8 |

| Marathon Petroleum | NYSE: MPC | 52.1 | 3.2 | 9.5 |

| Valero Energy | NYSE: VLO | 48.7 | 2.8 | 10.2 |

The Repurchase Risk and Future Trajectory

The success of this program hinges on the U.S. Government’s ability to repurchase the loaned oil at a favorable price. If prices rise significantly, the repurchase could prove costly to taxpayers. This is a risk that analysts at Goldman Sachs have highlighted in recent research notes, estimating a potential cost of up to $5 billion if WTI prices exceed $90 per barrel during the repurchase window.

Looking ahead, the market’s focus will shift to the upcoming OPEC+ meetings and the trajectory of global demand. The IEA forecasts global oil demand to grow by 1.1 million barrels per day in 2026, driven primarily by emerging economies. However, the rise of electric vehicles and increasing energy efficiency measures could dampen demand growth in the long term. The SPR loan program, while providing a temporary buffer, is unlikely to fundamentally alter these long-term trends. The program’s true impact will be measured not by its immediate effect on prices, but by the cost and efficiency of the eventual repurchase.

The current strategy appears to be a calculated gamble, predicated on a belief that current price levels represent a temporary peak. Whether that gamble pays off remains to be seen, but the market’s initial reaction suggests a healthy dose of skepticism.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*