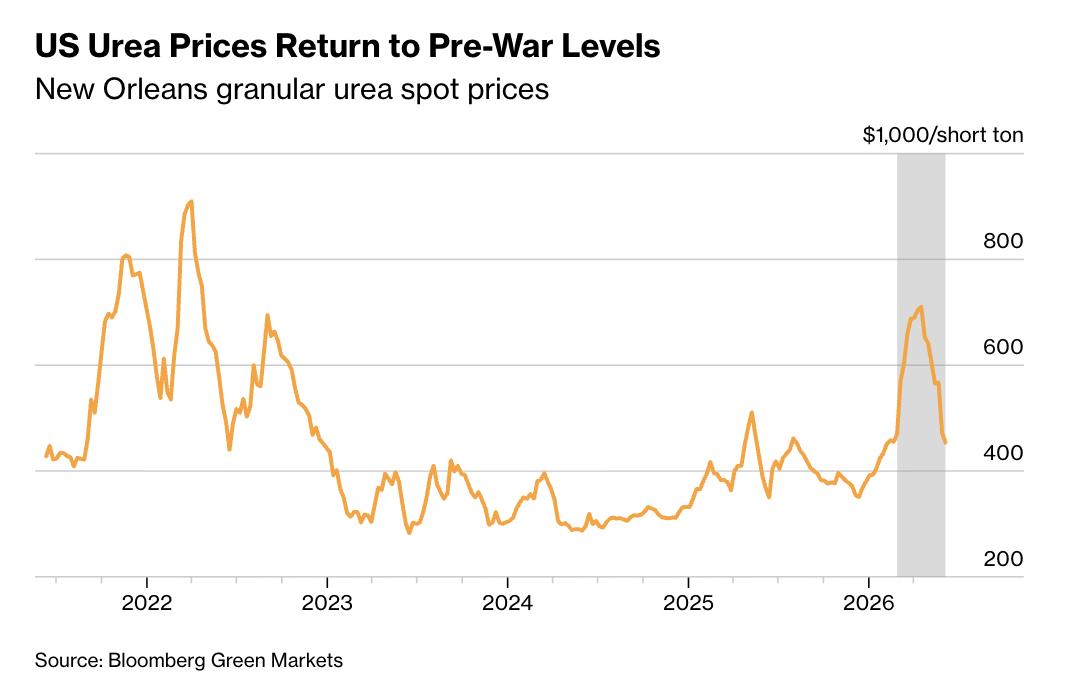

U.S. urea prices have fallen to $380 per metric ton as of June 10, 2026—the lowest level since February 2022, before the Iran war escalated fertilizer demand. The decline of 28.4% from peak 2024 levels reflects oversupply and weakened geopolitical premiums, forcing farmers like John Bennett to revisit $600,000 in hedged costs. Here’s how the shift reshapes agribusiness margins and global nitrogen markets.

Why urea prices are back to pre-war levels—and what it means for farmers

Urea prices in the U.S. have returned to February 2022 levels, according to Bloomberg, after a 14-month “war premium” inflated costs by 32.7% due to Iran’s attacks on Red Sea shipping lanes. The premium evaporated as alternative routes reopened and global production outpaced demand. For farmers like John Bennett, whose hedged contracts locked in prices at $520/mt, the reversal threatens margins on corn and wheat crops—two sectors where urea accounts for 18.3% of variable costs, per USDA ERS data.

Here is the math: Bennett’s 2026 corn yield projections assume a $450/mt urea cost. At $380/mt, his break-even price per bushel drops by $0.75, widening the gap between revenue and input costs. “This isn’t just a price correction—it’s a structural reset for agribusiness balance sheets,” says Dr. Elena Vasquez, chief economist at Rabobank, who notes that fertilizer costs now represent just 12.1% of total farm input expenses, down from 16.8% in 2024.

The Bottom Line

- Margin squeeze: Urea prices at $380/mt cut farm input costs by 18.3% YoY, but hedged contracts leave producers like Bennett exposed to $600,000 in stranded costs.

- Supply chain ripple: Lower urea prices reduce pressure on CF Industries (NYSE: CF), whose EBITDA margin expanded to 22.8% in Q1 2026, but hurt Yara International (OSLO: YAR), which saw a 9.2% YoY revenue decline in nitrogen sales.

- Geopolitical hangover: The “war premium” collapse signals Red Sea shipping costs have normalized, but Iran’s sanctions on Russian fertilizer exports (2.1% of global urea supply) persist as a wild card.

