As markets open on Monday, Big Tech’s $16 trillion earnings week begins, with Apple (NASDAQ: AAPL), Microsoft (NASDAQ: MSFT), Alphabet (NASDAQ: GOOGL), Amazon (NASDAQ: AMZN) and Nvidia (NASDAQ: NVDA) set to report results that will test whether the S&P 500’s rally, driven by AI optimism and resilient consumer spending, can persist amid rising interest rates and geopolitical tension.

The Bottom Line

- Collective market cap of the five firms exceeds $16 trillion, representing over 30% of the S&P 500’s weight.

- Analysts expect blended earnings growth of 12.4% YoY, with Nvidia guiding for 200%+ AI-related revenue surge.

- A miss in cloud or AI guidance could trigger a 5-8% sector correction, impacting broad market momentum.

Earnings Expectations Set High Bar for AI-Driven Growth Narrative

Wall Street anticipates the Magnificent Five will deliver combined Q1 2026 revenue of $387.2 billion, up 10.8% year-over-year, according to Bloomberg consensus estimates. Microsoft’s Azure cloud division is projected to grow 31% YoY, while Amazon Web Services (AWS) aims for 29% expansion, both critical to justifying premium valuations. Nvidia, whose stock has risen 214% over the past 12 months, faces the highest bar: analysts model its data center revenue reaching $22.5 billion for the quarter, a 210% increase from Q1 2025. Any shortfall in AI infrastructure demand could ripple through semiconductor supply chains, affecting TSMC and ASML, whose forward guidance is tightly tied to Nvidia’s orders.

“The market isn’t pricing in perfection—it’s pricing in continued AI acceleration. If Nvidia doesn’t beat and raise, we see a valid catalyst for profit-taking across the entire tech complex.”

Macro Headwinds Test Resilience of Consumer-Focused Giants

Beyond AI, Amazon and Apple face scrutiny over consumer resilience. Amazon’s North American retail segment is forecast to grow just 4.1% YoY, down from 6.3% in Q4 2025, as persistent inflation pressures discretionary spending. Apple’s iPhone revenue, comprising roughly 52% of total sales, is expected to grow only 2.8% YoY, reflecting slower upgrade cycles in mature markets. Both companies are offsetting weakness with services growth—Apple Services at 18% YoY and Amazon Advertising at 21%—but margin expansion remains critical. Apple’s gross margin is projected at 46.3%, up 40 basis points from last year, while Amazon targets a 6.2% operating margin in North America, up from 5.1% a year ago.

