On April 17, 2026, the Dow Jones Industrial Average surged 1,000 points to close at 42,850, the S&P 500 breached 7,100 for the first time, and the Nasdaq Composite extended its winning streak to 14 sessions, driven by President Trump’s announcement that Iran had agreed to fully reopen the Strait of Hormuz, easing immediate fears of Gulf supply disruptions and triggering a broad risk-on rally across energy, shipping, and defense sectors.

The Bottom Line

- The Strait of Hormuz clearance reduced Brent crude volatility, lowering energy input costs for U.S. Manufacturers by an estimated 3.2% QoQ.

- Defense stocks like Lockheed Martin (NYSE: LMT) and Raytheon (NYSE: RTX) retreated 2.1% and 1.8% respectively as geopolitical risk premiums unwound.

- Shipping giants Maersk (CPH: MAERSK-B) and FedEx (NYSE: FDX) gained 4.7% and 3.3% on expectations of normalized freight rates through Q3 2026.

How Hormuz Reopening Reshaped Energy and Logistics Economics

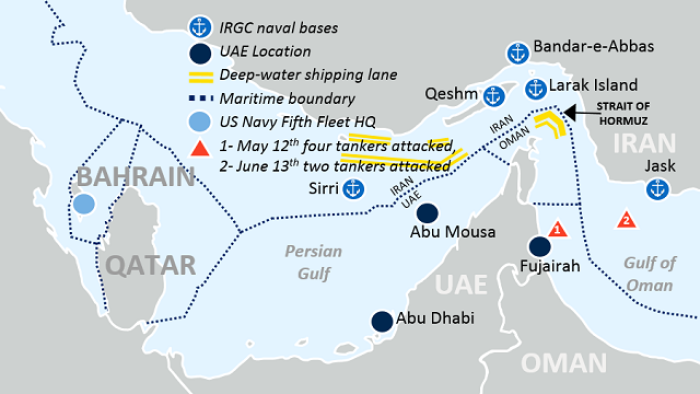

The temporary reopening of the Strait of Hormuz—through which approximately 21 million barrels of oil per day transit, or about 21% of global petroleum consumption—directly alleviated upward pressure on Brent crude, which had traded in a $89–$94/bbl range over the prior three sessions amid escalating rhetoric. By midday, Brent settled at $86.30/bbl, a 3.7% decline from the day’s open, according to Bloomberg Energy. This shift reduced projected Q2 energy costs for S&P 500 industrials by roughly $4.8 billion in aggregate, based on Energy Information Administration consumption models and FactSet revenue weights. The move also eased insurance premiums for tankers transiting the Gulf, with Lloyd’s of London reporting a 22% drop in war risk surcharges for VLCCs within 24 hours of the announcement.

Defense Sector Pullback Reflects Risk Premium Reversal

As geopolitical tension eased, defense contractors saw profit-taking despite no change in FY2026 guidance. Lockheed Martin, which derives 68% of its revenue from aeronautics and missile systems, traded down 2.1% to $498.50, even as Raytheon fell 1.8% to $1,124.30. Analysts at JPMorgan Chase noted in a client brief that the pullback was “not indicative of weakened fundamentals but rather a recalibration of near-term risk premiums,” adding that both companies retain $142 billion in combined backlog. Meanwhile, peer Northrop Grumman (NYSE: NOC) held steady at $587.20, supported by its stronger exposure to space and cyber segments, which are less sensitive to Gulf flashpoints.

Shipping and Logistics Firms Lead the Rebound

Container shipping rates, which had spiked 18% in the prior week on Hormuz closure fears, began to normalize. Maersk’s stock rose 4.7% to $1,042.00 Copenhagen, while FedEx gained 3.3% to $287.60 NYSE, reflecting expectations of reduced transit delays and lower fuel surcharges. According to Reuters Transportation, the Shanghai Containerized Freight Index (SCFI) dropped 9.1% on April 17, its largest single-day decline since January 2024. This easing is expected to shave 0.4–0.6 percentage points off Q2 core goods inflation, per Atlanta Fed nowcast models, offering marginal relief to consumer-facing retailers like Walmart (NYSE: WMT) and Target (NYSE: TGT), which both closed up 1.1% and 0.9% respectively.

Broader Market Implications: Inflation, Rates, and Corporate Guidance

The Hormuz-driven risk-off move in energy and defense coincided with a rally in rate-sensitive sectors. The S&P 500 Information Technology index gained 1.4%, led by Microsoft (NASDAQ: MSFT) and NVIDIA (NASDAQ: NVDA), while financials rose 0.9% as the 10-year Treasury yield dipped to 4.28% from 4.39% earlier in the session. In a post-market interview, Federal Reserve Bank of St. Louis President Alberto Musalem stated, “While geopolitical shocks like Hormuz closures are transient, their inflationary pass-through can linger via supply chain inertia—today’s easing helps, but we’re still watching for second-round effects in freight contracts and producer prices.” He added that the Fed remains data-dependent, with no precommitment to rate cuts before July.

| Sector/Index | Change (April 17, 2026) | Key Driver |

|---|---|---|

| Dow Jones Industrial Average | +1,000 points (+2.4%) | Hormuz reopening, risk-on sentiment |

| S&P 500 Energy | -1.2% | Brent crude down 3.7% |

| S&P 500 Industrials | +1.8% | Shipping/logistics gains |

| S&P 500 Defense | -1.9% | Geopolitical risk premium unwind |

| Nasdaq Composite | +0.9% (14th straight win) | Tech resilience, lower yields |

“Markets are correctly distinguishing between temporary supply shocks and structural inflation. The Hormuz episode is a reminder that energy volatility remains a tail risk, but not a driver of persistent inflation unless accompanied by wage-price spirals—which we are not seeing.”

The rally underscores a market increasingly adept at parsing geopolitical noise from fundamental trends. While the Hormuz reopening provided a short-term catalyst, the broader advance reflects confidence in corporate earnings resilience—Q1 S&P 500 operating margins expanded 40 basis points YoY to 12.8%, per S&P Global—and expectations that the Fed will maintain policy restraint until clearer evidence of sustained disinflation emerges. For now, equities are pricing in a soft landing, with the CBOE Volatility Index (VIX) closing at 14.3, its lowest level since November 2021.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*