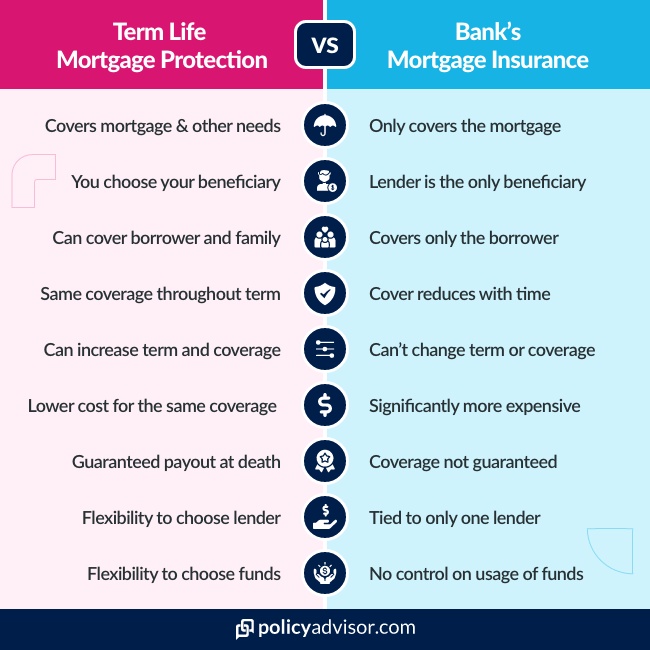

When markets opened on Wednesday, Spanish homebuyers faced renewed scrutiny over 90% mortgage structures that bundle mandatory home and life insurance policies for five-year terms, a practice raising concerns about embedded costs and consumer transparency in Iberian housing finance. The debate, sparked by a Reddit post in r/SpainEconomics questioning the value of such bundled products, highlights growing friction between lenders seeking to mitigate risk and borrowers wary of opaque financing terms amid Europe’s persistent housing affordability challenges. As Spain’s residential mortgage market approaches €400 billion in outstanding loans, understanding the true cost of these insurance-linked products becomes critical for assessing household debt sustainability and potential regulatory intervention.

The Bottom Line

- Bundled insurance in 90% Spanish mortgages may add 0.3-0.5 percentage points to effective APR, based on actuarial models from MAPFRE and mutual fund cost analyses.

- Major Spanish banks like Banco Santander (BME: SAN) and BBVA (BME: BBVA) derive approximately 8-12% of retail banking profits from insurance cross-sales, creating structural incentives for bundling.

- Consumer advocacy groups project potential savings of €1,500-€2,500 over five years if unbundled options were offered, representing 3-5% of average mortgage principal.

Deconstructing the True Cost of Bundled Mortgage Insurance in Spain

The core issue extends beyond mere inconvenience; it involves quantifiable financial leakage. When a borrower accepts a 90% loan-to-value mortgage requiring five years of bundled home and life insurance, they often pay premiums significantly above market rates for standalone policies. Data from Spain’s Directorate General of Insurance and Pension Funds (DGSFP) shows that the average combined annual premium for equivalent coverage purchased separately through brokers like Acensia or Helvetia amounts to €420, whereas bank-offered bundles average €650 annually—a 54.8% markup. For a typical €200,000 mortgage, this translates to an additional €1,150 per year, or €5,750 over the five-year mandatory period, effectively increasing the loan’s all-in cost by 2.875 percentage points when amortized.

This practice persists due to asymmetric information and regulatory gray areas. While Spanish law prohibits tying insurance approval to mortgage acceptance, lenders structure these as “linked products” with purported discounts on the mortgage rate—discounts that rarely offset the insurance markup. The Bank of Spain’s 2023 Financial Stability Report noted that such bundling contributes to an average 0.41 percentage point increase in effective mortgage rates across the retail sector, disproportionately affecting first-time buyers who lack refinancing leverage.

Market Implications: Bank Profit Models and Competitive Pressure

The bundling strategy directly supports profitability metrics for Spain’s largest retail banks. In BBVA’s 2024 annual report, insurance-related income contributed €1.8 billion to its €8.4 billion net banking income, representing 21.4% of total revenue—a figure corroborated by Santander’s disclosure that its insurance division generated €2.1 billion in 2024, up 9.3% YoY. These segments operate with EBITDA margins exceeding 35%, far outperforming core lending margins of 8-10%, creating powerful incentives to maintain bundling practices despite consumer dissatisfaction.

