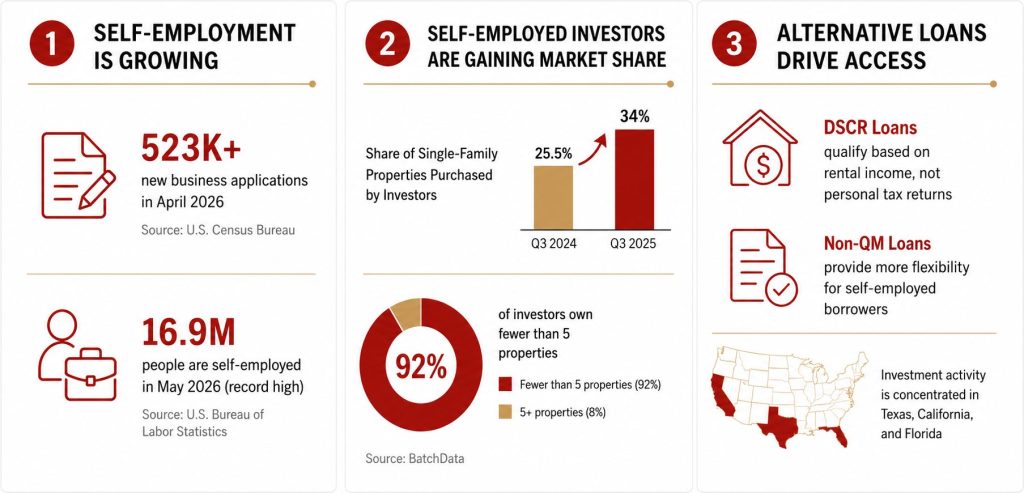

The Shift Toward DSCR Financing Among U.S. Independent Contractors

The rapid expansion of the U.S. self-employed workforce is fundamentally altering residential real estate investment strategies. By prioritizing Debt Service Coverage Ratio (DSCR) loans—which evaluate property-generated rental income rather than personal tax returns—independent contractors are circumventing traditional underwriting hurdles, effectively democratizing access to institutional-grade leveraged real estate acquisition.

The rise of the “gig economy” investor is no longer a fringe phenomenon; it is a structural shift in how liquidity enters the housing market. As traditional W-2 employment models face volatility, the self-employed are leveraging non-QM (non-qualified mortgage) products to scale property portfolios, creating a new class of investors who treat residential units as independent business assets rather than personal debt obligations.

The Bottom Line

- Underwriting Evolution: DSCR loans shift the risk assessment from the borrower’s personal income volatility to the asset’s cash flow potential, lowering the barrier to entry for freelancers and small business owners.

- Interest Rate Sensitivity: Because DSCR loans typically carry interest rates 100 to 200 basis points higher than conventional mortgages, these investors are highly sensitive to rental yield compression in a high-rate environment.

- Market Concentration: The influx of self-employed capital is skewing demand toward high-yield rental markets, potentially decoupling local home prices from local median income levels.

The Mechanics of DSCR Arbitrage

The core appeal of the DSCR loan lies in its departure from the standard 1040-tax-return-based qualification. For a self-employed individual, traditional mortgage applications often result in lower borrowing power due to tax deductions that artificially suppress reported net income. According to data from BlackRock (NYSE: BLK), which tracks institutional shifts in credit availability, non-QM originations have maintained a resilient footprint despite the broader tightening of credit standards by the Federal Reserve.

Here is the math: A DSCR of 1.0 means the property’s rent exactly covers the mortgage payment (PITI). Most lenders now require a ratio of 1.2 or higher. For the borrower, this turns the property into a self-contained financial entity. If the rental market in a specific corridor remains robust, the investor can scale indefinitely, provided they maintain the required cash reserves.

| Metric | Conventional Mortgage | DSCR Loan |

|---|---|---|

| Primary Qualification | Debt-to-Income (DTI) / Tax Returns | Cash Flow (Rental Income) |

| Interest Rate Premium | Baseline | +1.5% to +2.5% avg. |

| Down Payment Requirement | Typically 5%–20% | Typically 20%–30% |

| Employment History | 2 Years Required | Minimal / Not Required |

Macroeconomic Implications and Institutional Feedback

This trend is not occurring in a vacuum. As the Bureau of Labor Statistics continues to report shifts in labor participation, the secondary mortgage market has responded by securitizing these loans. Investors are essentially betting that the “entrepreneurial class” will maintain higher repayment discipline to protect their business credit profiles.

However, the risks are pronounced. “The reliance on DSCR financing creates a feedback loop where property prices are dictated by rental yield projections rather than fundamental housing demand from owner-occupants,” notes a senior economist at a major housing think tank. “When the yield spread tightens—due to rising maintenance costs or occupancy dips—these portfolios become highly vulnerable to cash flow insolvency.”

The competitive landscape is also shifting. Major players like Rocket Companies (NYSE: RKT) and loanDepot (NYSE: LDI) have been recalibrating their product suites to capture this segment. By facilitating these loans, they aren’t just selling mortgages; they are effectively underwriting the expansion of the “investor-landlord” class, which puts them in direct competition with private equity firms for inventory.

The Sustainability of the Self-Employed Investor Model

The long-term viability of this model depends on the stability of the rental market. As of July 2026, rental growth has moderated in several Tier-1 metros, forcing investors to look toward Tier-2 and Tier-3 markets to maintain the required 1.25 DSCR. This geographic migration is putting upward pressure on home prices in suburban areas, a trend monitored closely by the Federal Open Market Committee as they weigh the impact of housing costs on core inflation.

But the balance sheet tells a different story. While these investors are providing necessary liquidity to the rental market, they are also introducing a layer of fragility. Should the labor market for independent contractors soften, the lack of traditional income buffers could lead to a localized surge in distressed asset sales, particularly if the investors are over-leveraged across multiple non-QM portfolios.

For the sophisticated market participant, the signal is clear: watch the spread between residential rental yields and the cost of capital for non-QM products. If that spread narrows below 200 basis points, the rush of new investors will likely stall, leading to a consolidation of these portfolios into the hands of better-capitalized institutional operators.

Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.