The U.S. National debt has reached $39 trillion, primarily held by domestic entities including the Federal Reserve, mutual funds, and pension funds, alongside foreign governments like Japan and China. This massive accumulation reflects the U.S. Government’s reliance on Treasury securities to fund systemic deficits and global hegemony.

I’ve spent the better part of my career walking the halls of power from Brussels to Riyadh, and if there is one thing I’ve learned, it is that debt is never just about accounting. It is about power. When we gaze at a $39 trillion ledger, we aren’t just looking at a bill. we are looking at the world’s most complex web of geopolitical leverage.

Earlier this week, as the latest Treasury data filtered through the wires, the sheer scale of the debt became a focal point for analysts. But here is the catch: the “Who” matters far more than the “How much.” The shift in who holds this debt dictates whether the U.S. Maintains its “exorbitant privilege” or begins a gradual slide toward a multipolar financial reality.

The Great Domestic Pivot: A Shield Against Foreign Pressure

For decades, the narrative was centered on the “China Threat”—the idea that Beijing could crash the U.S. Economy by dumping Treasuries. But if you look closely at the current distribution, that leverage has eroded. A massive portion of the debt is now held domestically. The Federal Reserve, through various quantitative easing cycles, has essentially become the lender of last resort for the U.S. Government.

Here’s a strategic pivot. By shifting the debt burden toward internal institutions—pension funds, 401(k)s, and the Fed—the U.S. Reduces its vulnerability to external geopolitical blackmail. However, this creates a recent, internal fragility: the “inflation tax.” When the Fed prints money to buy debt, it risks eroding the purchasing power of the very citizens whose retirement funds are tied to these bonds.

But there is more to the story. This domestic concentration is inextricably linked to the International Monetary Fund’s ongoing observations regarding global liquidity. As the U.S. Leans inward, other nations are forced to find new anchors for their reserves.