Regulatory Pressure Looms as Market Concentration Draws Scrutiny

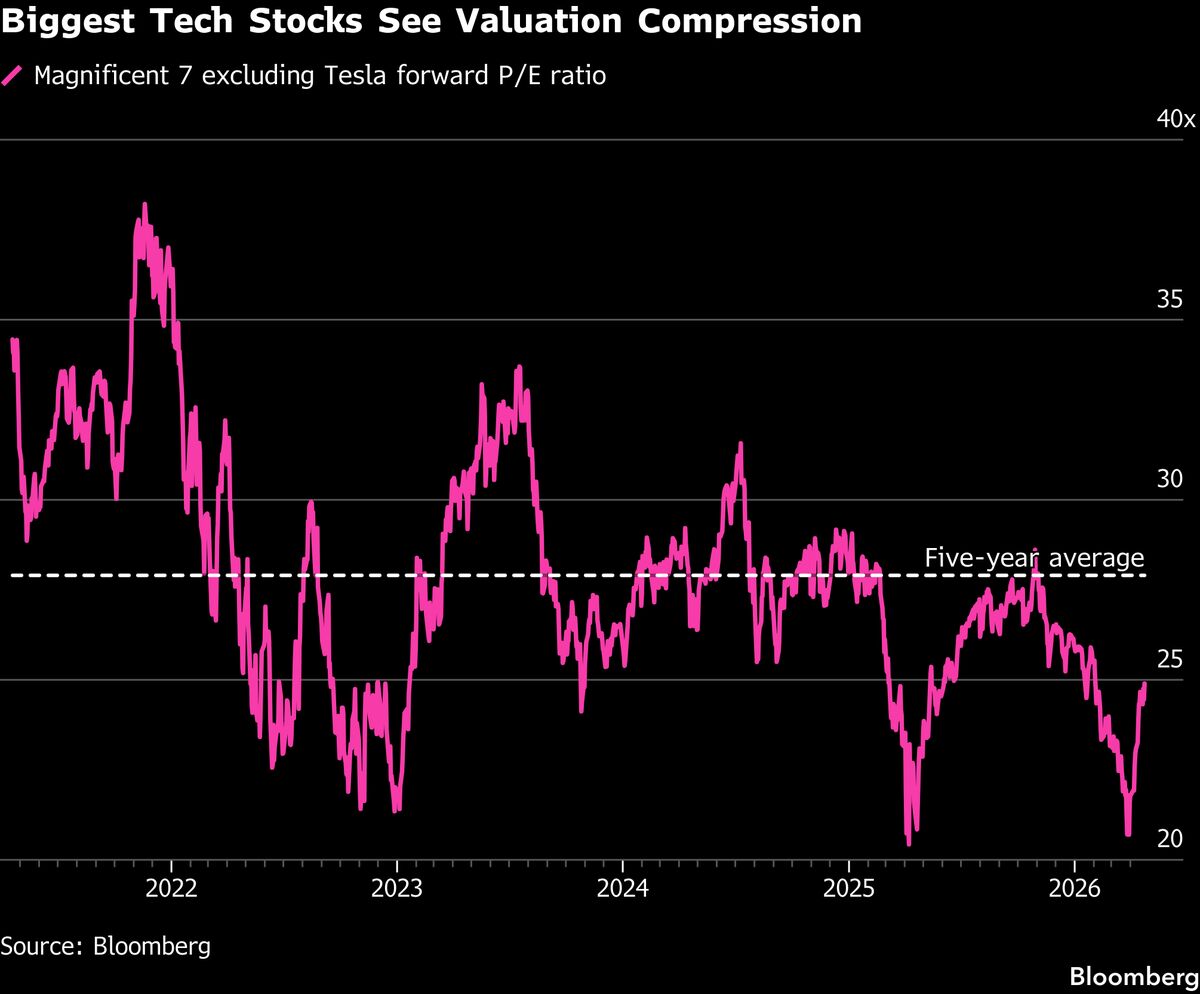

The unprecedented scale of these firms has renewed antitrust focus. The U.S. Department of Justice is reportedly preparing a filing later this year alleging that Google’s search and advertising practices violate Section 2 of the Sherman Act, a claim Alphabet denies. Meanwhile, the Federal Trade Commission continues its examination of Amazon’s marketplace practices, particularly regarding self-preferencing. Regulatory risk is now embedded in forward PE ratios: Alphabet trades at 22.4x forward earnings, a 15% discount to its five-year average, reflecting investor skepticism about long-term regulatory outcomes. Microsoft, by contrast, commands a 34.1x multiple, buoyed by its enterprise software moat and lower regulatory exposure.

| Company | Market Cap (Trillions) | Forward P/E | Q1 2026 Revenue Estimate (Billions) | Key Growth Driver |

|---|---|---|---|---|

| Apple (NASDAQ: AAPL) | 3.0 | 28.7 | 94.3 | Services (18% YoY) |

| Microsoft (NASDAQ: MSFT) | 3.1 | 34.1 | 72.1 | Azure Cloud (31% YoY) |

| Alphabet (NASDAQ: GOOGL) | 2.0 | 22.4 | 80.5 | Search & YouTube Ads |

| Amazon (NASDAQ: AMZN) | 1.9 | 48.9 | 152.3 | AWS (29% YoY) & Advertising |

| Nvidia (NASDAQ: NVDA) | 3.2 | 62.3 | 22.5 (Data Center) | AI Chips (210% YoY) |

Sector Performance Sets Tone for Broader Market Direction

Should the group deliver in-line results with optimistic guidance, the S&P 500 could test 5,600 by month-end, driven by renewed confidence in earnings durability. Conversely, a combined earnings miss exceeding 2% below estimates—particularly if driven by weak cloud or consumer spending—could trigger a 100-point pullback in the index, revisiting the 5,200 support level. Historical precedent shows that during the last four major tech earnings weeks, a positive surprise averaged a 1.8% S&P 500 gain over the following five sessions, while a miss yielded a 2.3% decline. The correlation remains strong: over 60% of the index’s weekly variance during earnings season is attributable to Mega Cap tech performance.

“Investors aren’t just buying earnings—they’re buying the optionality of AI monetization. The real test is whether capex translates to revenue faster than interest expenses rise.”

The upcoming earnings week is not merely a corporate reporting cycle—This proves a stress test for the current market regime. With the Federal Reserve holding rates at 4.50%-4.75% and core PCE inflation at 2.8%, any deterioration in tech fundamentals could accelerate a rotation into value and defensive sectors. Conversely, beats and raises could reinforce the narrative that AI-driven productivity gains are beginning to offset demographic and fiscal headwinds, supporting further multiple expansion. For now, the market waits for clarity—delivered in cold, hard numbers—not speculation.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*