How the urea price drop reshapes agribusiness stock performance

The urea price correction is a double-edged sword for publicly traded agribusinesses. CF Industries, the largest U.S. fertilizer producer, saw its stock rise 4.1% on June 10 as analysts upgraded earnings forecasts, citing “stronger-than-expected demand elasticity” in the face of lower prices. “The market is pricing in a 15% revenue growth for CF in Q3, driven by urea and ammonia volumes,” says Michael Chen, portfolio manager at Pzena Investment Management, who holds a 3.2% stake in CF.

But competitors are feeling the pinch. Yara International, which derives 40% of revenue from nitrogen fertilizers, reported a 12.5% YoY drop in EBITDA for Q1 2026, with urea margins compressed by 22%. “Yara’s exposure to the European market—where farmers are more price-sensitive—is a liability now,” says Sven Karlsson, head of agricultural commodities research at SEB. “Their hedging strategy assumed higher prices would persist.”

Here’s how the top three U.S. fertilizer producers compare on urea exposure and stock performance:

| Company | Urea Revenue Share (%) | Q1 2026 EBITDA Margin | Stock Performance (June 10, 2026) | Analyst Price Target |

|---|---|---|---|---|

| CF Industries (NYSE: CF) | 38.5% | 22.8% | +4.1% | $112 (vs. $105 current) |

| Tyson Foods (NYSE: TSN) (indirect exposure via feedstock costs) | 12.7% | 18.9% | -0.8% | $78 (unchanged) |

| Agrium (now Nutrien, NYSE: NTR) | 29.3% | 19.7% | +1.3% | $108 (vs. $102 current) |

Source: Company filings, Reuters, and SEC 10-K filings.

What happens next: Supply chain and inflation implications

The urea price drop is a leading indicator for broader fertilizer market trends. Here’s how it cascades:

1. Corn and wheat futures: Lower urea costs reduce input costs for U.S. corn (currently trading at $5.10/bushel) and wheat ($6.30/bushel), but the effect is muted by oversupply. “The market is pricing in a 3% yield boost from cheaper fertilizer, but global stocks are already at 20-year highs,” says Jim Wiesemeyer, chief commodity analyst at StoneX. CME Group data shows corn futures have only risen 0.4% since urea prices fell.

2. Inflation pressure: The USDA’s Food Price Outlook projects fertilizer costs will contribute just 0.1 percentage points to CPI in 2026, down from 0.8pp in 2024. “This is a deflationary tailwind for food prices, but it won’t offset rising labor or energy costs,” says Dr. Vasquez.

3. Russian fertilizer exports: Iran’s continued sanctions on Russian urea (2.1% of global supply) create a supply gap, but Europe’s stockpiles—up 15% YoY—mitigate the risk. “The real wild card is China’s domestic urea production, which surged 12% in 2025,” notes Karlsson. “If they flood the market, prices could drop another 10% by Q4.”

Who wins and who loses in the urea price war

The urea price correction benefits downstream industries but exposes vulnerabilities in the supply chain:

- Winners:

- Farmers with unhedged contracts: Those who avoided locking in 2024 prices (e.g., 40% of U.S. soybean farmers, per Farm Journal) gain a 12.5% cost advantage.

- Retailers like Tractor Supply (NASDAQ: TSCO): Lower input costs improve margins on seed-and-feed sales, though TSCO’s stock has only risen 0.9%—reflecting cautious consumer spending.

- Losers:

- Hedged producers like Bennett: Farmers with fixed-price contracts face a $0.75/bushel revenue gap on corn and wheat.

- European producers (e.g., Yara):** Their unhedged exposure to urea prices leaves them vulnerable to further declines.

- Russian exporters: Sanctions limit their ability to capitalize on lower global prices.

The takeaway: A temporary reprieve or a new normal?

The urea price drop is a correction, not a collapse. Global nitrogen demand remains robust—supported by India’s 4.2% YoY fertilizer consumption growth and Brazil’s 6.8% expansion in corn acreage—but the oversupply headwind will persist unless geopolitical tensions flare again. “The market is pricing in a 5% price recovery by Q4 2026, assuming no further Red Sea disruptions,” says Chen. For now, the data supports a sideways trend: urea prices will stabilize at $380–$420/mt, but the risk of a 15% rebound remains if Iran escalates attacks.

Farmers like Bennett must act fast: renegotiate hedges, lock in forward contracts, or pivot to crops with lower urea dependence (e.g., soybeans). Meanwhile, investors should watch CF Industries and Nutrien for earnings beats—but brace for volatility if China’s production surge materializes.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.