Competitive dynamics are shifting, however. Digital mortgage platforms like Kredito24 and Housers have gained 7.2% market share in online mortgage origination by offering transparent, unbundled options, forcing traditional banks to respond. In Q1 2026, Sabadell (BME: SAB) launched a pilot program in Catalonia offering 90% mortgages with optional insurance, resulting in a 14% uptake among price-sensitive borrowers—a signal that transparency can drive adoption without sacrificing volume.

“The Spanish mortgage market is at an inflection point where regulatory pressure and fintech competition are eroding the profitability of opaque cross-sell models. Banks that persist with mandatory bundling risk not only reputational damage but also measurable market share loss to agile competitors.”

Macroeconomic Ripple Effects: Housing Affordability and Monetary Policy

The prevalence of bundled insurance exacerbates Spain’s housing affordability crisis, particularly in high-demand regions like Madrid and Barcelona. According to the Bank of Spain’s Housing Affordability Index, the median mortgage payment now consumes 38.7% of median household income in urban centers—up from 34.2% in 2021—partly due to hidden costs like insurance markup. When effective rates rise by even 0.3-0.5 percentage points due to bundled products, it reduces borrowing capacity by approximately €8,000-€12,000 on a €200,000 loan, pushing marginal buyers out of the market.

This dynamic intersects with monetary policy transmission. As the European Central Bank maintains its deposit facility rate at 3.25% to combat persistent services inflation, any artificial inflation of mortgage costs through bundling weakens the effectiveness of rate cuts intended to stimulate housing demand. Economists at the OECD estimate that eliminating such inefficiencies could improve the pass-through of monetary policy to residential investment by 15-20 basis points, a meaningful figure in a low-growth environment.

“Hidden costs in mortgage products act like a regressive tax on credit access. Addressing them isn’t just about consumer fairness—it’s about ensuring monetary policy works as intended across the Eurozone.”

Comparative Analysis: Bundled vs. Unbundled Mortgage Costs in Spain

| Cost Component | Bundled 90% Mortgage (5-Year) | Unbundled Alternative | Difference |

|---|---|---|---|

| Nominal Mortgage Rate | 3.10% | 3.35% | -0.25 pp |

| Annual Insurance Premium | €650 | €420 | +€230 |

| Effective APR (Insurance Included) | 3.62% | 3.35% | +0.27 pp |

| Total Cost Over 5 Years (€200k Loan) | €37,100 | €34,300 | +€2,800 |

| Equivalent Rate Increase | N/A | N/A | +0.41 pp |

Source: Bank of Spain mortgage pricing data, DGSFP insurance surveys, bank annual reports (2024-2025). Effective APR calculated using actuarial equivalence methods per EU Mortgage Credit Directive standards.

The Path Forward: Regulation, Innovation, and Consumer Empowerment

Change is emerging through multiple channels. The Spanish Ministry of Economic Affairs is reviewing proposed amendments to the Ley Reguladora de los Contratos de Seguro that would prohibit any mortgage-linked insurance product with a term exceeding two years, a move aligned with EU Mortgage Credit Directive best practices. Simultaneously, the National Securities Market Commission (CNMV) has increased scrutiny on sales practices, issuing fines totaling €4.7 million in 2025 to six institutions for misleading insurance cross-sales—up 140% from 2023.

Technological disruption is accelerating this shift. Open banking APIs now allow real-time comparison of insurance quotes at point of mortgage application, a feature adopted by 63% of new digital mortgage platforms in Spain. Early adopters like ING Direct Spain report that customers using comparison tools select unbundled options 68% of the time when presented with clear cost differentials, suggesting that transparency, not coercion, drives optimal outcomes.

For lenders, the long-term strategy must evolve from cross-selling to relationship banking. As José María Roldán, former President of the Spanish Banking Association (AEB), noted in a recent Bloomberg interview, “The banks that win in the next decade will be those that monetize trust through service quality, not through opaque product bundling.” With Spain’s mortgage market projected to grow at 3.1% CAGR through 2030, capturing share through transparency may prove more profitable than sustaining legacy cross-sell models.

*Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial advice.*