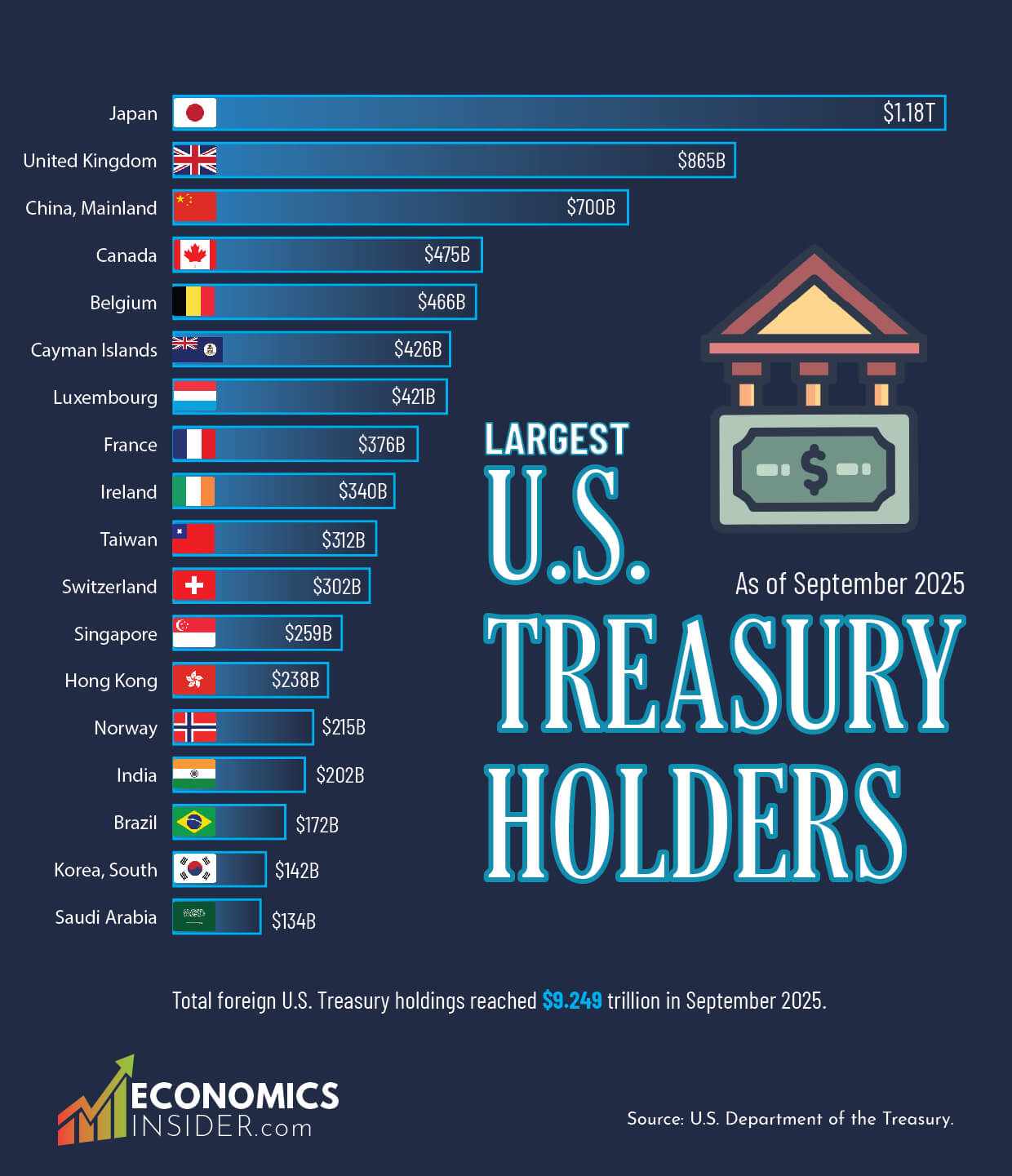

The Geopolitical Chessboard of Foreign Holdings

Whereas domestic holdings dominate, the foreign slice of the pie remains the most volatile. Japan remains the largest foreign holder, a relationship built on decades of symbiotic trade and security reliance. China, however, has been strategically diversifying. This isn’t just about risk management; it is about the “de-dollarization” movement.

We are seeing a slow-motion migration toward “non-traditional” reserve assets. Gold is making a comeback in the vaults of central banks from the Global South to the East. This shift is a direct response to the weaponization of the dollar, specifically the freezing of Russian reserves following the invasion of Ukraine.

“The transition from a unipolar financial system to a fragmented one is not an overnight event, but a gradual erosion of trust in the dollar as the sole neutral reserve asset.” — Dr. Zhu Xiaodan, Senior Fellow at the Institute for International Economic Studies.

Here is why that matters: if the world stops seeing the U.S. Treasury as the “risk-free asset,” the cost of borrowing for Washington skyrockets. That means fewer resources for foreign aid, a smaller defense budget for overseas bases, and a diminished ability to project power in the Indo-Pacific.

Mapping the Debt Architecture

To understand the gravity of this situation, we have to look at the breakdown of the holders. The following table illustrates the primary pillars of the $39 trillion architecture as of early 2026.

| Holder Category | Primary Motivation | Geopolitical Risk Level | Impact on US Sovereignty |

|---|---|---|---|

| Federal Reserve | Monetary Policy/Liquidity | Medium (Inflationary) | High (Internal Control) |

| Mutual/Pension Funds | Safe Returns/Retirement | Low (Market Volatility) | Moderate (Social Stability) |

| Japan (MoF) | Currency Stability | Low (Strategic Ally) | Moderate (Trade Balance) |

| China (PBOC) | Reserve Diversification | High (Strategic Rival) | Moderate (Declining) |

| Other Foreign Govts | Capital Preservation | Medium (Political Shift) | Low (Fragmented) |

The Ripple Effect on Global Supply Chains and Security

You might wonder how a government bond affects the price of a semiconductor in Taiwan or a shipping container in Rotterdam. The connection is the “Cost of Capital.” When the U.S. Manages its debt through interest rate hikes, it triggers a global vacuum of liquidity.

Emerging markets, often holding debt denominated in dollars, find themselves in a vice. As the U.S. Treasury attracts more capital to fund its $39 trillion burden, capital flees the Global South. This leads to currency collapses, political instability, and an increased reliance on Chinese loans through the World Bank alternatives or bilateral agreements.

This is the “Debt Trap” diplomacy in reverse. By maintaining a massive debt load that requires high interest rates to attract buyers, the U.S. Inadvertently pushes developing nations into the orbit of its rivals. It is a paradox of power: the very tool used to fund American global leadership is creating the conditions for its obsolescence.

“We are witnessing the emergence of a ‘bifurcated’ financial world, where the choice of reserve asset is no longer just an economic decision, but a declaration of political alignment.” — Ambassador Elena Rossi, Former EU Trade Envoy.

For a deeper dive into the mechanics of this shift, the Bank for International Settlements provides critical data on the “cross-border claims” that define these relationships.

The Bottom Line for the Global Order

the $39 trillion debt is not a ticking time bomb in the way sensationalist headlines suggest. It is more like a slow leak in a massive ship. The ship is still the largest in the ocean, but it is sitting lower in the water than it was twenty years ago.

The real danger isn’t a sudden default—that’s a fantasy. The danger is the gradual loss of the dollar’s status as the undisputed global medium of exchange. When the world stops needing to hold Treasuries to facilitate trade, the U.S. Loses its ability to print money to solve its problems without triggering hyperinflation.

We are entering an era of “Financial Realism.” The U.S. Must now balance its domestic appetite for spending with the reality that the world is looking for an exit strategy. The question is no longer whether the debt is sustainable, but whether the global trust that sustains it can be renewed.

As we move toward the end of the decade, do you believe the U.S. Can maintain its financial hegemony through sheer size, or is a fragmented, multi-currency world inevitable? I’d love to hear your thoughts in the comments below.